Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Danto Holdings Corporation (TSE:5337) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Danto Holdings

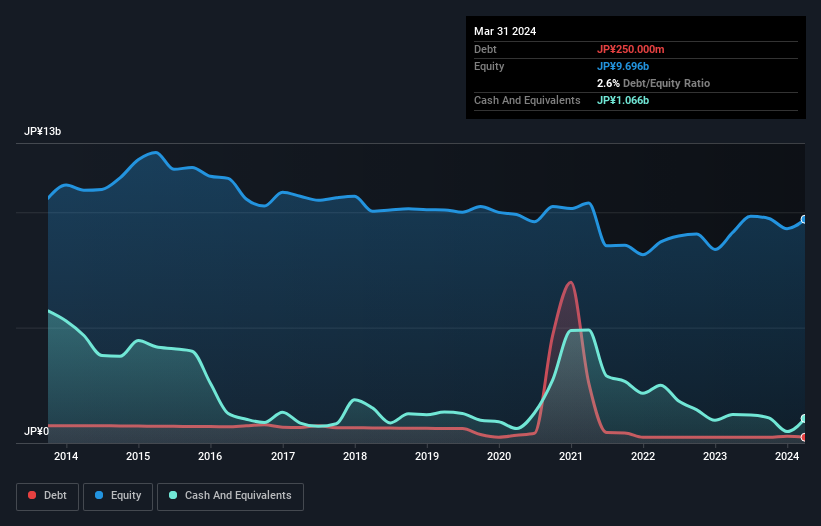

How Much Debt Does Danto Holdings Carry?

As you can see below, Danto Holdings had JP¥250.0m of debt, at March 2024, which is about the same as the year before. You can click the chart for greater detail. But it also has JP¥1.07b in cash to offset that, meaning it has JP¥816.0m net cash.

How Healthy Is Danto Holdings' Balance Sheet?

The latest balance sheet data shows that Danto Holdings had liabilities of JP¥1.20b due within a year, and liabilities of JP¥1.27b falling due after that. On the other hand, it had cash of JP¥1.07b and JP¥922.0m worth of receivables due within a year. So it has liabilities totalling JP¥488.0m more than its cash and near-term receivables, combined.

Given Danto Holdings has a market capitalization of JP¥21.5b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Danto Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is Danto Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Danto Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 18%, to JP¥5.8b. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Danto Holdings?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Danto Holdings lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through JP¥2.1b of cash and made a loss of JP¥687m. With only JP¥816.0m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Danto Holdings you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5337

Danto Holdings

Manufactures, sells, and installs ceramics and related products in Japan.

Mediocre balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.7% undervalued

RO

Community Contributor