- India

- /

- Paper and Forestry Products

- /

- NSEI:WSTCSTPAPR

Does West Coast Paper Mills's (NSE:WSTCSTPAPR) Statutory Profit Adequately Reflect Its Underlying Profit?

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. Today we'll focus on whether this year's statutory profits are a good guide to understanding West Coast Paper Mills (NSE:WSTCSTPAPR).

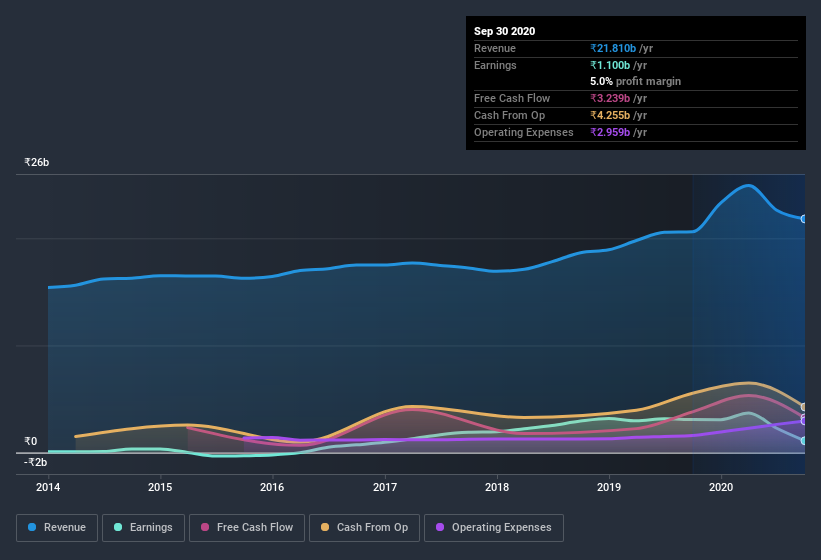

We like the fact that West Coast Paper Mills made a profit of ₹1.10b on its revenue of ₹21.8b, in the last year. As you can see in the chart below, its profit has declined over the last three years, even though its revenue has increased.

View our latest analysis for West Coast Paper Mills

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. So today we'll look at what West Coast Paper Mills' cashflow, tax benefits and unusual items tell us about the quality of its earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of West Coast Paper Mills.

A Closer Look At West Coast Paper Mills' Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

West Coast Paper Mills has an accrual ratio of -0.14 for the year to September 2020. That indicates that its free cash flow was a fair bit more than its statutory profit. Indeed, in the last twelve months it reported free cash flow of ₹3.2b, well over the ₹1.10b it reported in profit. West Coast Paper Mills did see its free cash flow drop year on year, which is less than ideal, like a Simpson's episode without Groundskeeper Willie. Having said that it seems that a recent tax benefit and some unusual items have impacted its profit (and this its accrual ratio).

The Impact Of Unusual Items On Profit

While the accrual ratio might bode well, we also note that West Coast Paper Mills' profit was boosted by unusual items worth ₹208m in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

An Unusual Tax Situation

Moving on from the accrual ratio, we note that West Coast Paper Mills profited from a tax benefit which contributed ₹605m to profit. It's always a bit noteworthy when a company is paid by the tax man, rather than paying the tax man. Of course, prima facie it's great to receive a tax benefit. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth.

Our Take On West Coast Paper Mills' Profit Performance

Summing up, West Coast Paper Mills' accrual ratio suggests that its statutory earnings are well matched by free cash flow while its unusual items and tax benefit is boosted profit in a way that may not be sustained. Based on these factors, we think that West Coast Paper Mills' statutory profits probably make it seem better than it is on an underlying level. If you want to do dive deeper into West Coast Paper Mills, you'd also look into what risks it is currently facing. For example, we've discovered 3 warning signs that you should run your eye over to get a better picture of West Coast Paper Mills.

Our examination of West Coast Paper Mills has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you decide to trade West Coast Paper Mills, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade West Coast Paper Mills, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if West Coast Paper Mills might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:WSTCSTPAPR

West Coast Paper Mills

Manufactures, produces and sells pulp, paper, and paper boards in India.

Flawless balance sheet average dividend payer.

Market Insights

Community Narratives