Laurus Labs Limited Just Recorded A 7.2% EPS Beat: Here's What Analysts Are Forecasting Next

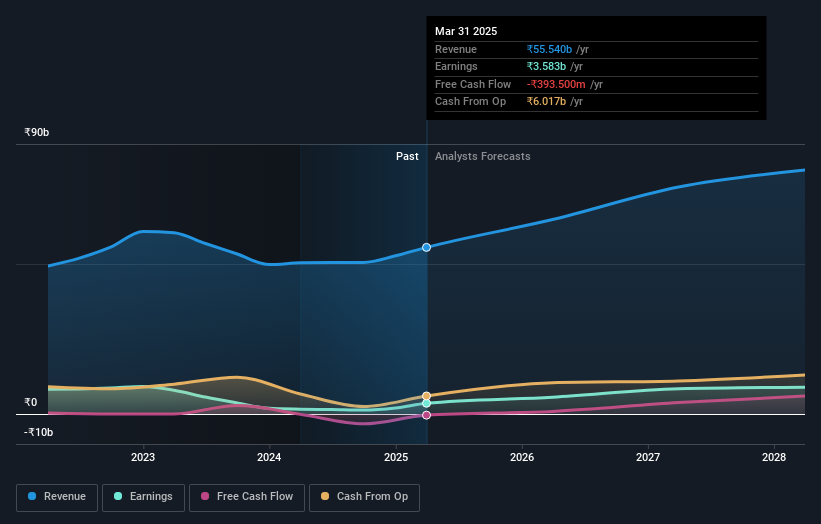

Laurus Labs Limited (NSE:LAURUSLABS) last week reported its latest yearly results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. The result was positive overall - although revenues of ₹56b were in line with what the analysts predicted, Laurus Labs surprised by delivering a statutory profit of ₹6.64 per share, modestly greater than expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Taking into account the latest results, the most recent consensus for Laurus Labs from 13 analysts is for revenues of ₹64.8b in 2026. If met, it would imply a notable 17% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to bounce 60% to ₹10.60. Yet prior to the latest earnings, the analysts had been anticipated revenues of ₹64.6b and earnings per share (EPS) of ₹10.88 in 2026. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a small dip in their earnings per share forecasts.

See our latest analysis for Laurus Labs

Althoughthe analysts have revised their earnings forecasts for next year, they've also lifted the consensus price target 8.3% to ₹565, suggesting the revised estimates are not indicative of a weaker long-term future for the business. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Laurus Labs at ₹750 per share, while the most bearish prices it at ₹293. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Laurus Labs' rate of growth is expected to accelerate meaningfully, with the forecast 17% annualised revenue growth to the end of 2026 noticeably faster than its historical growth of 7.2% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 11% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Laurus Labs to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Laurus Labs. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for Laurus Labs going out to 2028, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Laurus Labs that you should be aware of.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:LAURUSLABS

Laurus Labs

Manufactures and sells medicines and active pharmaceutical ingredients (APIs) in India and internationally.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion