Advertisement

LTIMindtree (NSE:LTIM) Is Paying Out A Larger Dividend Than Last Year

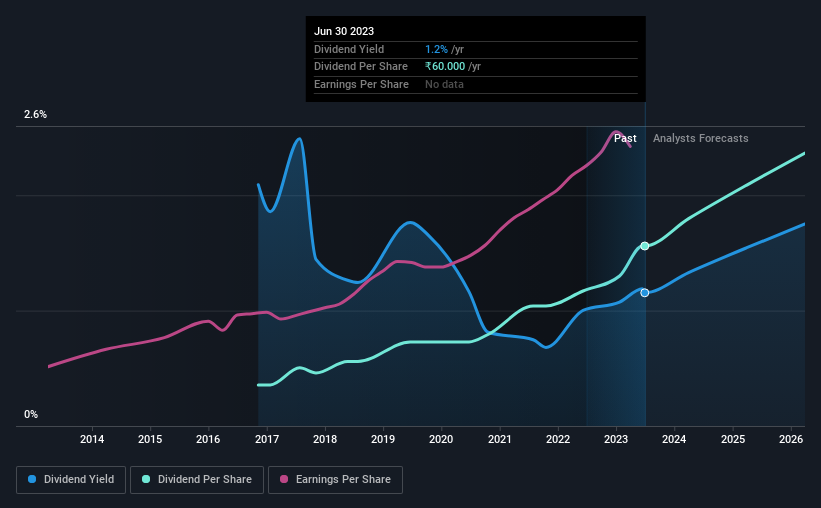

LTIMindtree Limited (NSE:LTIM) has announced that it will be increasing its dividend from last year's comparable payment on the 16th of August to ₹40.00. This takes the annual payment to 1.2% of the current stock price, which unfortunately is below what the industry is paying.

See our latest analysis for LTIMindtree

LTIMindtree's Earnings Easily Cover The Distributions

Even a low dividend yield can be attractive if it is sustained for years on end. Prior to this announcement, LTIMindtree was quite comfortably covering its dividend with earnings and it was paying more than 75% of its free cash flow to shareholders. By paying out so much of its cash flows, this could indicate that the company has limited opportunities for investment and growth.

Looking forward, earnings per share is forecast to rise by 63.4% over the next year. If the dividend continues on this path, the payout ratio could be 27% by next year, which we think can be pretty sustainable going forward.

LTIMindtree's Dividend Has Lacked Consistency

Looking back, LTIMindtree's dividend hasn't been particularly consistent. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. The dividend has gone from an annual total of ₹13.70 in 2016 to the most recent total annual payment of ₹60.00. This implies that the company grew its distributions at a yearly rate of about 23% over that duration. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. LTIMindtree has seen EPS rising for the last five years, at 18% per annum. Since earnings per share is growing at an acceptable rate, and the payout policy is balanced, we think the company is positioning itself well to grow earnings and dividends in the future.

An additional note is that the company has been raising capital by issuing stock equal to 69% of shares outstanding in the last 12 months. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think LTIMindtree's payments are rock solid. The company hasn't been paying a very consistent dividend over time, despite only paying out a small portion of earnings. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've identified 4 warning signs for LTIMindtree (2 are significant!) that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:LTIM

LTIMindtree

A technology consulting and digital solutions company, provides information technology services and solutions in India, North America, Europe, and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

PPG Industries set to soar with 9% revenue growth in the next 3 years

Fair Value US$152.76|24.9% undervalued

DM

Community Contributor

Predicting a Steady Future for Crocs with Modest Growth and a 10% Discount Rate

Fair Value US$151.43|33.2% undervalued

JO

Community Contributor