- India

- /

- Auto Components

- /

- NSEI:UNOMINDA

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For Uno Minda Limited's (NSE:UNOMINDA) CEO For Now

Key Insights

- Uno Minda's Annual General Meeting to take place on 20th of September

- Salary of ₹42.1m is part of CEO Nirmal Minda's total remuneration

- The overall pay is 74% above the industry average

- Over the past three years, Uno Minda's EPS grew by 64% and over the past three years, the total shareholder return was 238%

Performance at Uno Minda Limited (NSE:UNOMINDA) has been reasonably good and CEO Nirmal Minda has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 20th of September. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for Uno Minda

Comparing Uno Minda Limited's CEO Compensation With The Industry

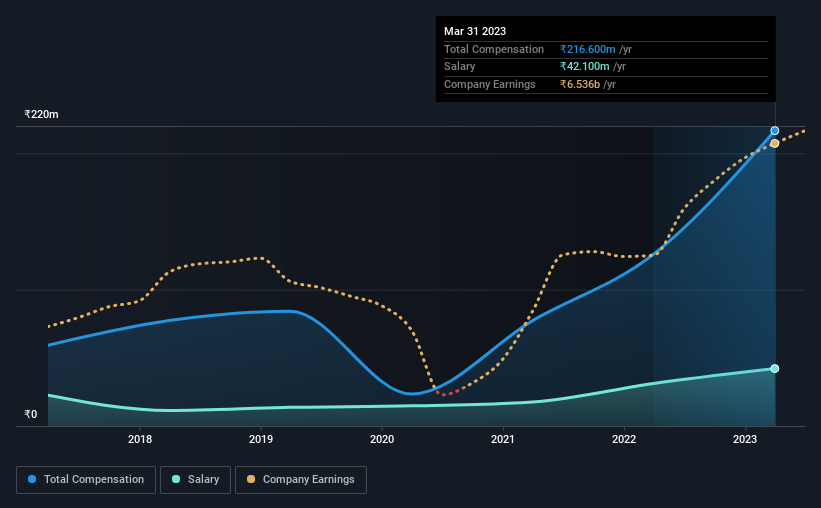

At the time of writing, our data shows that Uno Minda Limited has a market capitalization of ₹355b, and reported total annual CEO compensation of ₹217m for the year to March 2023. That's a notable increase of 72% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at ₹42m.

In comparison with other companies in the Indian Auto Components industry with market capitalizations ranging from ₹166b to ₹531b, the reported median CEO total compensation was ₹125m. Hence, we can conclude that Nirmal Minda is remunerated higher than the industry median. Furthermore, Nirmal Minda directly owns ₹129b worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | ₹42m | ₹31m | 19% |

| Other | ₹175m | ₹95m | 81% |

| Total Compensation | ₹217m | ₹126m | 100% |

Talking in terms of the industry, salary represented approximately 76% of total compensation out of all the companies we analyzed, while other remuneration made up 24% of the pie. Uno Minda sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Uno Minda Limited's Growth

Uno Minda Limited's earnings per share (EPS) grew 64% per year over the last three years. Its revenue is up 27% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Uno Minda Limited Been A Good Investment?

Most shareholders would probably be pleased with Uno Minda Limited for providing a total return of 238% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 1 warning sign for Uno Minda that investors should look into moving forward.

Important note: Uno Minda is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:UNOMINDA

Uno Minda

Manufactures and supplies auto components and systems in India and internationally.

Flawless balance sheet with high growth potential.