- Japan

- /

- Auto Components

- /

- TSE:7256

Even after rising 13% this past week, Kasai Kogyo (TSE:7256) shareholders are still down 65% over the past five years

Kasai Kogyo Co., Ltd. (TSE:7256) shareholders will doubtless be very grateful to see the share price up 38% in the last quarter. But that is little comfort to those holding over the last half decade, sitting on a big loss. In fact, the share price has declined rather badly, down some 67% in that time. So is the recent increase sufficient to restore confidence in the stock? Not yet. We'd err towards caution given the long term under-performance.

While the last five years has been tough for Kasai Kogyo shareholders, this past week has shown signs of promise. So let's look at the longer term fundamentals and see if they've been the driver of the negative returns.

View our latest analysis for Kasai Kogyo

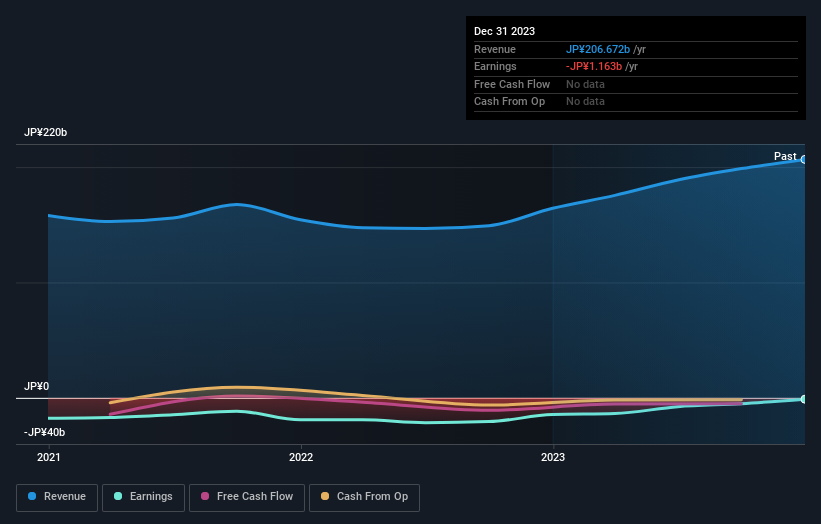

Kasai Kogyo isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

Over half a decade Kasai Kogyo reduced its trailing twelve month revenue by 5.1% for each year. While far from catastrophic that is not good. With neither profit nor revenue growth, the loss of 11% per year doesn't really surprise us. The chance of imminent investor enthusiasm for this stock seems slimmer than Louise Brooks. Ultimately, it may be worth watching - should revenue pick up, the share price might follow.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

This free interactive report on Kasai Kogyo's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Kasai Kogyo shareholders have received returns of 30% over twelve months, which isn't far from the general market return. To take a positive view, the gain is pleasing, and it sure beats annualized TSR loss of 11%, which was endured over half a decade. While 'turnarounds seldom turn' there are green shoots for Kasai Kogyo. It's always interesting to track share price performance over the longer term. But to understand Kasai Kogyo better, we need to consider many other factors. For example, we've discovered 3 warning signs for Kasai Kogyo (2 are a bit concerning!) that you should be aware of before investing here.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Japanese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Kasai Kogyo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7256

Kasai Kogyo

Engages in manufacture and sale of automotive interior and exterior parts, and related businesses in Japan and internationally.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives