- India

- /

- Basic Materials

- /

- NSEI:MANGLMCEM

Does Mangalam Cement (NSE:MANGLMCEM) Deserve A Spot On Your Watchlist?

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Mangalam Cement (NSE:MANGLMCEM). While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

See our latest analysis for Mangalam Cement

How Fast Is Mangalam Cement Growing Its Earnings Per Share?

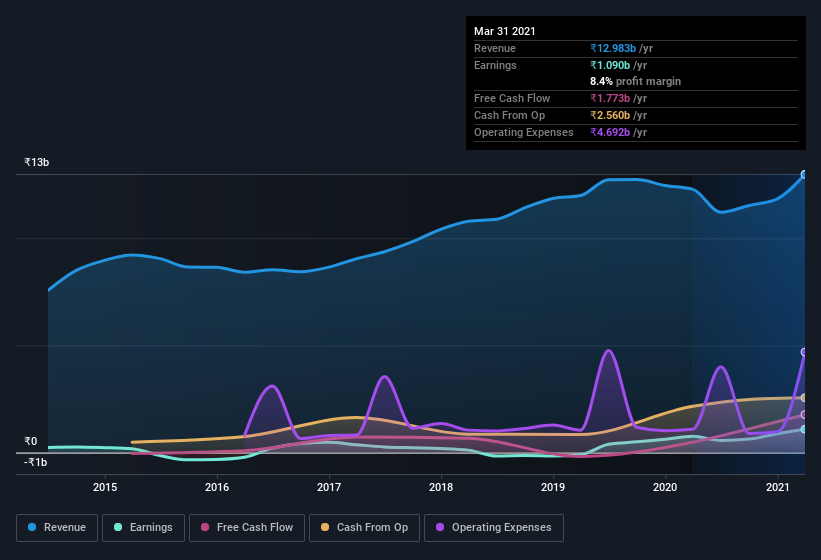

Over the last three years, Mangalam Cement has grown earnings per share (EPS) like young bamboo after rain; fast, and from a low base. So I don't think the percent growth rate is particularly meaningful. Thus, it makes sense to focus on more recent growth rates, instead. Like a wedge-tailed eagle on the wind, Mangalam Cement's EPS soared from ₹28.43 to ₹40.83, in just one year. That's a impressive gain of 44%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The good news is that Mangalam Cement is growing revenues, and EBIT margins improved by 3.1 percentage points to 15%, over the last year. Ticking those two boxes is a good sign of growth, in my book.

In the chart below, you can see how the company has grown earnings, and revenue, over time. Click on the chart to see the exact numbers.

Mangalam Cement isn't a huge company, given its market capitalization of ₹8.3b. That makes it extra important to check on its balance sheet strength.

Are Mangalam Cement Insiders Aligned With All Shareholders?

Like that fresh smell in the air when the rains are coming, insider buying fills me with optimistic anticipation. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Not only did Mangalam Cement insiders refrain from selling stock during the year, but they also spent ₹14m buying it. That's nice to see, because it suggests insiders are optimistic. It is also worth noting that it was Executive Co-Chairperson Anshuman Jalan who made the biggest single purchase, worth ₹5.3m, paying ₹178 per share.

On top of the insider buying, it's good to see that Mangalam Cement insiders have a valuable investment in the business. To be specific, they have ₹1.4b worth of shares. That's a lot of money, and no small incentive to work hard. That amounts to 17% of the company, demonstrating a degree of high-level alignment with shareholders.

Does Mangalam Cement Deserve A Spot On Your Watchlist?

For growth investors like me, Mangalam Cement's raw rate of earnings growth is a beacon in the night. On top of that, insiders own a significant stake in the company and have been buying more shares. So it's fair to say I think this stock may well deserve a spot on your watchlist. Still, you should learn about the 2 warning signs we've spotted with Mangalam Cement .

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Mangalam Cement, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you’re looking to trade Mangalam Cement, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Mangalam Cement, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:MANGLMCEM

Mangalam Cement

Manufactures and sells cement and clinker primarily in India.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives