- India

- /

- Telecom Services and Carriers

- /

- NSEI:INDUSTOWER

Is Weakness In Indus Towers Limited (NSE:INDUSTOWER) Stock A Sign That The Market Could be Wrong Given Its Strong Financial Prospects?

Indus Towers (NSE:INDUSTOWER) has had a rough month with its share price down 13%. But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. Particularly, we will be paying attention to Indus Towers' ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for Indus Towers

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Indus Towers is:

23% = ₹66b ÷ ₹289b (Based on the trailing twelve months to June 2024).

The 'return' is the yearly profit. So, this means that for every ₹1 of its shareholder's investments, the company generates a profit of ₹0.23.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Indus Towers' Earnings Growth And 23% ROE

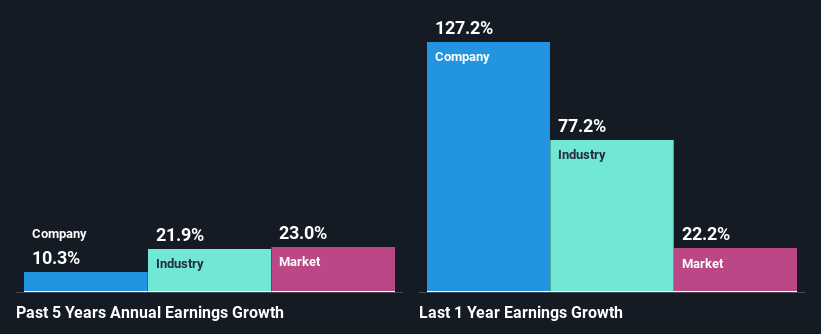

To begin with, Indus Towers seems to have a respectable ROE. Further, the company's ROE is similar to the industry average of 22%. This certainly adds some context to Indus Towers' moderate 10% net income growth seen over the past five years.

Next, on comparing with the industry net income growth, we found that Indus Towers' reported growth was lower than the industry growth of 22% over the last few years, which is not something we like to see.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Has the market priced in the future outlook for INDUSTOWER? You can find out in our latest intrinsic value infographic research report.

Is Indus Towers Making Efficient Use Of Its Profits?

While the company did pay out a portion of its dividend in the past, it currently doesn't pay a regular dividend. We infer that the company has been reinvesting all of its profits to grow its business.

Summary

On the whole, we feel that Indus Towers' performance has been quite good. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see a good amount of growth in its earnings. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INDUSTOWER

Indus Towers

A telecom infrastructure company, engages in the operation and maintenance of wireless communication towers and related infrastructures for various telecom service providers in India.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives