Advertisement

Harmonic Drive Systems (TSE:6324): Assessing Valuation in Light of Jefferies Downgrade and Rising Chinese Competition

Simply Wall St

Reviewed by Kshitija Bhandaru

Harmonic Drive Systems (TSE:6324) is in focus after Jefferies downgraded the stock, flagging growing competitive pressure from Chinese firms and fresh strategic hurdles in key robotics markets. The announcement highlights how the company’s current valuation compares with these challenges.

See our latest analysis for Harmonic Drive Systems.

Shares of Harmonic Drive Systems have seen notable swings this year, with a recent 17.2% jump over the past month followed by a sharp pullback. The stock posted a 1-day share price return of -4.39% and a 7-day return of -11.59%. While current momentum appears to be fading, the stock’s longer-term performance presents a mixed picture, with a 1-year total shareholder return of 3.36% and a much steeper 3-year total return of -32.64%, highlighting how sentiment has shifted amid evolving competitive and strategic headwinds.

If these market moves have you scanning for your next big discovery, consider expanding your perspective and check out fast growing stocks with high insider ownership.

Given these dynamics, investors are left to weigh whether Harmonic Drive Systems is trading below its true value or if mounting challenges mean that the current share price already reflects any future growth potential. Is there still an opportunity here, or is everything priced in?

Price-to-Earnings of 77.6x: Is it justified?

Harmonic Drive Systems trades at a Price-to-Earnings (P/E) ratio of 77.6, putting its last close of ¥3,050 well above the typical level seen among Japanese machinery peers.

The P/E ratio measures how much investors are willing to pay today for a yen of current earnings. In industries with rapid profit expansion or high confidence in future growth, higher P/E ratios may be more justified. For Harmonic Drive Systems, this multiple signals that the market is pricing in significant future profit growth relative to its current profitability.

However, when compared to industry benchmarks, the gap is stark. The company’s P/E is significantly higher than both the Japanese Machinery industry average of 13.2x and the peer group’s 21.3x, highlighting a sizable premium. Notably, it is also substantially higher than the estimated fair Price-to-Earnings Ratio of 42.9x, suggesting the market price leaves little room for error and could revert toward the fair ratio as investor expectations adjust.

Explore the SWS fair ratio for Harmonic Drive Systems

Result: Price-to-Earnings of 77.6x (OVERVALUED)

However, persistent competitive pressure and any slowdown in revenue or net income growth could quickly challenge the company's premium valuation.

Find out about the key risks to this Harmonic Drive Systems narrative.

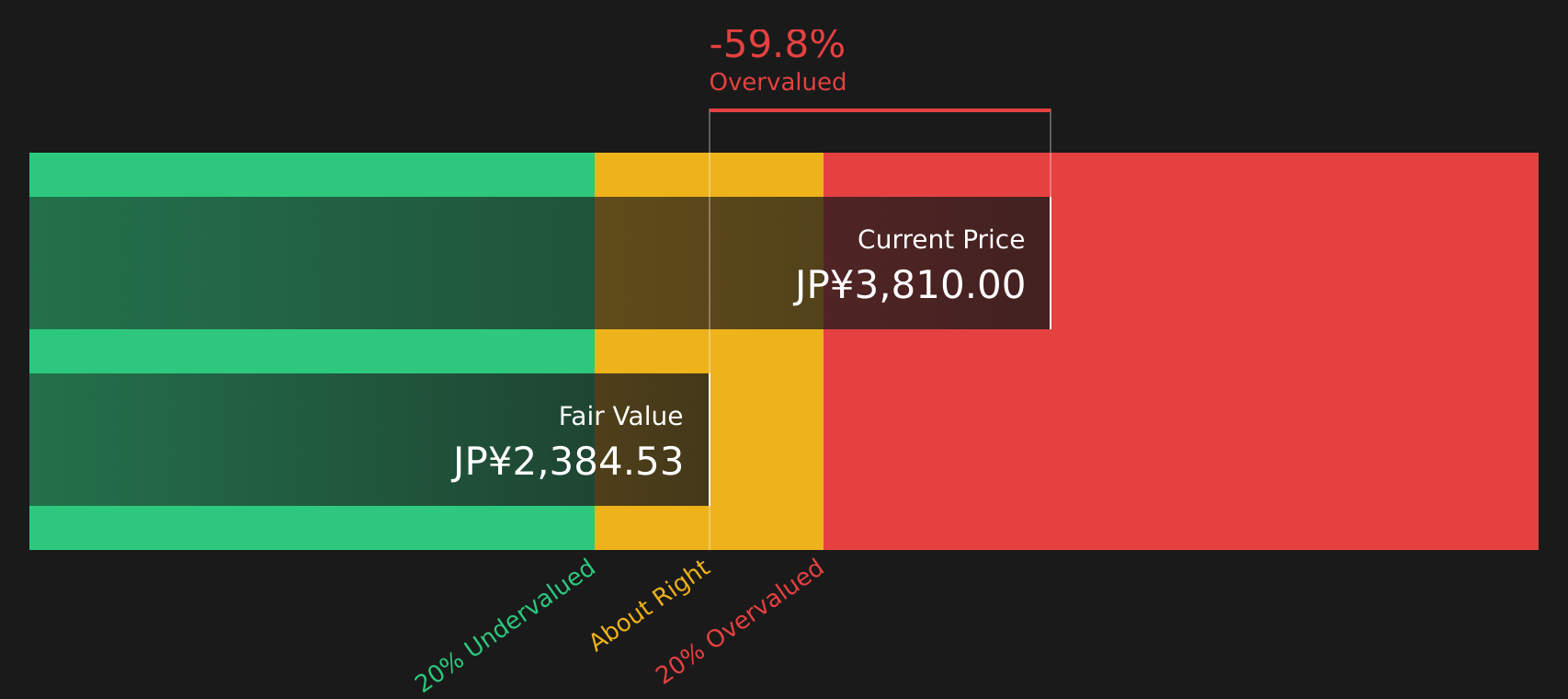

Another View: SWS DCF Model Points to Overvaluation

Taking a different angle, our DCF model suggests that Harmonic Drive Systems is trading well above its fair value, with the current price of ¥3,050 much higher than the DCF estimated value of ¥1,548. This perspective highlights the possibility that the market has already factored in too much optimism for future growth. Which viewpoint will prove more accurate as conditions unfold?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Harmonic Drive Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Harmonic Drive Systems Narrative

If you have a different perspective or enjoy running your own analysis, you can generate a personal take in just a few minutes. So why not Do it your way?

A great starting point for your Harmonic Drive Systems research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let your next big opportunity pass you by. Uncover standout stocks and fresh investment angles that you might have missed with these powerful tools:

- Start building future-focused positions by checking out these 874 undervalued stocks based on cash flows, which could be trading at significant discounts based on cash flows.

- Boost your search for growth potential by tapping into these 24 AI penny stocks, where artificial intelligence is already shifting the landscape.

- Secure your income by exploring these 18 dividend stocks with yields > 3%, featuring companies with yields over 3% for more reliable returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Harmonic Drive Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6324

Harmonic Drive Systems

Produces and sells precision control equipment and components worldwide.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor