Exploring Jammu and Kashmir Bank And Two More Undiscovered Gems in India

Reviewed by Simply Wall St

The Indian market has shown robust growth, rising by 1.1% over the last week and an impressive 45% over the past 12 months, with earnings expected to grow by 16% annually. In such a thriving environment, uncovering lesser-known stocks like Jammu and Kashmir Bank can offer unique opportunities for investors looking to diversify their portfolios.

Top 10 Undiscovered Gems With Strong Fundamentals In India

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Pearl Global Industries | 54.72% | 19.34% | 38.59% | ★★★★★★ |

| Goldiam International | NA | 10.09% | 16.51% | ★★★★★★ |

| Le Travenues Technology | 8.99% | 36.48% | 63.83% | ★★★★★★ |

| Timex Group India | 2.24% | 16.39% | 61.31% | ★★★★★★ |

| Indo Tech Transformers | 2.30% | 20.60% | 62.92% | ★★★★★☆ |

| Avantel | 7.01% | 35.59% | 35.41% | ★★★★★☆ |

| Spright Agro | 0.58% | 83.13% | 86.22% | ★★★★★☆ |

| Nibe | 33.91% | 81.20% | 80.04% | ★★★★★☆ |

| Monarch Networth Capital | 32.66% | 30.99% | 50.24% | ★★★★☆☆ |

| Innovana Thinklabs | 4.53% | 12.52% | 19.93% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

Jammu and Kashmir Bank (NSEI:J&KBANK)

Simply Wall St Value Rating: ★★★★☆☆

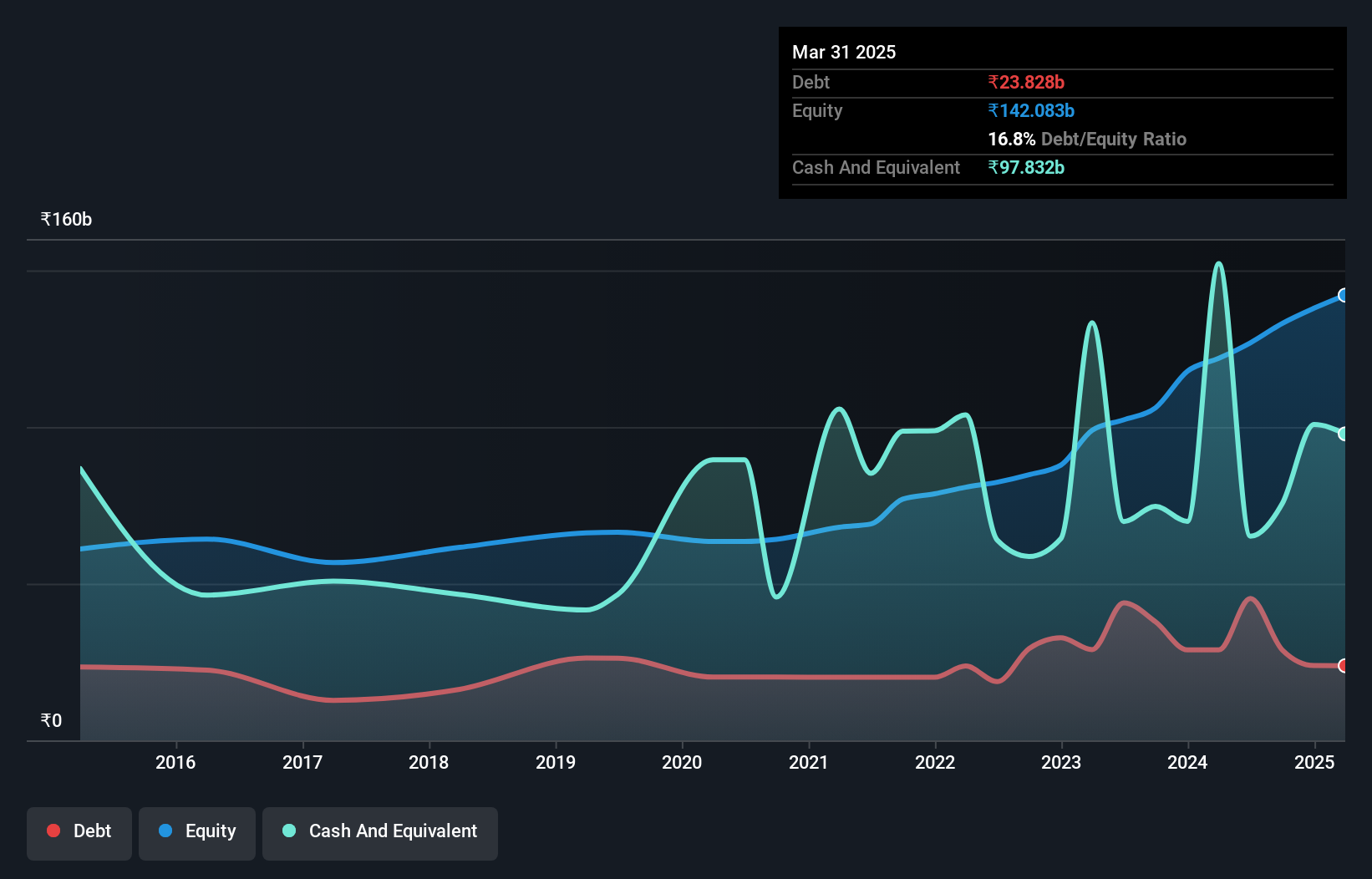

Overview: Jammu and Kashmir Bank Limited operates as a comprehensive financial services provider in India, focusing on diverse banking solutions ranging from retail to corporate banking. The bank's market capitalization stands at approximately ₹125.45 billion.

Operations: The bank operates with a consistent gross profit margin of 100%, reflecting its ability to generate revenue without the cost of goods sold. Its net income margin has shown significant variation, ranging from -7.79% in 2017 to a high of approximately 29.51% by the end of 2023, indicating fluctuating profitability over the years.

Jammu and Kashmir Bank, often overlooked, showcases robust potential with a 50% earnings growth surpassing the industry's 30%. With assets totaling ₹1,545B and a strong deposit base of ₹1,348B reflecting stable funding primarily from customer deposits—a less risky source—its financial foundation is solid. However, it grapples with high non-performing loans at 4.2%, signaling areas needing attention. The bank's P/E ratio stands attractively at 7.1x against the broader Indian market average of 34x.

- Click here and access our complete health analysis report to understand the dynamics of Jammu and Kashmir Bank.

Explore historical data to track Jammu and Kashmir Bank's performance over time in our Past section.

Jammu and Kashmir Bank (NSEI:J&KBANK)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Jammu and Kashmir Bank Limited operates as a comprehensive financial services provider in India, focusing on diverse banking solutions ranging from retail to corporate banking. The bank's market capitalization stands at approximately ₹125.45 billion.

Operations: The bank operates with a consistent gross profit margin of 100%, reflecting its ability to generate revenue without the cost of goods sold. Its net income margin has shown significant variation, ranging from -7.79% in 2017 to a high of approximately 29.51% by the end of 2023, indicating fluctuating profitability over the years.

Jammu and Kashmir Bank, often overlooked, showcases robust potential with a 50% earnings growth surpassing the industry's 30%. With assets totaling ₹1,545B and a strong deposit base of ₹1,348B reflecting stable funding primarily from customer deposits—a less risky source—its financial foundation is solid. However, it grapples with high non-performing loans at 4.2%, signaling areas needing attention. The bank's P/E ratio stands attractively at 7.1x against the broader Indian market average of 34x.

- Click here and access our complete health analysis report to understand the dynamics of Jammu and Kashmir Bank.

Explore historical data to track Jammu and Kashmir Bank's performance over time in our Past section.

Network People Services Technologies (NSEI:NPST)

Simply Wall St Value Rating: ★★★★★☆

Overview: Network People Services Technologies Limited specializes in creating digital payment solutions for banks, financial institutions, and merchants within the fintech sector in India, with a market capitalization of ₹41.00 billion.

Operations: The company generates its revenue primarily from software and programming services, with a notable gross profit margin of 38.78% as of the latest reporting period. Its operational model has scaled significantly, reflected by an increase in revenue to ₹1275.52 million, coupled with a substantial rise in net income to ₹267.21 million during the same timeframe.

Network People Services Technologies, a burgeoning player in India's financial sector, has demonstrated robust growth with a 310% increase in earnings over the past year, surpassing the industry's 21% average. The company boasts high-quality earnings and an EBIT coverage of its interest payments by a staggering 1295 times. With more cash than debt on its books and recent executive appointments bolstering its leadership team, NPST is poised for further growth amidst market volatility.

Network People Services Technologies (NSEI:NPST)

Simply Wall St Value Rating: ★★★★★☆

Overview: Network People Services Technologies Limited specializes in creating digital payment solutions for banks, financial institutions, and merchants within the fintech sector in India, with a market capitalization of ₹41.00 billion.

Operations: The company generates its revenue primarily from software and programming services, with a notable gross profit margin of 38.78% as of the latest reporting period. Its operational model has scaled significantly, reflected by an increase in revenue to ₹1275.52 million, coupled with a substantial rise in net income to ₹267.21 million during the same timeframe.

Network People Services Technologies, a burgeoning player in India's financial sector, has demonstrated robust growth with a 310% increase in earnings over the past year, surpassing the industry's 21% average. The company boasts high-quality earnings and an EBIT coverage of its interest payments by a staggering 1295 times. With more cash than debt on its books and recent executive appointments bolstering its leadership team, NPST is poised for further growth amidst market volatility.

Prudent Advisory Services (NSEI:PRUDENT)

Simply Wall St Value Rating: ★★★★★★

Overview: Prudent Corporate Advisory Services Limited offers advisory and distribution services for various mutual funds targeting individuals, corporates, high net worth individuals (HNIs), and ultra HNIs both in India and globally, with a market capitalization of ₹87.99 billion.

Operations: Through its core activity, the distribution and sale of financial products, the company generated ₹8.23 billion in revenue as of the latest reporting period. It has observed a gross profit margin of approximately 47.07%, reflecting its cost management in relation to generated sales.

Prudent Advisory Services, a notable player in the Indian financial sector, has demonstrated robust financial health and growth potential. With no debt and high-quality earnings, the company has maintained an impressive annual earnings growth of 28.8% over the past five years. Recently, it forecasted a further 22.77% yearly increase in earnings. The firm also declared a dividend of INR 2 per share after reporting substantial revenue growth to INR 8,247 million this year from INR 6,189 million last year, reflecting strong operational performance and investor confidence.

- Take a closer look at Prudent Advisory Services' potential here in our health report.

Gain insights into Prudent Advisory Services' past trends and performance with our Past report.

Prudent Advisory Services (NSEI:PRUDENT)

Simply Wall St Value Rating: ★★★★★★

Overview: Prudent Corporate Advisory Services Limited offers advisory and distribution services for various mutual funds targeting individuals, corporates, high net worth individuals (HNIs), and ultra HNIs both in India and globally, with a market capitalization of ₹87.99 billion.

Operations: Through its core activity, the distribution and sale of financial products, the company generated ₹8.23 billion in revenue as of the latest reporting period. It has observed a gross profit margin of approximately 47.07%, reflecting its cost management in relation to generated sales.

Prudent Advisory Services, a notable player in the Indian financial sector, has demonstrated robust financial health and growth potential. With no debt and high-quality earnings, the company has maintained an impressive annual earnings growth of 28.8% over the past five years. Recently, it forecasted a further 22.77% yearly increase in earnings. The firm also declared a dividend of INR 2 per share after reporting substantial revenue growth to INR 8,247 million this year from INR 6,189 million last year, reflecting strong operational performance and investor confidence.

- Take a closer look at Prudent Advisory Services' potential here in our health report.

Gain insights into Prudent Advisory Services' past trends and performance with our Past report.

Key Takeaways

- Unlock our comprehensive list of 459 Indian Undiscovered Gems With Strong Fundamentals by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:J&KBANK

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives