Advertisement

- India

- /

- Construction

- /

- NSEI:SWSOLAR

Market Participants Recognise Sterling and Wilson Renewable Energy Limited's (NSE:SWSOLAR) Revenues Pushing Shares 40% Higher

Sterling and Wilson Renewable Energy Limited (NSE:SWSOLAR) shares have had a really impressive month, gaining 40% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 70%.

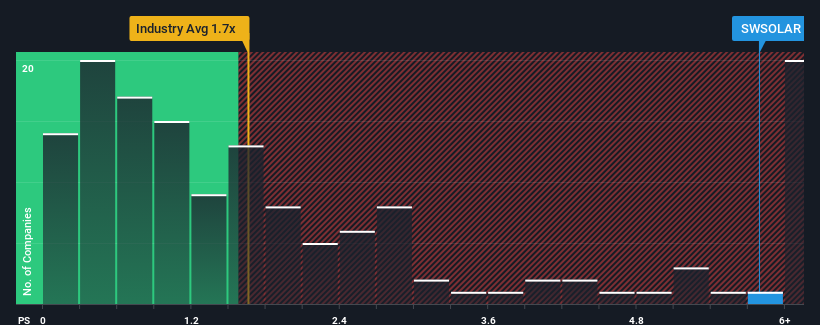

Since its price has surged higher, you could be forgiven for thinking Sterling and Wilson Renewable Energy is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 5.8x, considering almost half the companies in India's Construction industry have P/S ratios below 1.7x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for Sterling and Wilson Renewable Energy

What Does Sterling and Wilson Renewable Energy's P/S Mean For Shareholders?

While the industry has experienced revenue growth lately, Sterling and Wilson Renewable Energy's revenue has gone into reverse gear, which is not great. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Sterling and Wilson Renewable Energy's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Sterling and Wilson Renewable Energy's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 57%. The last three years don't look nice either as the company has shrunk revenue by 68% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 534% during the coming year according to the sole analyst following the company. Meanwhile, the rest of the industry is forecast to only expand by 11%, which is noticeably less attractive.

In light of this, it's understandable that Sterling and Wilson Renewable Energy's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

The strong share price surge has lead to Sterling and Wilson Renewable Energy's P/S soaring as well. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Sterling and Wilson Renewable Energy maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Construction industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Sterling and Wilson Renewable Energy (1 is significant!) that you need to be mindful of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SWSOLAR

Sterling and Wilson Renewable Energy

Engages in the provision of engineering, procurement, and construction (EPC) services to solar power projects.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor