As global markets navigate a period of mixed economic signals, with the Nasdaq Composite reaching new heights and small-cap stocks underperforming, investors are closely watching the Federal Reserve's upcoming rate decision amid stalled inflation progress and a cooling labor market. In this environment, identifying high-growth tech stocks requires careful consideration of their ability to capitalize on technological advancements and maintain robust growth trajectories despite broader market volatility.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Material Group | 20.45% | 24.01% | ★★★★★★ |

| Yggdrazil Group | 30.20% | 87.10% | ★★★★★★ |

| Seojin SystemLtd | 35.41% | 39.86% | ★★★★★★ |

| eWeLLLtd | 27.24% | 28.74% | ★★★★★★ |

| Medley | 25.57% | 31.67% | ★★★★★★ |

| Waystream Holding | 22.09% | 113.25% | ★★★★★★ |

| Mental Health TechnologiesLtd | 25.83% | 113.12% | ★★★★★★ |

| CD Projekt | 24.92% | 27.00% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 131.08% | ★★★★★★ |

| JNTC | 29.48% | 104.37% | ★★★★★★ |

Click here to see the full list of 1267 stocks from our High Growth Tech and AI Stocks screener.

Let's dive into some prime choices out of from the screener.

TXT e-solutions (BIT:TXT)

Simply Wall St Growth Rating: ★★★★★☆

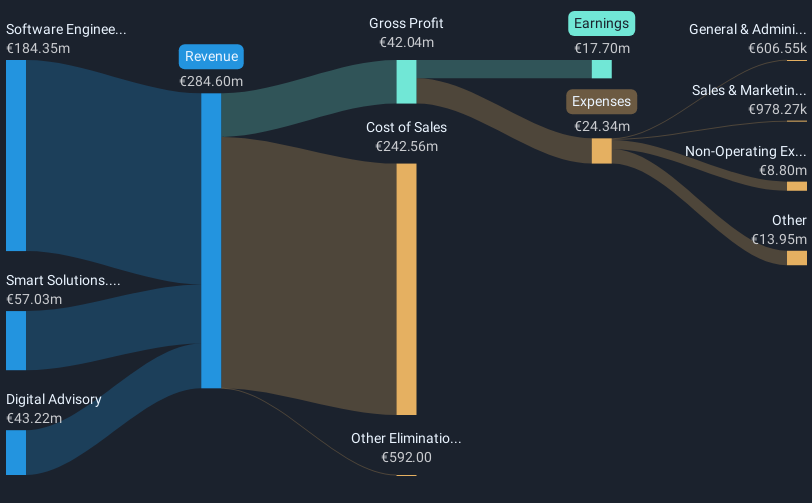

Overview: TXT e-solutions S.p.A. offers software and service solutions across Italy and globally, with a market cap of €443.54 million.

Operations: The company's revenue streams are primarily driven by Software Engineering (€184.35 million), followed by Smart Solutions (€57.03 million) and Digital Advisory (€43.22 million).

TXT e-solutions has demonstrated a robust trajectory in its financial performance, with recent earnings highlighting a significant uptick. In the third quarter of 2024 alone, sales surged to €81.37 million from €52.06 million in the previous year, while net income grew to €4.02 million from €3.01 million, reflecting an adept capability in scaling operations amidst competitive pressures. Annually, revenue is expected to climb by 13.6%, outpacing the Italian market's growth of 4%. Moreover, earnings are projected to expand at an impressive rate of 22.9% per year, surpassing market expectations of 7.1%. This financial momentum is underpinned by TXT's strategic focus on high-profile events and industry conferences such as their presentation at the Annual Flight Operations Conference, positioning them well for sustained growth within the tech sector.

Avant Group (TSE:3836)

Simply Wall St Growth Rating: ★★★★☆☆

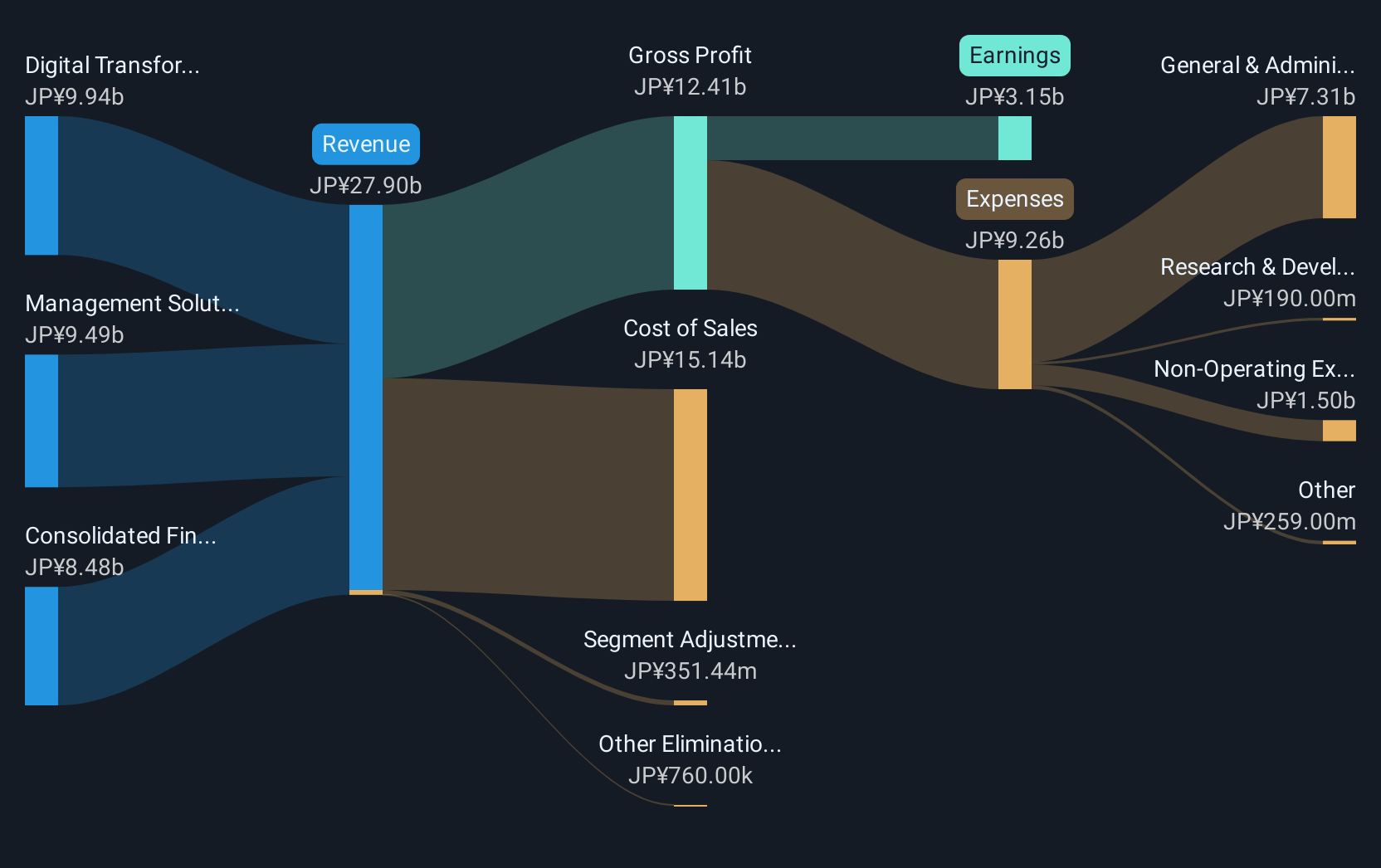

Overview: Avant Group Corporation, with a market cap of ¥73.09 billion, operates through its subsidiaries to offer accounting, business intelligence, and outsourcing services.

Operations: Avant Group generates revenue primarily from three segments: Group Governance Business (¥7.88 billion), Management Solutions Business (¥8.96 billion), and Digital Transformation Promotion Business (¥9.16 billion). The company's offerings focus on accounting, business intelligence, and outsourcing services through its subsidiaries.

Avant Group has showcased a robust growth trajectory, with an anticipated annual revenue increase of 15.8%, significantly outpacing the Japanese market's average of 4.2%. This performance is bolstered by earnings expected to rise by 18.1% annually, dwarfing the sector's norm of 7.8%. Notably, Avant’s commitment to innovation is evident from its R&D spending trends which align closely with these growth figures, ensuring the company remains at the forefront of technological advancements. Moreover, recent share repurchase activities underscore a strategic use of capital to enhance shareholder value; specifically, from July to November 2024, Avant repurchased shares worth ¥828.93 million under its buyback plan announced earlier in April. These financial maneuvers reflect not just growth but a calculated approach to maintaining market leadership and investor confidence amidst industry volatilities.

- Get an in-depth perspective on Avant Group's performance by reading our health report here.

Examine Avant Group's past performance report to understand how it has performed in the past.

Computer Modelling Group (TSX:CMG)

Simply Wall St Growth Rating: ★★★★☆☆

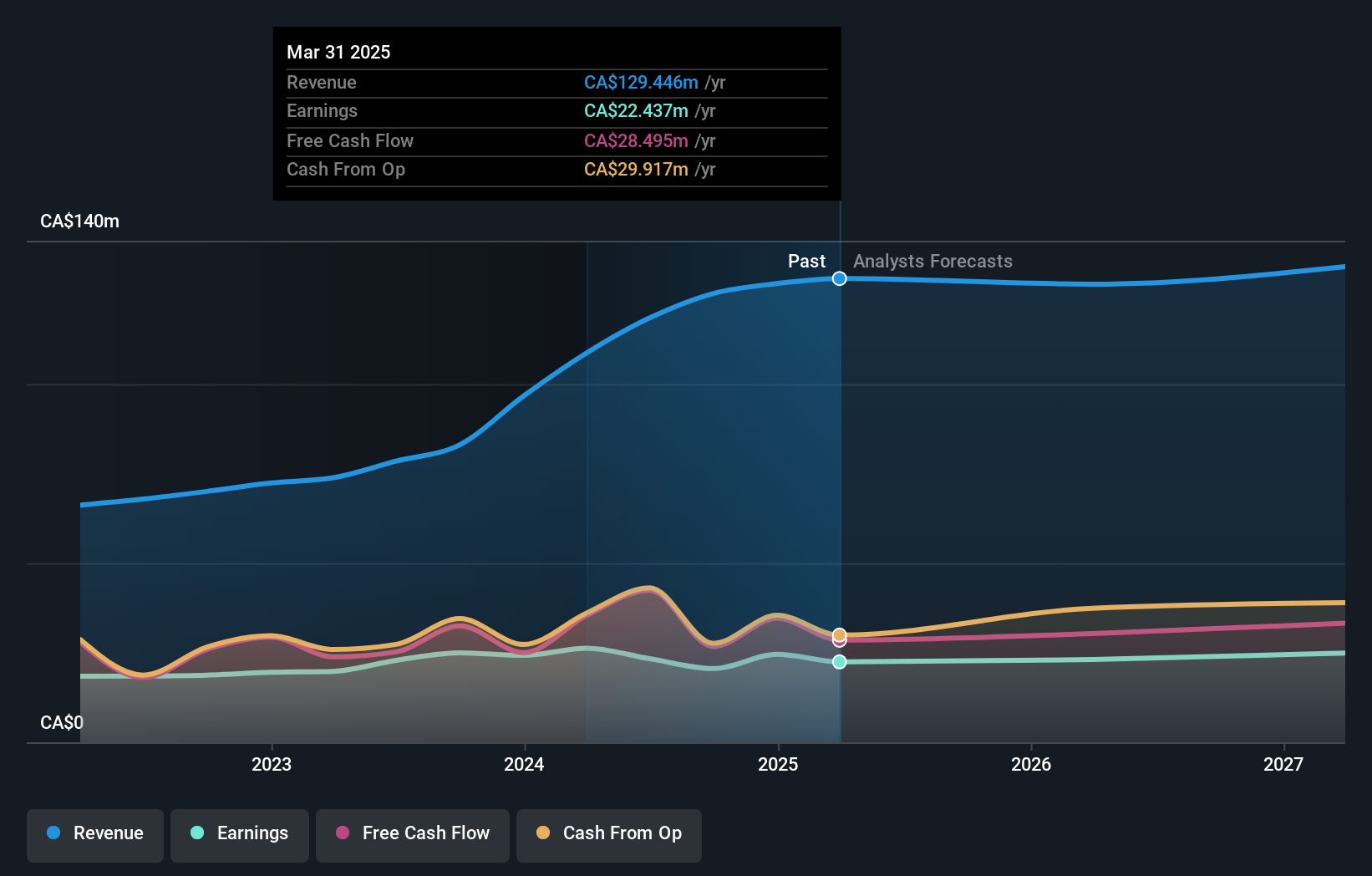

Overview: Computer Modelling Group Ltd. is a software and consulting technology company focused on developing and licensing reservoir simulation and seismic interpretation software, with a market cap of CA$892.15 million.

Operations: The company generates revenue primarily through the development and licensing of reservoir simulation and seismic interpretation software, with significant contributions from segments labeled BHV (CA$34.74 million) and CMG (CA$90.55 million).

Computer Modelling Group Ltd. (CMG) demonstrates a notable blend of financial and strategic growth, particularly in its collaboration with NVIDIA to enhance simulation solutions for energy efficiency and speed, crucial for sectors like oil, gas, and carbon capture storage. This partnership is expected to leverage NVIDIA's advanced GPUs and software stacks, potentially revolutionizing CMG’s product offerings while aligning with energy transition goals. Financially, CMG reported a revenue increase to CAD 59.99 million from CAD 43.38 million year-over-year in the first half of 2024, although net income dipped to CAD 7.73 million from CAD 13.42 million in the same period last year—an indicator of current investment phases possibly gearing towards future profitability through technological advancements and market expansion.

- Unlock comprehensive insights into our analysis of Computer Modelling Group stock in this health report.

Understand Computer Modelling Group's track record by examining our Past report.

Next Steps

- Access the full spectrum of 1267 High Growth Tech and AI Stocks by clicking on this link.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CMG

Computer Modelling Group

A software and consulting technology company, engages in the development and licensing of reservoir simulation and seismic interpretation software and related services.

Flawless balance sheet and good value.