Advertisement

Orient Bell (NSE:ORIENTBELL) Is Reducing Its Dividend To ₹0.50

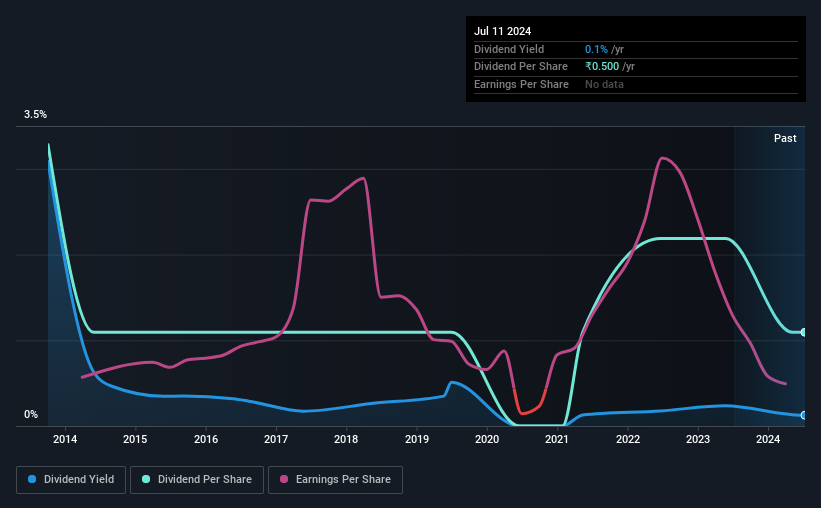

Orient Bell Limited's (NSE:ORIENTBELL) dividend is being reduced from last year's payment covering the same period to ₹0.50 on the 5th of September. This payment takes the dividend yield to 0.1%, which only provides a modest boost to overall returns.

View our latest analysis for Orient Bell

Orient Bell Is Paying Out More Than It Is Earning

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Prior to this announcement, Orient Bell's dividend was making up a very large proportion of earnings, and the company was also not generating any cash flow to offset this. Generally, we think that this would be a risky long term practice.

If the company can't turn things around, EPS could fall by 37.2% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could reach 133%, which could put the dividend in jeopardy if the company's earnings don't improve.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2014, the dividend has gone from ₹1.50 total annually to ₹0.50. The dividend has fallen 67% over that period. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

The Dividend Has Limited Growth Potential

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. Orient Bell's earnings per share has shrunk at 37% a year over the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future.

Orient Bell's Dividend Doesn't Look Sustainable

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. The payments are bit high to be considered sustainable, and the track record isn't the best. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 2 warning signs for Orient Bell that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:ORIENTBELL

Orient Bell

Manufactures, trades in, and sells ceramic and floor tiles in India and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|17.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|11.0% undervalued

CH

Community Contributor