The latest analyst coverage could presage a bad day for Fiera Milano SpA (BIT:FM), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) estimates were cut sharply as the analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

Following the downgrade, the most recent consensus for Fiera Milano from its two analysts is for revenues of €135m in 2021 which, if met, would be a huge increase on its sales over the past 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 74% to €0.14. Yet prior to the latest estimates, the analysts had been forecasting revenues of €151m and losses of €0.12 per share in 2021. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

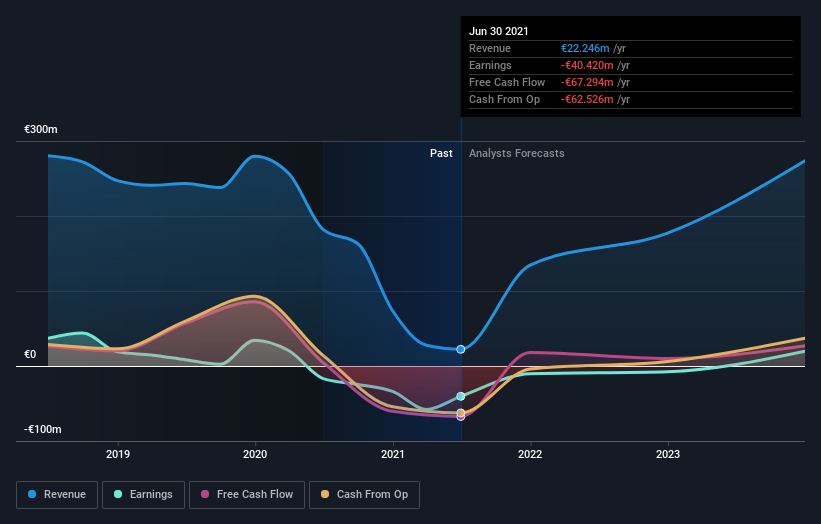

Check out our latest analysis for Fiera Milano

The consensus price target was broadly unchanged at €3.50, perhaps implicitly signalling that the weaker earnings outlook is not expected to have a long-term impact on the valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Fiera Milano at €3.60 per share, while the most bearish prices it at €3.40. This is a very narrow spread of estimates, implying either that Fiera Milano is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. For example, we noticed that Fiera Milano's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 5x growth to the end of 2021 on an annualised basis. That is well above its historical decline of 16% a year over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 8.2% annually. Not only are Fiera Milano's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at Fiera Milano. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of Fiera Milano.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading Fiera Milano or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BIT:FM

Fiera Milano

Fiera Milano SpA, together with its subsidiaries, organizes and hosts shows and international events and fairs in Italy and internationally.

Outstanding track record with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives