Advertisement

First Bank Of Toyama (TSE:7184) Has Announced That It Will Be Increasing Its Dividend To ¥15.00

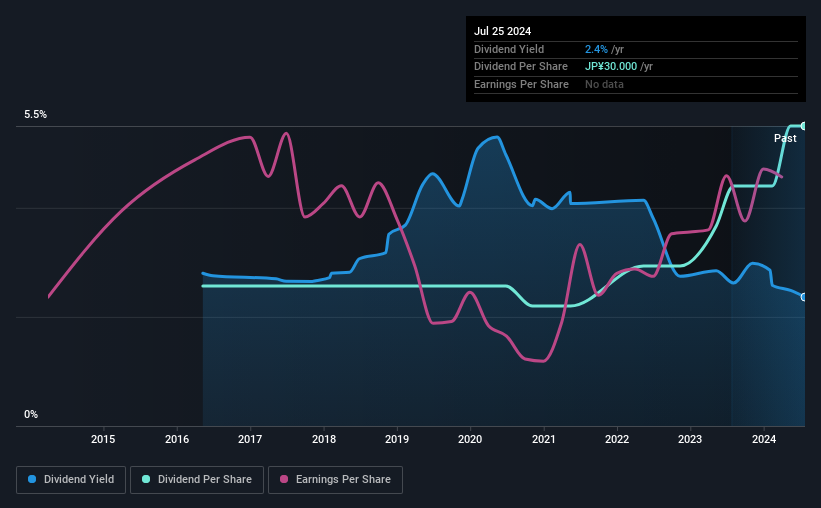

The First Bank Of Toyama, Ltd. (TSE:7184) has announced that it will be increasing its dividend from last year's comparable payment on the 5th of December to ¥15.00. Even though the dividend went up, the yield is still quite low at only 2.4%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that First Bank Of Toyama's stock price has increased by 36% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for First Bank Of Toyama

First Bank Of Toyama's Earnings Will Easily Cover The Distributions

Even a low dividend yield can be attractive if it is sustained for years on end.

First Bank Of Toyama has a good history of paying out dividends, with its current track record at 8 years. Past distributions do not necessarily guarantee future ones, but First Bank Of Toyama's payout ratio of 30% is a good sign for current shareholders as this means that earnings decently cover dividends.

Looking forward, earnings per share could rise by 9.1% over the next year if the trend from the last few years continues. If the dividend continues along recent trends, we estimate the future payout ratio will be 33%, which is in the range that makes us comfortable with the sustainability of the dividend.

First Bank Of Toyama's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2016, the annual payment back then was ¥14.00, compared to the most recent full-year payment of ¥30.00. This means that it has been growing its distributions at 10.0% per annum over that time. A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

We Could See First Bank Of Toyama's Dividend Growing

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's encouraging to see that First Bank Of Toyama has been growing its earnings per share at 9.1% a year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for First Bank Of Toyama's prospects of growing its dividend payments in the future.

First Bank Of Toyama Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 2 warning signs for First Bank Of Toyama that investors need to be conscious of moving forward. Is First Bank Of Toyama not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7184

First Bank Of Toyama

Provides banking and financial services for individual, corporate, and business customers.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|1.4% undervalued

RO

Community Contributor