CyberTech Systems and Software Limited (NSE:CYBERTECH) Looks Like A Good Stock, And It's Going Ex-Dividend Soon

CyberTech Systems and Software Limited (NSE:CYBERTECH) is about to trade ex-dividend in the next 3 days. You will need to purchase shares before the 19th of September to receive the dividend, which will be paid on the 25th of October.

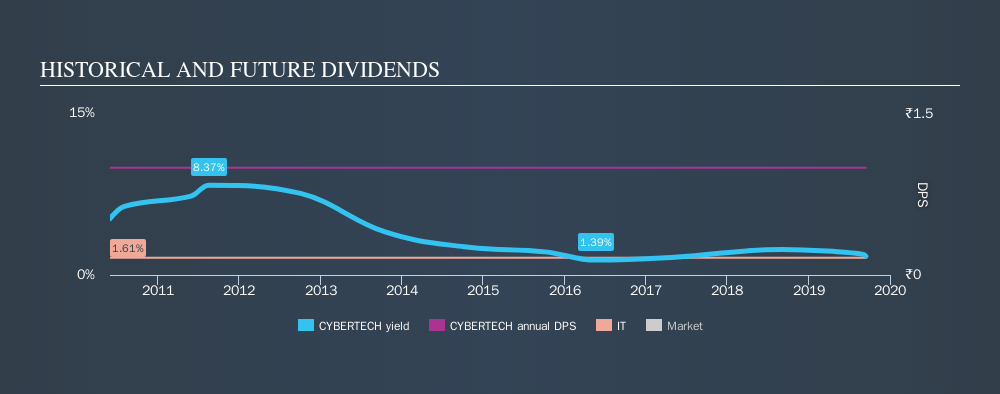

CyberTech Systems and Software's upcoming dividend is ₹1.00 a share, following on from the last 12 months, when the company distributed a total of ₹1.00 per share to shareholders. Based on the last year's worth of payments, CyberTech Systems and Software stock has a trailing yield of around 1.7% on the current share price of ₹57. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

See our latest analysis for CyberTech Systems and Software

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. CyberTech Systems and Software is paying out just 21% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. What's good is that dividends were well covered by free cash flow, with the company paying out 23% of its cash flow last year.

It's positive to see that CyberTech Systems and Software's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit CyberTech Systems and Software paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Fortunately for readers, CyberTech Systems and Software's earnings per share have been growing at 10% a year for the past five years. Earnings per share have been growing rapidly and the company is retaining a majority of its earnings within the business. This will make it easier to fund future growth efforts and we think this is an attractive combination - plus the dividend can always be increased later.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. CyberTech Systems and Software's dividend payments are effectively flat on where they were nine years ago.

The Bottom Line

Should investors buy CyberTech Systems and Software for the upcoming dividend? CyberTech Systems and Software has been growing earnings at a rapid rate, and has a conservatively low payout ratio, implying that it is reinvesting heavily in its business; a sterling combination. CyberTech Systems and Software looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

Want to learn more about CyberTech Systems and Software? Here's a visualisation of its historical rate of revenue and earnings growth.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:CYBERTECH

CyberTech Systems and Software

Provides geospatial, networking, and enterprise information technology solutions in India and the United States.

Flawless balance sheet 6 star dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)