Advertisement

OSG (TSE:6136) — Assessing Valuation After Strong Year-to-Date Growth

Simply Wall St

Reviewed by Kshitija Bhandaru

OSG (TSE:6136) continues to draw investor interest as it trends higher over the past month, not because of a fresh headline event but due to its solid performance and steady growth metrics.

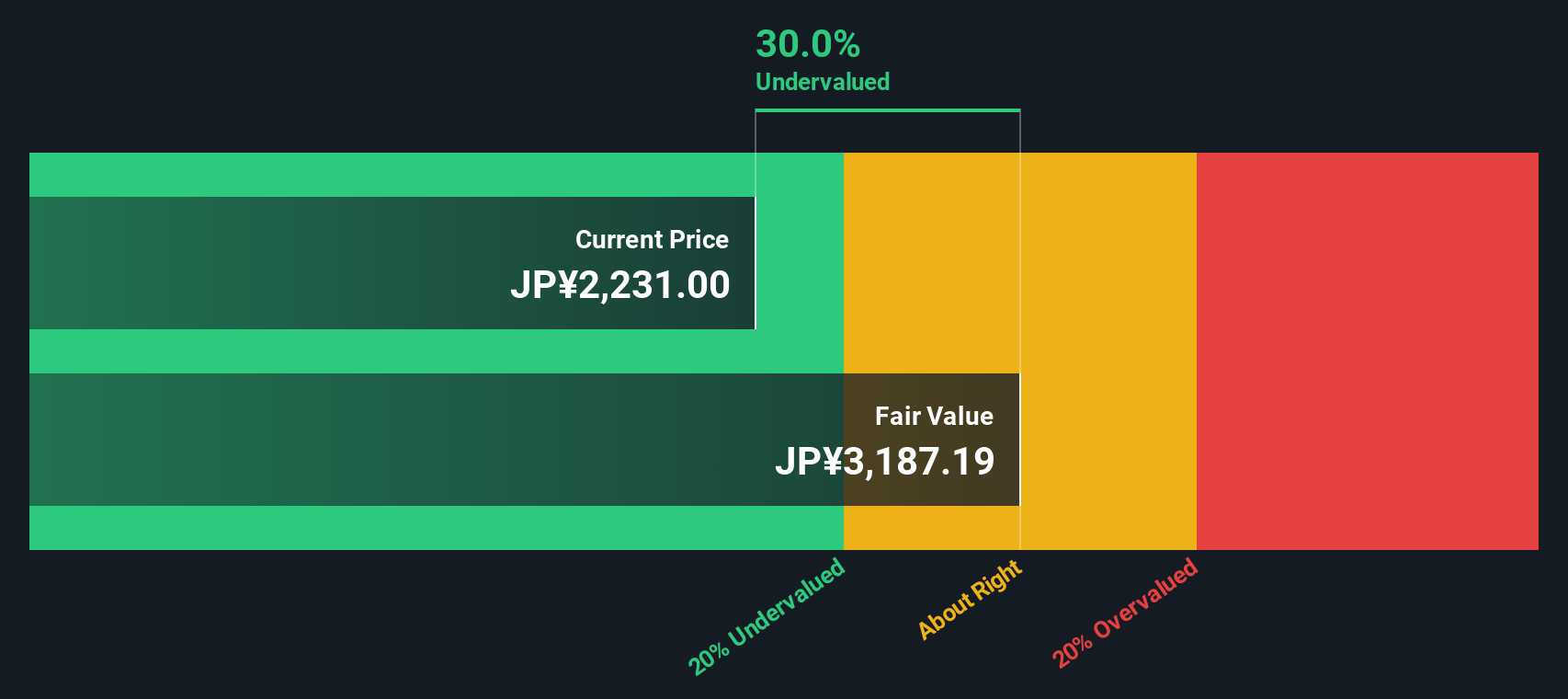

See our latest analysis for OSG.

Momentum has clearly been building for OSG, with the share price delivering a 7.99% return over the past month and extending to a hefty 21.71% return year-to-date. Even more impressively, OSG's total shareholder return of nearly 30% over the past year highlights how investors are catching on to its consistent growth trend.

If strong short-term results have you curious about what else is performing, now is the perfect time to broaden your search and discover fast growing stocks with high insider ownership

But with OSG currently trading above analyst price targets despite strong earnings momentum, investors are left to wonder whether there is still value to be found, or if the market is already factoring in all of the company’s future growth.

Price-to-Earnings of 13.8x: Is it justified?

OSG’s price-to-earnings ratio stands at 13.8x, making shares more expensive than both its peers and the sector average. With a last close price of ¥2231, the market appears to place a premium on OSG’s future growth or perceived quality, even though there are indications the multiple may not be fully justified.

The price-to-earnings ratio compares a company's share price to its earnings per share and is widely used to value manufacturing stocks like OSG. It reflects market expectations about future profitability and growth potential, making it highly relevant when analyzing established industrial firms.

The market is currently valuing OSG well above the peer average of 12x, and also above the JP Machinery industry average of 13.5x. Compared to an estimated fair P/E ratio of 13x, the current premium suggests investors anticipate better performance or lower risk ahead. However, this could leave little room for upside if those expectations are not met.

Explore the SWS fair ratio for OSG

Result: Price-to-Earnings of 13.8x (OVERVALUED)

However, risks such as slowing revenue growth and the stock trading above analyst targets could quickly change market sentiment for OSG moving forward.

Find out about the key risks to this OSG narrative.

Another View: What Does the DCF Model Say?

While OSG’s current price appears expensive based on earnings multiples, our SWS DCF model suggests a different story. The shares are trading at nearly 30% below their estimated fair value. This indicates the potential for undervaluation if long-term cash flows develop as modeled. Which approach will the market trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OSG for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OSG Narrative

If you'd like to form your own perspective or dive deeper into the numbers, it's easy to analyze the details and develop your own narrative in just a few minutes. Do it your way

A great starting point for your OSG research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors look beyond just one stock. Don’t pass up the chance to target your next opportunity. Simply Wall Street’s screener helps you spot new trends before they hit the headlines.

- Benefit from market shifts and tap into potential with these 898 undervalued stocks based on cash flows, which offers substantial upside based on future cash flow projections.

- Generate consistent passive income and see which companies stand out among these 19 dividend stocks with yields > 3%, featuring strong yields above 3%.

- Get ahead of disruptive innovation by reviewing these 24 AI penny stocks, where AI-powered businesses are making their mark in the tech sector.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6136

OSG

Manufactures and sells cutting tools in Japan, the Americas, Europe, Africa, and Asia.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor