How Does IntraSoft Technologies's (NSE:ISFT) P/E Compare To Its Industry, After Its Big Share Price Gain?

IntraSoft Technologies (NSE:ISFT) shareholders are no doubt pleased to see that the share price has bounced 54% in the last month alone, although it is still down 61% over the last quarter. But that will do little to salve the savage burn caused by the 72% share price decline, over the last year.

All else being equal, a sharp share price increase should make a stock less attractive to potential investors. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. The implication here is that deep value investors might steer clear when expectations of a company are too high. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). Investors have optimistic expectations of companies with higher P/E ratios, compared to companies with lower P/E ratios.

View our latest analysis for IntraSoft Technologies

How Does IntraSoft Technologies's P/E Ratio Compare To Its Peers?

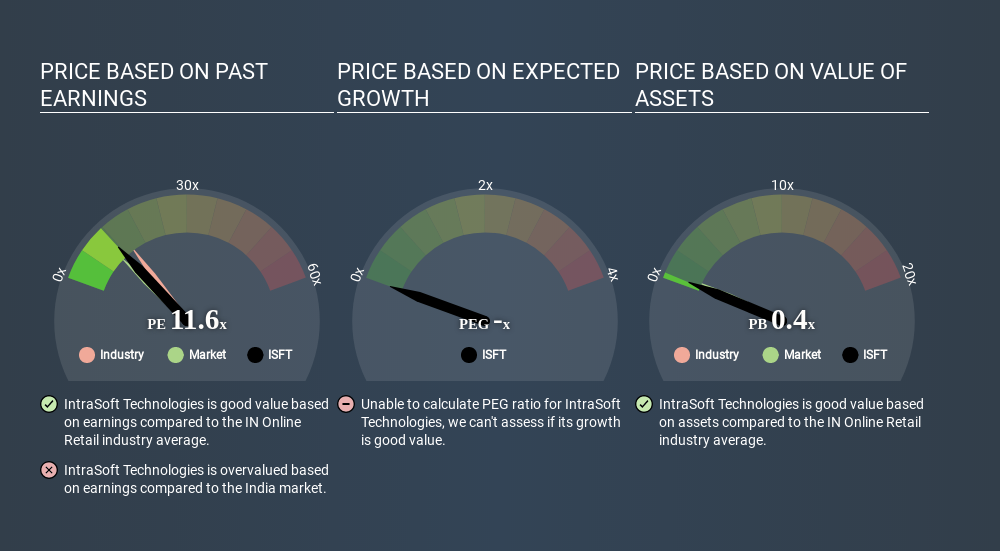

We can tell from its P/E ratio of 11.64 that sentiment around IntraSoft Technologies isn't particularly high. We can see in the image below that the average P/E (14.2) for companies in the online retail industry is higher than IntraSoft Technologies's P/E.

Its relatively low P/E ratio indicates that IntraSoft Technologies shareholders think it will struggle to do as well as other companies in its industry classification. Since the market seems unimpressed with IntraSoft Technologies, it's quite possible it could surprise on the upside. If you consider the stock interesting, further research is recommended. For example, I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

When earnings fall, the 'E' decreases, over time. That means even if the current P/E is low, it will increase over time if the share price stays flat. Then, a higher P/E might scare off shareholders, pushing the share price down.

IntraSoft Technologies had pretty flat EPS growth in the last year. And it has shrunk its earnings per share by 8.2% per year over the last five years. So we might expect a relatively low P/E.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

Don't forget that the P/E ratio considers market capitalization. That means it doesn't take debt or cash into account. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

How Does IntraSoft Technologies's Debt Impact Its P/E Ratio?

IntraSoft Technologies has net debt worth 14% of its market capitalization. This could bring some additional risk, and reduce the number of investment options for management; worth remembering if you compare its P/E to businesses without debt.

The Bottom Line On IntraSoft Technologies's P/E Ratio

IntraSoft Technologies has a P/E of 11.6. That's higher than the average in its market, which is 10.3. Given the debt is only modest, and earnings are already moving in the right direction, it's not surprising that the market expects continued improvement. What is very clear is that the market has become more optimistic about IntraSoft Technologies over the last month, with the P/E ratio rising from 7.6 back then to 11.6 today. For those who prefer to invest with the flow of momentum, that might mean it's time to put the stock on a watchlist, or research it. But the contrarian may see it as a missed opportunity.

Investors should be looking to buy stocks that the market is wrong about. If the reality for a company is better than it expects, you can make money by buying and holding for the long term. Although we don't have analyst forecasts you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:ISFT

IntraSoft Technologies

Through its subsidiaries, engages in the development and delivery of e-commerce and e-cards through internet platform in India and internationally.

Excellent balance sheet and slightly overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)