Advertisement

- Japan

- /

- Construction

- /

- TSE:1968

We Think That There Are Some Issues For Taihei Dengyo Kaisha (TSE:1968) Beyond Its Promising Earnings

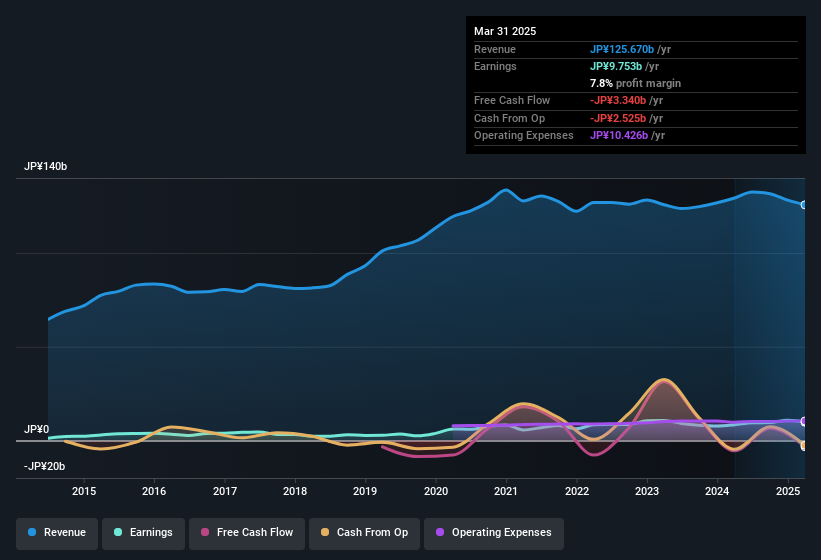

The recent earnings posted by Taihei Dengyo Kaisha, Ltd. (TSE:1968) were solid, but the stock didn't move as much as we expected. We believe that shareholders have noticed some concerning factors beyond the statutory profit numbers.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, Taihei Dengyo Kaisha issued 5.9% more new shares over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out Taihei Dengyo Kaisha's historical EPS growth by clicking on this link.

How Is Dilution Impacting Taihei Dengyo Kaisha's Earnings Per Share (EPS)?

As you can see above, Taihei Dengyo Kaisha has been growing its net income over the last few years, with an annualized gain of 16% over three years. And in the last year the company managed to bump profit up by 16%. On the other hand, earnings per share are only up 9.5% in that time. So you can see that the dilution has had a bit of an impact on shareholders.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So Taihei Dengyo Kaisha shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Impact Of Unusual Items On Profit

Finally, we should also consider the fact that unusual items boosted Taihei Dengyo Kaisha's net profit by JP¥1.0b over the last year. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. If Taihei Dengyo Kaisha doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Taihei Dengyo Kaisha's Profit Performance

To sum it all up, Taihei Dengyo Kaisha got a nice boost to profit from unusual items; without that, its statutory results would have looked worse. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. For the reasons mentioned above, we think that a perfunctory glance at Taihei Dengyo Kaisha's statutory profits might make it look better than it really is on an underlying level. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. Case in point: We've spotted 1 warning sign for Taihei Dengyo Kaisha you should be aware of.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Taihei Dengyo Kaisha might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:1968

Taihei Dengyo Kaisha

Engages in the plant construction business in Japan and internationally.

Excellent balance sheet with proven track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor