- India

- /

- Construction

- /

- NSEI:CEMPRO

Be Sure To Check Out ITD Cementation India Limited (NSE:ITDCEM) Before It Goes Ex-Dividend

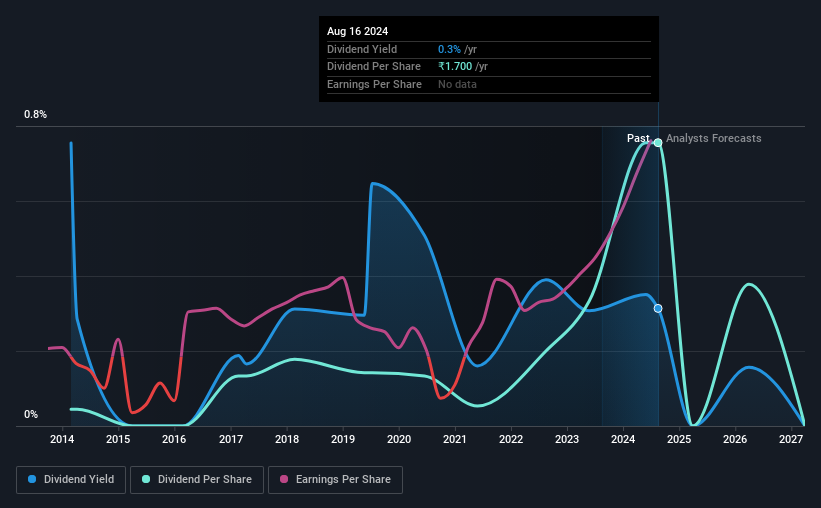

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that ITD Cementation India Limited (NSE:ITDCEM) is about to go ex-dividend in just three days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade takes at least two business day to settle. Accordingly, ITD Cementation India investors that purchase the stock on or after the 21st of August will not receive the dividend, which will be paid on the 10th of September.

The company's upcoming dividend is ₹1.70 a share, following on from the last 12 months, when the company distributed a total of ₹1.70 per share to shareholders. Calculating the last year's worth of payments shows that ITD Cementation India has a trailing yield of 0.3% on the current share price of ₹542.70. If you buy this business for its dividend, you should have an idea of whether ITD Cementation India's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

View our latest analysis for ITD Cementation India

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. ITD Cementation India paid out just 11% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. The good news is it paid out just 3.7% of its free cash flow in the last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. It's encouraging to see ITD Cementation India has grown its earnings rapidly, up 42% a year for the past five years. ITD Cementation India looks like a real growth company, with earnings per share growing at a cracking pace and the company reinvesting most of its profits in the business.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the last 10 years, ITD Cementation India has lifted its dividend by approximately 33% a year on average. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

The Bottom Line

Is ITD Cementation India worth buying for its dividend? ITD Cementation India has grown its earnings per share while simultaneously reinvesting in the business. Unfortunately it's cut the dividend at least once in the past 10 years, but the conservative payout ratio makes the current dividend look sustainable. It's a promising combination that should mark this company worthy of closer attention.

While it's tempting to invest in ITD Cementation India for the dividends alone, you should always be mindful of the risks involved. For example, we've found 2 warning signs for ITD Cementation India that we recommend you consider before investing in the business.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CEMPRO

Cemindia Projects

Provides construction and civil engineering contracting services in India.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion

Thanks for sharing these. They really help when I pick what dividend stocks to invest in