Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:NATIONALUM

The total return for National Aluminium (NSE:NATIONALUM) investors has risen faster than earnings growth over the last five years

It hasn't been the best quarter for National Aluminium Company Limited (NSE:NATIONALUM) shareholders, since the share price has fallen 27% in that time. But that doesn't change the fact that the returns over the last half decade have been spectacular. Indeed, the share price is up a whopping 417% in that time. So it might be that some shareholders are taking profits after good performance. The most important thing for savvy investors to consider is whether the underlying business can justify the share price gain.

In light of the stock dropping 3.4% in the past week, we want to investigate the longer term story, and see if fundamentals have been the driver of the company's positive five-year return.

See our latest analysis for National Aluminium

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

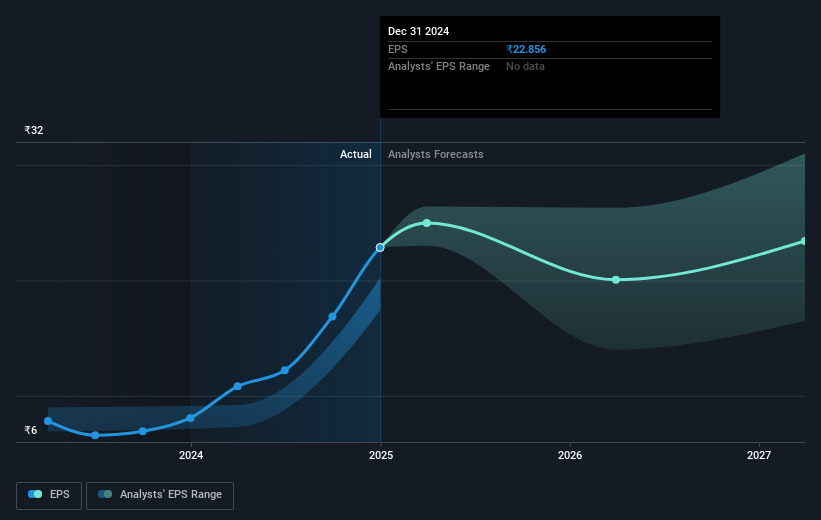

During five years of share price growth, National Aluminium achieved compound earnings per share (EPS) growth of 74% per year. The EPS growth is more impressive than the yearly share price gain of 39% over the same period. So one could conclude that the broader market has become more cautious towards the stock. This cautious sentiment is reflected in its (fairly low) P/E ratio of 7.91.

You can see how EPS has changed over time in the image below (click on the chart to see the exact values).

We know that National Aluminium has improved its bottom line lately, but is it going to grow revenue? You could check out this free report showing analyst revenue forecasts.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. We note that for National Aluminium the TSR over the last 5 years was 564%, which is better than the share price return mentioned above. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

It's nice to see that National Aluminium shareholders have received a total shareholder return of 25% over the last year. And that does include the dividend. Having said that, the five-year TSR of 46% a year, is even better. The pessimistic view would be that be that the stock has its best days behind it, but on the other hand the price might simply be moderating while the business itself continues to execute. It's always interesting to track share price performance over the longer term. But to understand National Aluminium better, we need to consider many other factors. Like risks, for instance. Every company has them, and we've spotted 2 warning signs for National Aluminium (of which 1 is concerning!) you should know about.

For those who like to find winning investments this free list of undervalued companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Indian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if National Aluminium might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NATIONALUM

National Aluminium

Engages in the manufacture and sale of alumina and aluminum products in India and internationally.

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|72.3% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|35.0% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|1.3% undervalued

BL

Community Contributor