Ingersoll-Rand (India) Limited's (NSE:INGERRAND) Stock Has Shown Weakness Lately But Financial Prospects Look Decent: Is The Market Wrong?

With its stock down 12% over the past three months, it is easy to disregard Ingersoll-Rand (India) (NSE:INGERRAND). However, stock prices are usually driven by a company’s financials over the long term, which in this case look pretty respectable. Specifically, we decided to study Ingersoll-Rand (India)'s ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Ingersoll-Rand (India)

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Ingersoll-Rand (India) is:

40% = ₹2.3b ÷ ₹5.8b (Based on the trailing twelve months to June 2024).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each ₹1 of shareholders' capital it has, the company made ₹0.40 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Ingersoll-Rand (India)'s Earnings Growth And 40% ROE

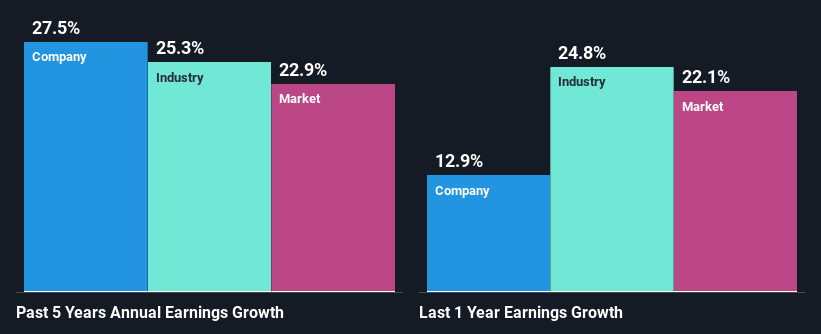

To begin with, Ingersoll-Rand (India) has a pretty high ROE which is interesting. Second, a comparison with the average ROE reported by the industry of 15% also doesn't go unnoticed by us. So, the substantial 28% net income growth seen by Ingersoll-Rand (India) over the past five years isn't overly surprising.

We then performed a comparison between Ingersoll-Rand (India)'s net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 25% in the same 5-year period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is Ingersoll-Rand (India) fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Ingersoll-Rand (India) Making Efficient Use Of Its Profits?

Ingersoll-Rand (India) has a significant three-year median payout ratio of 98%, meaning the company only retains 2.1% of its income. This implies that the company has been able to achieve high earnings growth despite returning most of its profits to shareholders.

Besides, Ingersoll-Rand (India) has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Conclusion

On the whole, we do feel that Ingersoll-Rand (India) has some positive attributes. Especially the growth in earnings which was backed by an impressive ROE. Still, the high ROE could have been even more beneficial to investors had the company been reinvesting more of its profits. As highlighted earlier, the current reinvestment rate appears to be negligible. Up till now, we've only made a short study of the company's growth data. To gain further insights into Ingersoll-Rand (India)'s past profit growth, check out this visualization of past earnings, revenue and cash flows.

If you're looking to trade Ingersoll-Rand (India), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INGERRAND

Ingersoll-Rand (India)

Manufactures and sells industrial air compressors in India.

Flawless balance sheet with proven track record and pays a dividend.

Market Insights

Community Narratives