Assessing Stellantis (BIT:STLAM) Valuation After Its Recent Share Price Rebound

Reviewed by Simply Wall St

Stellantis (BIT:STLAM) has quietly climbed about 12 % over the past month and roughly 23 % in the past 3 months, even though the shares are still down sharply year to date.

See our latest analysis for Stellantis.

Those gains mark a clear shift in sentiment, with the 30 day share price return now firmly positive even though the year to date share price performance and one year total shareholder return are still in the red. This suggests early momentum rather than a full turnaround.

If Stellantis has you rethinking the auto space, it is worth seeing what else is out there via auto manufacturers to compare potential opportunities.

With earnings still volatile but the stock trading at a hefty intrinsic discount, investors face a crucial question: is Stellantis genuinely undervalued right now, or is the market already pricing in its future growth?

Most Popular Narrative Narrative: 4.6% Overvalued

With Stellantis closing at €10.11 against a narrative fair value of about €9.66, the most followed view implies only a modest downside from here.

The analysts have a consensus price target of €9.442 for Stellantis based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €14.0, and the most bearish reporting a price target of just €6.0.

Want to see what kind of revenue climb and margin reset could justify this cautious upside case, and why opinions are so sharply split? The full narrative unpacks the exact profit path, the assumed earnings multiple and how long it might take for those expectations to show up in the share price.

Result: Fair Value of $9.66 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, lingering uncertainty around US tariffs and margin pressure from lower profitability on new EVs could quickly undermine this cautiously optimistic narrative.

Find out about the key risks to this Stellantis narrative.

Another Lens on Value

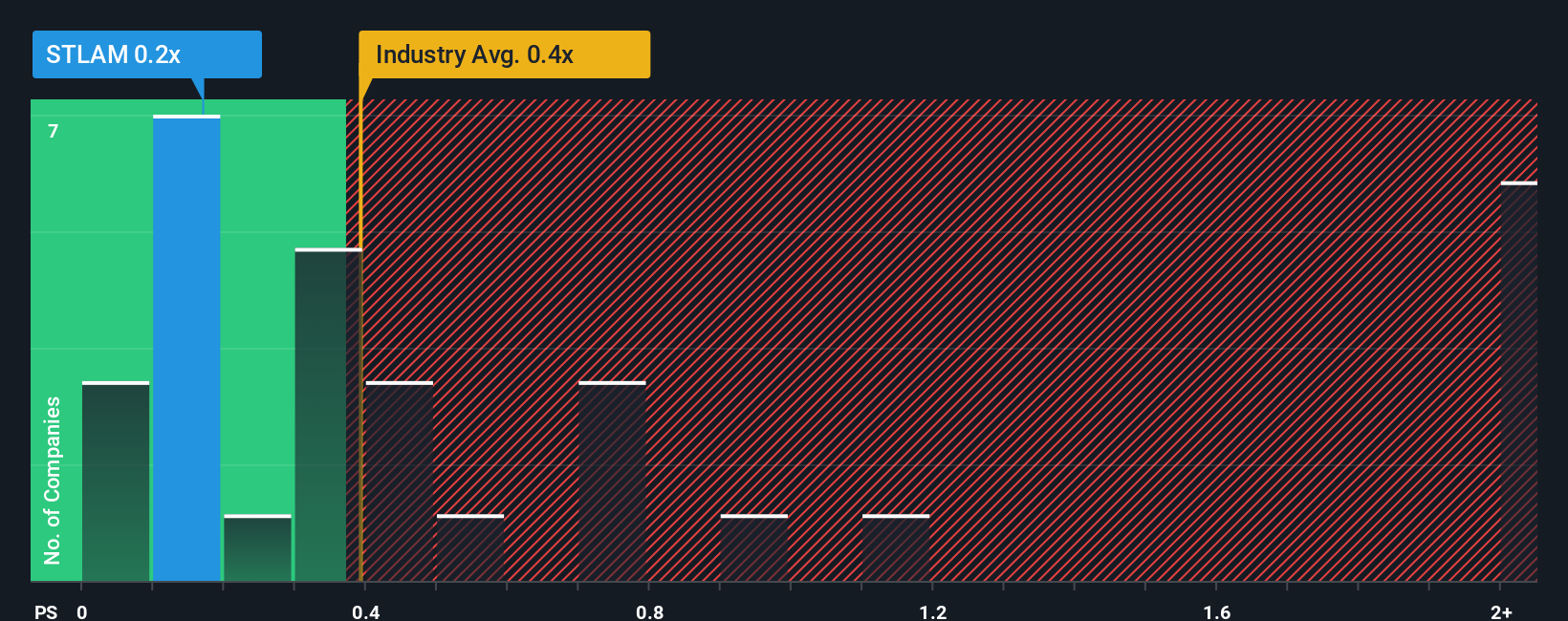

Step back from the narrative fair value and Stellantis looks very different on simple sales based metrics. At about 0.2 times sales, versus 0.4 times for the European auto sector and 0.4 times its own fair ratio, the market is heavily discounting the stock. Is that a margin of safety or a warning about future execution?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Stellantis Narrative

If you are not fully convinced by this view, or would rather explore the numbers yourself, you can build a fresh narrative in under three minutes: Do it your way.

A great starting point for your Stellantis research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep fresh ideas on their radar, so do not miss the chance to uncover new opportunities tailored to your strategy with our powerful screeners.

- Capture potential multi baggers early by scanning these 3625 penny stocks with strong financials where smaller names already show solid financial strength.

- Position yourself at the heart of the AI wave by targeting these 25 AI penny stocks that could benefit most as intelligent automation scales.

- Identify value focused opportunities by screening these 909 undervalued stocks based on cash flows that trade below what their cash flows suggest they are worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:STLAM

Stellantis

Engages in the design, engineering, manufacturing, distribution, and sale of automobiles and light commercial vehicles, engines, transmission systems, metallurgical products, mobility services, and production systems worldwide.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)