- India

- /

- Construction

- /

- NSEI:NBCC

Read This Before Considering NBCC (India) Limited (NSE:NBCC) For Its Upcoming ₹0.53 Dividend

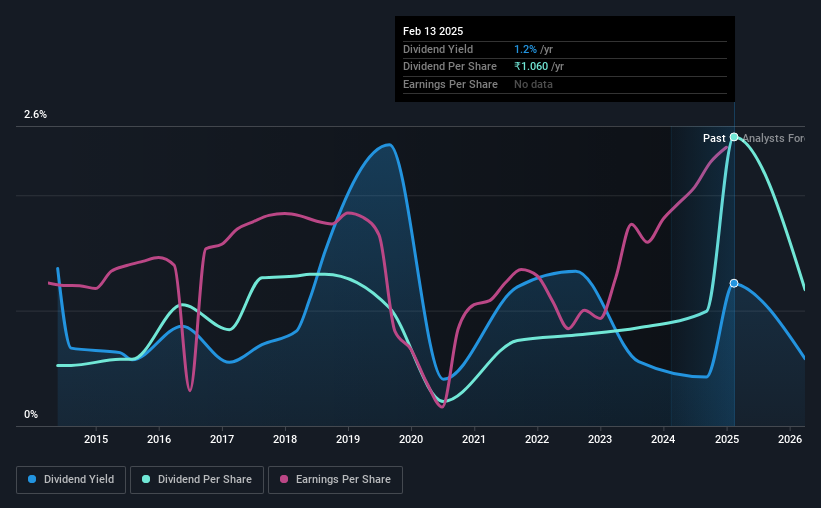

NBCC (India) Limited (NSE:NBCC) is about to trade ex-dividend in the next 3 days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade takes at least two business day to settle. Thus, you can purchase NBCC (India)'s shares before the 18th of February in order to receive the dividend, which the company will pay on the 13th of March.

The company's next dividend payment will be ₹0.53 per share. Last year, in total, the company distributed ₹1.06 to shareholders. Based on the last year's worth of payments, NBCC (India) stock has a trailing yield of around 1.2% on the current share price of ₹85.75. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether NBCC (India) can afford its dividend, and if the dividend could grow.

See our latest analysis for NBCC (India)

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. NBCC (India) paid out a comfortable 28% of its profit last year. A useful secondary check can be to evaluate whether NBCC (India) generated enough free cash flow to afford its dividend. It paid out more than half (69%) of its free cash flow in the past year, which is within an average range for most companies.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. With that in mind, we're encouraged by the steady growth at NBCC (India), with earnings per share up 6.0% on average over the last five years. While earnings have been growing at a credible rate, the company is paying out a majority of its earnings to shareholders. If management lifts the payout ratio further, we'd take this as a tacit signal that the company's growth prospects are slowing.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Since the start of our data, 10 years ago, NBCC (India) has lifted its dividend by approximately 17% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

The Bottom Line

Should investors buy NBCC (India) for the upcoming dividend? Earnings per share have been growing at a steady rate, and NBCC (India) paid out less than half its profits and more than half its free cash flow as dividends over the last year. Overall, it's hard to get excited about NBCC (India) from a dividend perspective.

So while NBCC (India) looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. Case in point: We've spotted 1 warning sign for NBCC (India) you should be aware of.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NBCC (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NBCC

NBCC (India)

Engages in project management consultancy, engineering procurement and construction, and real estate development businesses in India and internationally.

Flawless balance sheet with solid track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)