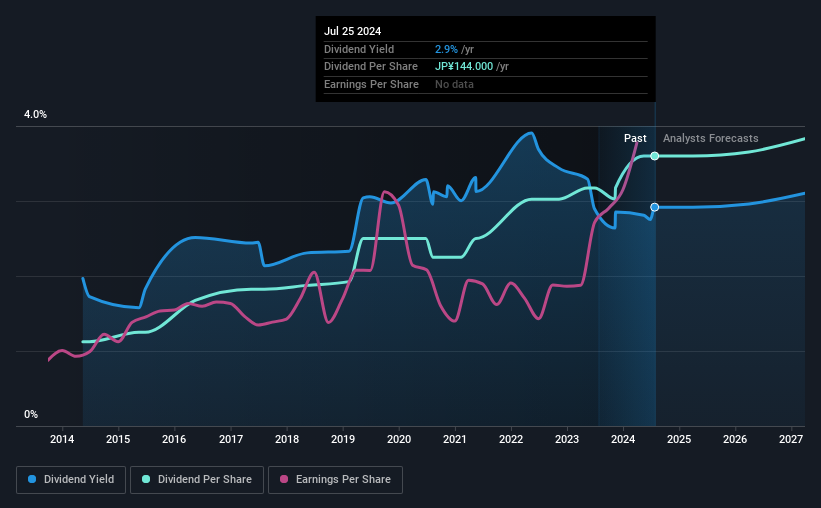

Taikisha Ltd. (TSE:1979) will pay a dividend of ¥60.00 on the 2nd of December. This takes the annual payment to 2.9% of the current stock price, which is about average for the industry.

Check out our latest analysis for Taikisha

Taikisha's Earnings Easily Cover The Distributions

Unless the payments are sustainable, the dividend yield doesn't mean too much. However, prior to this announcement, Taikisha's dividend was comfortably covered by both cash flow and earnings. This means that most of its earnings are being retained to grow the business.

EPS is set to fall by 4.1% over the next 12 months. Assuming the dividend continues along recent trends, we believe the payout ratio could be 34%, which we are pretty comfortable with and we think is feasible on an earnings basis.

Taikisha Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2014, the dividend has gone from ¥45.00 total annually to ¥144.00. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. Taikisha has impressed us by growing EPS at 13% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Taikisha's prospects of growing its dividend payments in the future.

Taikisha Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. The distributions are easily covered by earnings, and there is plenty of cash being generated as well. However, it is worth noting that the earnings are expected to fall over the next year, which may not change the long term outlook, but could affect the dividend payment in the next 12 months. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 1 warning sign for Taikisha that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

If you're looking to trade Taikisha, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Taikisha might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1979

Taikisha

Designs, manages, and constructs HVAC systems and automobile paint plants and sells related equipment in Japan and internationally.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Community Narratives