Advertisement

Is Indian Card Clothing (NSE:INDIANCARD) Weighed On By Its Debt Load?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that The Indian Card Clothing Company Limited (NSE:INDIANCARD) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Indian Card Clothing

How Much Debt Does Indian Card Clothing Carry?

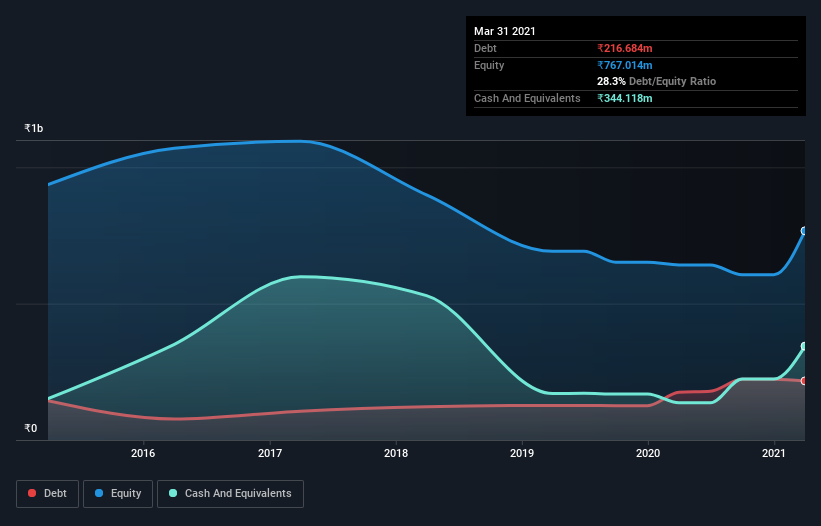

As you can see below, at the end of March 2021, Indian Card Clothing had ₹213.0m of debt, up from ₹175.2m a year ago. Click the image for more detail. But on the other hand it also has ₹344.1m in cash, leading to a ₹131.1m net cash position.

A Look At Indian Card Clothing's Liabilities

The latest balance sheet data shows that Indian Card Clothing had liabilities of ₹160.6m due within a year, and liabilities of ₹216.7m falling due after that. Offsetting this, it had ₹344.1m in cash and ₹116.4m in receivables that were due within 12 months. So it actually has ₹83.2m more liquid assets than total liabilities.

This short term liquidity is a sign that Indian Card Clothing could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Indian Card Clothing has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Indian Card Clothing will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Indian Card Clothing had a loss before interest and tax, and actually shrunk its revenue by 11%, to ₹546m. That's not what we would hope to see.

So How Risky Is Indian Card Clothing?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Indian Card Clothing lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through ₹138m of cash and made a loss of ₹23m. Given it only has net cash of ₹131.1m, the company may need to raise more capital if it doesn't reach break-even soon. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Indian Card Clothing is showing 3 warning signs in our investment analysis , and 1 of those makes us a bit uncomfortable...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

When trading Indian Card Clothing or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:INDIANCARD

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor