Ramco Systems Limited Beat Analyst Estimates: See What The Consensus Is Forecasting For Next Year

Ramco Systems Limited (NSE:RAMCOSYS) investors will be delighted, with the company turning in some strong numbers with its latest results. It was overall a positive result, with revenues beating expectations by 6.1% to hit ₹1.7b. Ramco Systems also reported a statutory profit of ₹5.84, which was an impressive 24% above what the analyst had forecast. The analyst typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what estimate suggests is in store for next year.

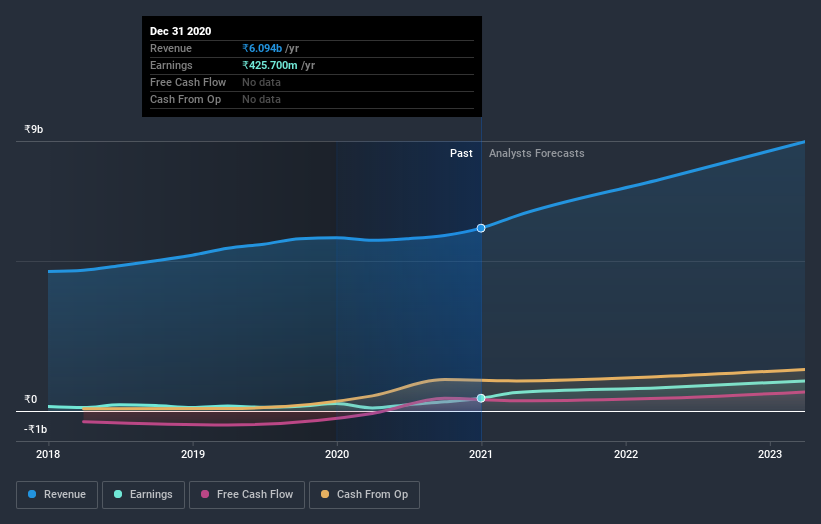

Check out our latest analysis for Ramco Systems

Taking into account the latest results, the most recent consensus for Ramco Systems from lone analyst is for revenues of ₹7.72b in 2022 which, if met, would be a sizeable 27% increase on its sales over the past 12 months. Per-share earnings are expected to shoot up 82% to ₹25.30. In the lead-up to this report, the analyst had been modelling revenues of ₹7.07b and earnings per share (EPS) of ₹22.30 in 2022. So it seems there's been a definite increase in optimism about Ramco Systems' future following the latest results, with a nice increase in the earnings per share forecasts in particular.

It will come as no surprise to learn that the analyst has increased their price target for Ramco Systems 8.1% to ₹600on the back of these upgrades.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Ramco Systems' rate of growth is expected to accelerate meaningfully, with the forecast 27% revenue growth noticeably faster than its historical growth of 7.2%p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 13% next year. It seems obvious that, while the growth outlook is brighter than the recent past, the analyst also expect Ramco Systems to grow faster than the wider industry.

The Bottom Line

The most important thing here is that the analyst upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Ramco Systems following these results. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analyst clearly feeling that the intrinsic value of the business is improving.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Ramco Systems , and understanding these should be part of your investment process.

If you’re looking to trade Ramco Systems, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:RAMCOSYS

Ramco Systems

Operates as an enterprise software company in the United States, Europe, the Asia-Pacific, India, and the Middle East, and Africa.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)