- India

- /

- Electrical

- /

- NSEI:ZODIAC

Zodiac Energy Limited (NSE:ZODIAC) Shares Slammed 28% But Getting In Cheap Might Be Difficult Regardless

Zodiac Energy Limited (NSE:ZODIAC) shareholders that were waiting for something to happen have been dealt a blow with a 28% share price drop in the last month. Looking at the bigger picture, even after this poor month the stock is up 31% in the last year.

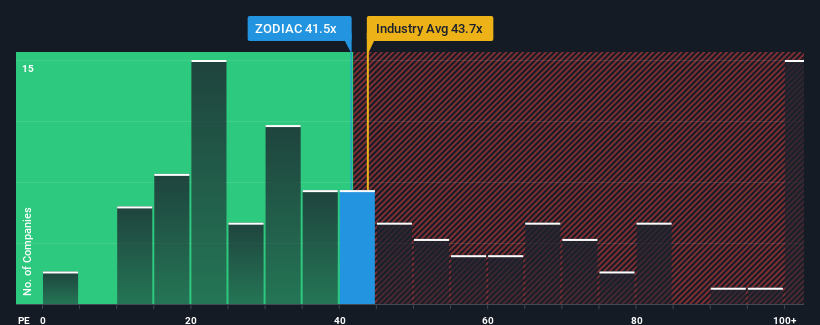

In spite of the heavy fall in price, given around half the companies in India have price-to-earnings ratios (or "P/E's") below 30x, you may still consider Zodiac Energy as a stock to potentially avoid with its 41.5x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's exceedingly strong of late, Zodiac Energy has been doing very well. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Zodiac Energy

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Zodiac Energy's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 168%. The latest three year period has also seen an excellent 131% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 26% shows it's noticeably more attractive on an annualised basis.

In light of this, it's understandable that Zodiac Energy's P/E sits above the majority of other companies. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the bourse.

The Final Word

Despite the recent share price weakness, Zodiac Energy's P/E remains higher than most other companies. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Zodiac Energy revealed its three-year earnings trends are contributing to its high P/E, given they look better than current market expectations. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Zodiac Energy (2 are a bit concerning!) that you should be aware of before investing here.

You might be able to find a better investment than Zodiac Energy. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Zodiac Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ZODIAC

Zodiac Energy

Engages in the installation of solar power generation plants and related items primarily in India.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives