- India

- /

- Basic Materials

- /

- NSEI:ULTRACEMCO

UltraTech Cement's (NSE:ULTRACEMCO) Dividend Will Be Increased To ₹70.00

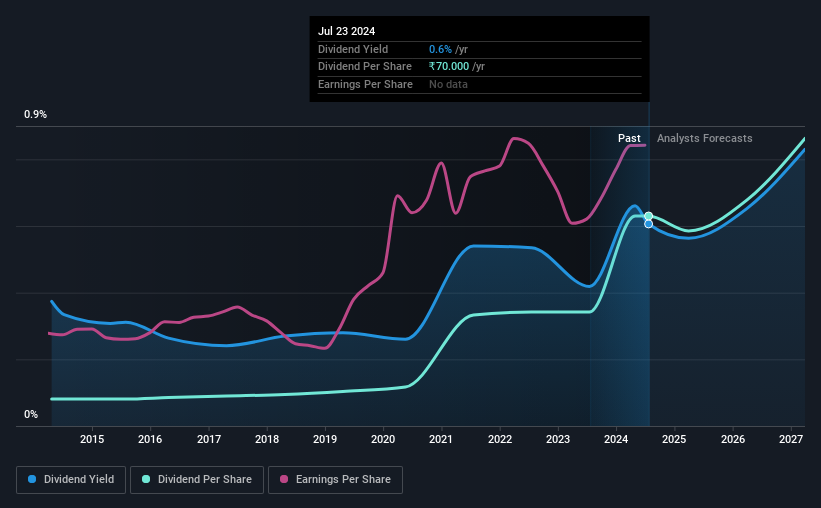

UltraTech Cement Limited's (NSE:ULTRACEMCO) dividend will be increasing from last year's payment of the same period to ₹70.00 on 13th of September. This makes the dividend yield 0.6%, which is above the industry average.

Check out our latest analysis for UltraTech Cement

UltraTech Cement's Payment Has Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Based on the last payment, UltraTech Cement was paying only paying out a fraction of earnings, but the payment was a massive 107% of cash flows. A cash payout ratio this high could put the dividend under pressure and force the company to reduce it in the future if it were to run into tough times.

The next year is set to see EPS grow by 66.1%. If the dividend continues along recent trends, we estimate the payout ratio will be 21%, which is in the range that makes us comfortable with the sustainability of the dividend.

UltraTech Cement Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of ₹9.00 in 2014 to the most recent total annual payment of ₹70.00. This means that it has been growing its distributions at 23% per annum over that time. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Looks Likely To Grow

The company's investors will be pleased to have been receiving dividend income for some time. We are encouraged to see that UltraTech Cement has grown earnings per share at 17% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for UltraTech Cement's prospects of growing its dividend payments in the future.

Our Thoughts On UltraTech Cement's Dividend

In summary, while it's always good to see the dividend being raised, we don't think UltraTech Cement's payments are rock solid. While UltraTech Cement is earning enough to cover the payments, the cash flows are lacking. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 1 warning sign for UltraTech Cement that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:ULTRACEMCO

UltraTech Cement

Primarily engages in the manufacture and sale of clinker, cement, and related products in India.

Solid track record with excellent balance sheet and pays a dividend.