Advertisement

Is Privi Speciality Chemicals (NSE:PRIVISCL) A Risky Investment?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Privi Speciality Chemicals Limited (NSE:PRIVISCL) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

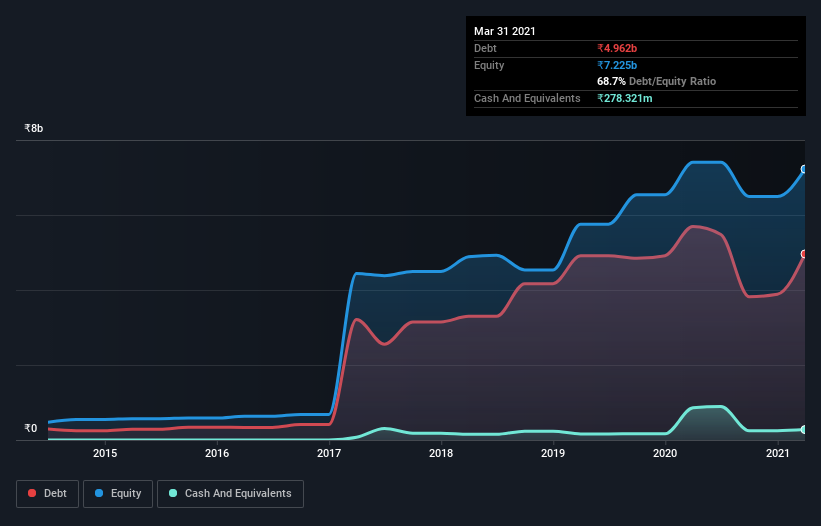

Check out our latest analysis for Privi Speciality Chemicals

What Is Privi Speciality Chemicals's Net Debt?

As you can see below, Privi Speciality Chemicals had ₹4.96b of debt at March 2021, down from ₹5.69b a year prior. However, it does have ₹278.3m in cash offsetting this, leading to net debt of about ₹4.68b.

How Strong Is Privi Speciality Chemicals' Balance Sheet?

According to the last reported balance sheet, Privi Speciality Chemicals had liabilities of ₹4.54b due within 12 months, and liabilities of ₹3.64b due beyond 12 months. Offsetting this, it had ₹278.3m in cash and ₹2.39b in receivables that were due within 12 months. So it has liabilities totalling ₹5.51b more than its cash and near-term receivables, combined.

Given Privi Speciality Chemicals has a market capitalization of ₹42.8b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Privi Speciality Chemicals's net debt is sitting at a very reasonable 2.3 times its EBITDA, while its EBIT covered its interest expense just 6.4 times last year. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. Shareholders should be aware that Privi Speciality Chemicals's EBIT was down 34% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Privi Speciality Chemicals's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Privi Speciality Chemicals burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

On the face of it, Privi Speciality Chemicals's conversion of EBIT to free cash flow left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to cover its interest expense with its EBIT isn't such a worry. Overall, we think it's fair to say that Privi Speciality Chemicals has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for Privi Speciality Chemicals that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Privi Speciality Chemicals, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:PRIVISCL

Privi Speciality Chemicals

Operates as a manufacturer, supplier, and exporter of aroma and fragrance chemicals in India, North America, Asia, the Middle East, Africa, Europe, South America, and the United Kingdom.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor