Advertisement

- Italy

- /

- Aerospace & Defense

- /

- BIT:OS

Officina Stellare S.p.A.'s (BIT:OS) Earnings Haven't Escaped The Attention Of Investors

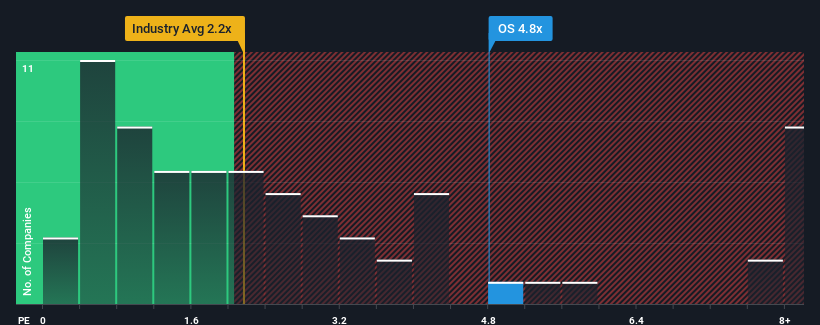

When close to half the companies in the Aerospace & Defense industry in Italy have price-to-sales ratios (or "P/S") below 1.5x, you may consider Officina Stellare S.p.A. (BIT:OS) as a stock to avoid entirely with its 4.8x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Officina Stellare

How Has Officina Stellare Performed Recently?

Officina Stellare certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. Perhaps the market is expecting future revenue performance to outperform the wider market, which has seemingly got people interested in the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Officina Stellare's earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The High P/S?

Officina Stellare's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Retrospectively, the last year delivered an exceptional 32% gain to the company's top line. Pleasingly, revenue has also lifted 148% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 15% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's understandable that Officina Stellare's P/S sits above the majority of other companies. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the wider industry.

The Bottom Line On Officina Stellare's P/S

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

It's no surprise that Officina Stellare can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Officina Stellare (at least 2 which make us uncomfortable), and understanding these should be part of your investment process.

If these risks are making you reconsider your opinion on Officina Stellare, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:OS

Officina Stellare

Designs, produces, and sells telescopes, and optical and aerospace instruments worldwide.

Slight with moderate growth potential.

Market Insights

Advertisement

Community Narratives

PPG Industries set to soar with 9% revenue growth in the next 3 years

Fair Value US$152.76|28.5% undervalued

DM

Community Contributor

Predicting a Steady Future for Crocs with Modest Growth and a 10% Discount Rate

Fair Value US$151.43|33.3% undervalued

JO

Community Contributor