Expert.ai (BIT:EXAI) Faces Deeper Losses Despite Revenue Forecasts of 18.9% Annual Growth

Reviewed by Simply Wall St

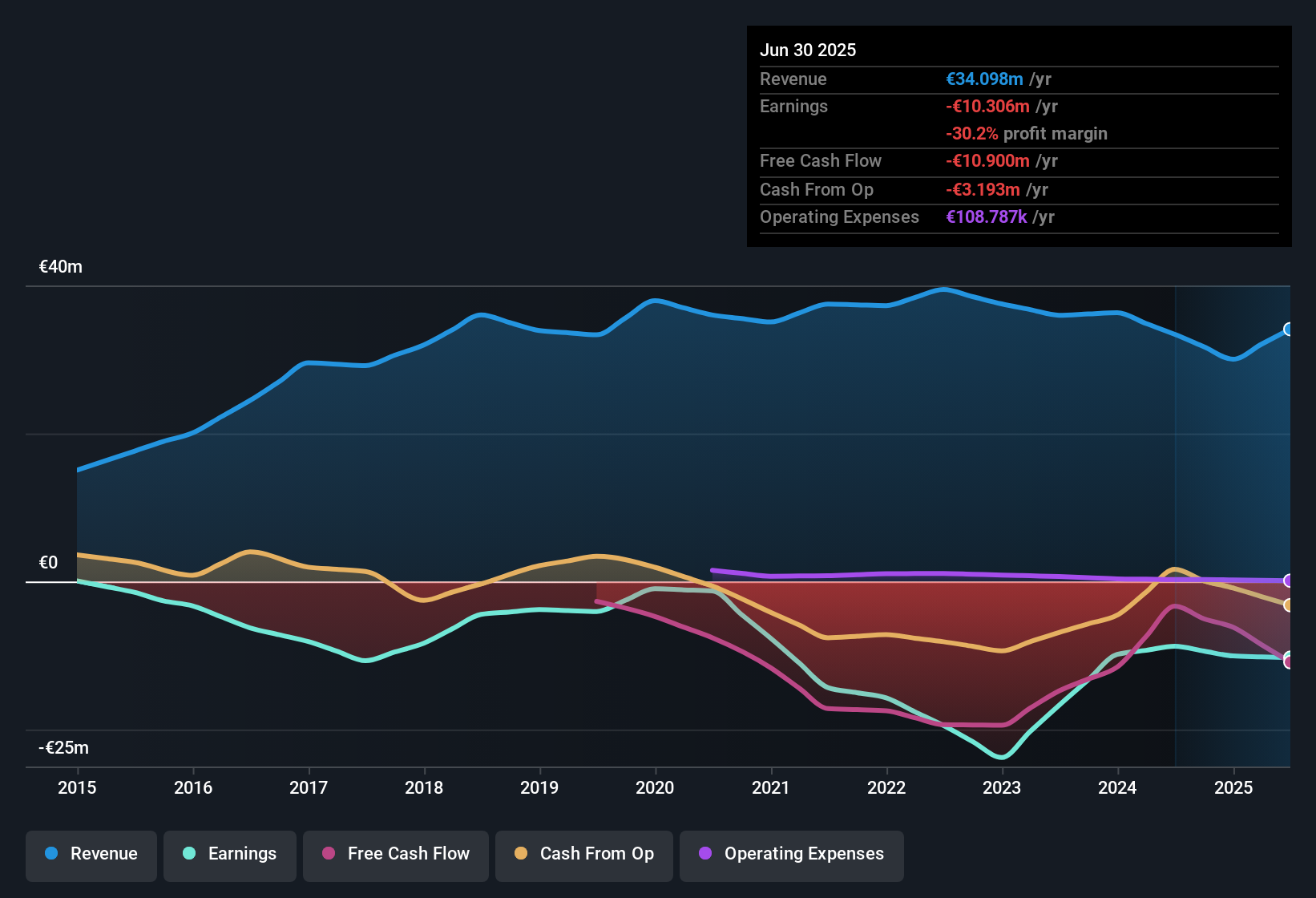

Expert.ai (BIT:EXAI) is forecasting revenue to grow at 18.9% per year, well ahead of the Italian market’s 4.9% annual pace. Earnings are projected to expand even faster at 120.76% annually. Despite these attractive growth forecasts, the company remains unprofitable, with net losses deepening at a yearly rate of 1.8% over the past five years. Its net profit margins have yet to show improvement. These results set the stage for a business with high expectations, but one that still faces near-term profitability issues and a premium valuation relative to peers.

See our full analysis for Expert.ai.The next section will put these headline figures head-to-head with the most widely followed narratives from across the market, highlighting where the consensus view is supported and where it runs into new realities.

Curious how numbers become stories that shape markets? Explore Community Narratives

Premium Price-to-Sales Stands Out

- Expert.ai trades at a Price-to-Sales ratio of 5.1x, well above the European software industry average of 2.2x and its closest peer group at 1.6x. This signals that investors are already paying a premium for its growth outlook.

- The prevailing market view expects this premium to hold if projected 18.9% annual revenue growth materializes.

- However, with net losses deepening by 1.8% per year, even optimistic scenarios must account for the costs of scaling up faster than the regional average.

- The current margin pressures provide less room for missteps compared to industry peers trading at much lower multiples.

Profitability Tipping Point Within Three Years

- Despite ongoing unprofitability, forecasts anticipate Expert.ai will reach profitability within the next three years, which is a pace considered above average for the Italian market’s technology sector.

- The prevailing market view sees rapid earnings expansion as a catalyst.

- Yet the lack of improvement in net profit margins so far tempers enthusiasm that this inflection is guaranteed in the near term.

- Investors weighing this timeline must balance high growth expectations against the risk that deeper losses could persist longer than anticipated.

DCF Fair Value vs. Current Price Creates Opportunity Gap

- The current share price of €1.57 sits meaningfully below a DCF fair value estimate of €2.62, suggesting a potential upside if aggressive growth targets are met.

- The prevailing market view highlights this valuation gap.

- Realizing this fair value depends on both achieving outsized growth and a successful pivot to sustained profitability.

- If Expert.ai underdelivers on either revenue expansion or profit improvement, this perceived undervaluation may quickly evaporate.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Expert.ai's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Expert.ai faces persistent losses and margin pressures, making its rapid revenue growth vulnerable if profitability remains elusive and costs continue to outpace expansion.

If you’re seeking steadier performance and less risk of erratic earnings, try stable growth stocks screener to discover companies delivering reliable growth through various market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Expert.ai might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:EXAI

Expert.ai

An artificial intelligence (AI) platform company, develops and sells cognitive computing software products based on AI algorithms to read and understand written language worldwide.

Excellent balance sheet with reasonable growth potential.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

CS Disco Stock: Legal AI Is Moving From Efficiency Tool to Competitive Necessity

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)