Advertisement

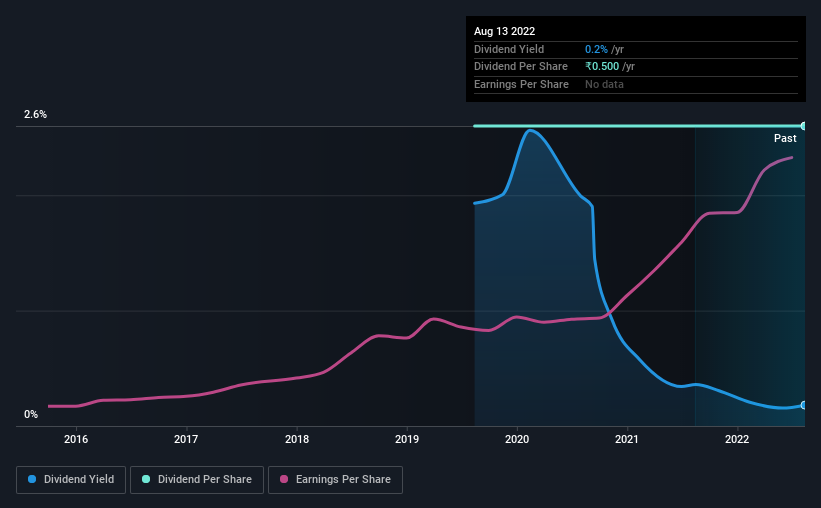

Dynacons Systems & Solutions Limited's (NSE:DSSL) investors are due to receive a payment of ₹0.50 per share on 9th of September. Including this payment, the dividend yield on the stock will be 0.2%, which is a modest boost for shareholders' returns.

Check out our latest analysis for Dynacons Systems & Solutions

Dynacons Systems & Solutions' Dividend Is Well Covered By Earnings

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Based on the last payment, Dynacons Systems & Solutions was earning enough to cover the dividend, but free cash flows weren't positive. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

If the trend of the last few years continues, EPS will grow by 44.8% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio will be 2.2%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dynacons Systems & Solutions Is Still Building Its Track Record

The company has maintained a consistent dividend for a few years now, but we would like to see a longer track record before relying on it. The payments haven't really changed that much since 3 years ago. Modest dividend growth is good to see, especially with the payments being relatively stable. However, the payment history is relatively short and we wouldn't want to rely on this dividend too much.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Dynacons Systems & Solutions has seen EPS rising for the last five years, at 45% per annum. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

An additional note is that the company has been raising capital by issuing stock equal to 11% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

In Summary

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Dynacons Systems & Solutions' payments, as there could be some issues with sustaining them into the future. While Dynacons Systems & Solutions is earning enough to cover the payments, the cash flows are lacking. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 3 warning signs for Dynacons Systems & Solutions (of which 1 doesn't sit too well with us!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:DSSL

Dynacons Systems & Solutions

Provides IT solutions and related services in India and internationally.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

37 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

42 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

AD

Addu0g on iShares Gold Trust ·

iShares Gold Trust will Boost Future PE by 2.7% over Five Years

Fair Value:US$10324.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on Sipef ·

Why I Invest in SIPEF?

Fair Value:€12125.5% undervalued

13 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on Kucingko Berhad ·

Kucingko Berhad: Fundamentals Show Early Recovery as Creative Content Expansion Gains Traction

Fair Value:RM 0.012733.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

AN

andre_k1tsg on Companhia de Saneamento de Minas Gerais ·

Eu André José Julião digo o caminho da melhorar a toda população esta entrando no trilhos.

0

|0