- Japan

- /

- Auto Components

- /

- TSE:6493

Here's Why We're Wary Of Buying NITTAN's (TSE:6493) For Its Upcoming Dividend

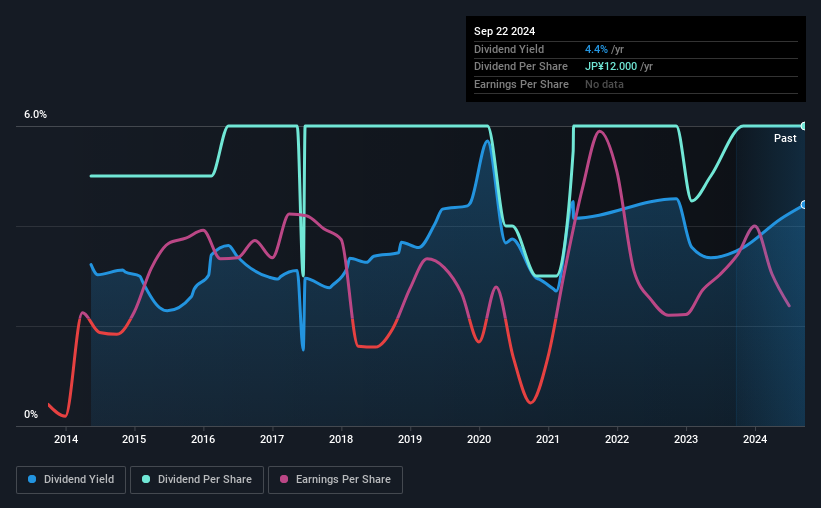

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see NITTAN Corporation (TSE:6493) is about to trade ex-dividend in the next 3 days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. This means that investors who purchase NITTAN's shares on or after the 27th of September will not receive the dividend, which will be paid on the 5th of December.

The company's next dividend payment will be JP¥6.00 per share. Last year, in total, the company distributed JP¥12.00 to shareholders. Looking at the last 12 months of distributions, NITTAN has a trailing yield of approximately 4.4% on its current stock price of JP¥271.00. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! We need to see whether the dividend is covered by earnings and if it's growing.

Check out our latest analysis for NITTAN

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. NITTAN distributed an unsustainably high 197% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. A useful secondary check can be to evaluate whether NITTAN generated enough free cash flow to afford its dividend. What's good is that dividends were well covered by free cash flow, with the company paying out 6.4% of its cash flow last year.

It's good to see that while NITTAN's dividends were not covered by profits, at least they are affordable from a cash perspective. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

Click here to see how much of its profit NITTAN paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. Readers will understand then, why we're concerned to see NITTAN's earnings per share have dropped 26% a year over the past five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the last 10 years, NITTAN has lifted its dividend by approximately 1.8% a year on average.

Final Takeaway

Should investors buy NITTAN for the upcoming dividend? It's not a great combination to see a company with earnings in decline and paying out 197% of its profits, which could imply the dividend may be at risk of being cut in the future. Yet cashflow was much stronger, which makes us wonder if there are some large timing issues in NITTAN's cash flows, or perhaps the company has written down some assets aggressively, reducing its income. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of NITTAN.

So if you're still interested in NITTAN despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. For example - NITTAN has 3 warning signs we think you should be aware of.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

If you're looking to trade NITTAN, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NITTAN might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6493

Flawless balance sheet average dividend payer.

Market Insights

Community Narratives