- Turkey

- /

- Transportation

- /

- IBSE:LIDER

Exploring Three Undiscovered Gems in the Middle East Market

Reviewed by Simply Wall St

In recent weeks, Middle Eastern markets have experienced fluctuations, with most Gulf equities ending lower as investors await signals from the U.S. Federal Reserve's upcoming Jackson Hole speech. Amidst this backdrop of uncertainty and profit-taking in key indices like Qatar's and Dubai's, discerning investors are on the lookout for stocks that demonstrate resilience and potential growth despite broader market challenges.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 10.97% | 10.37% | 3.14% | ★★★★★★ |

| MOBI Industry | 6.50% | 5.60% | 24.00% | ★★★★★★ |

| Baazeem Trading | 8.48% | -1.74% | -2.37% | ★★★★★★ |

| Sure Global Tech | NA | 11.95% | 18.65% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 1.94% | 16.33% | 21.26% | ★★★★★★ |

| Najran Cement | 14.76% | -3.67% | -26.79% | ★★★★★★ |

| Nofoth Food Products | NA | 15.75% | 27.63% | ★★★★★★ |

| Etihad Atheeb Telecommunication | 0.97% | 37.69% | 60.25% | ★★★★★☆ |

| Gür-Sel Turizm Tasimacilik ve Servis Ticaret | 6.88% | 51.77% | 67.59% | ★★★★★☆ |

| National Environmental Recycling | 69.43% | 43.47% | 32.77% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

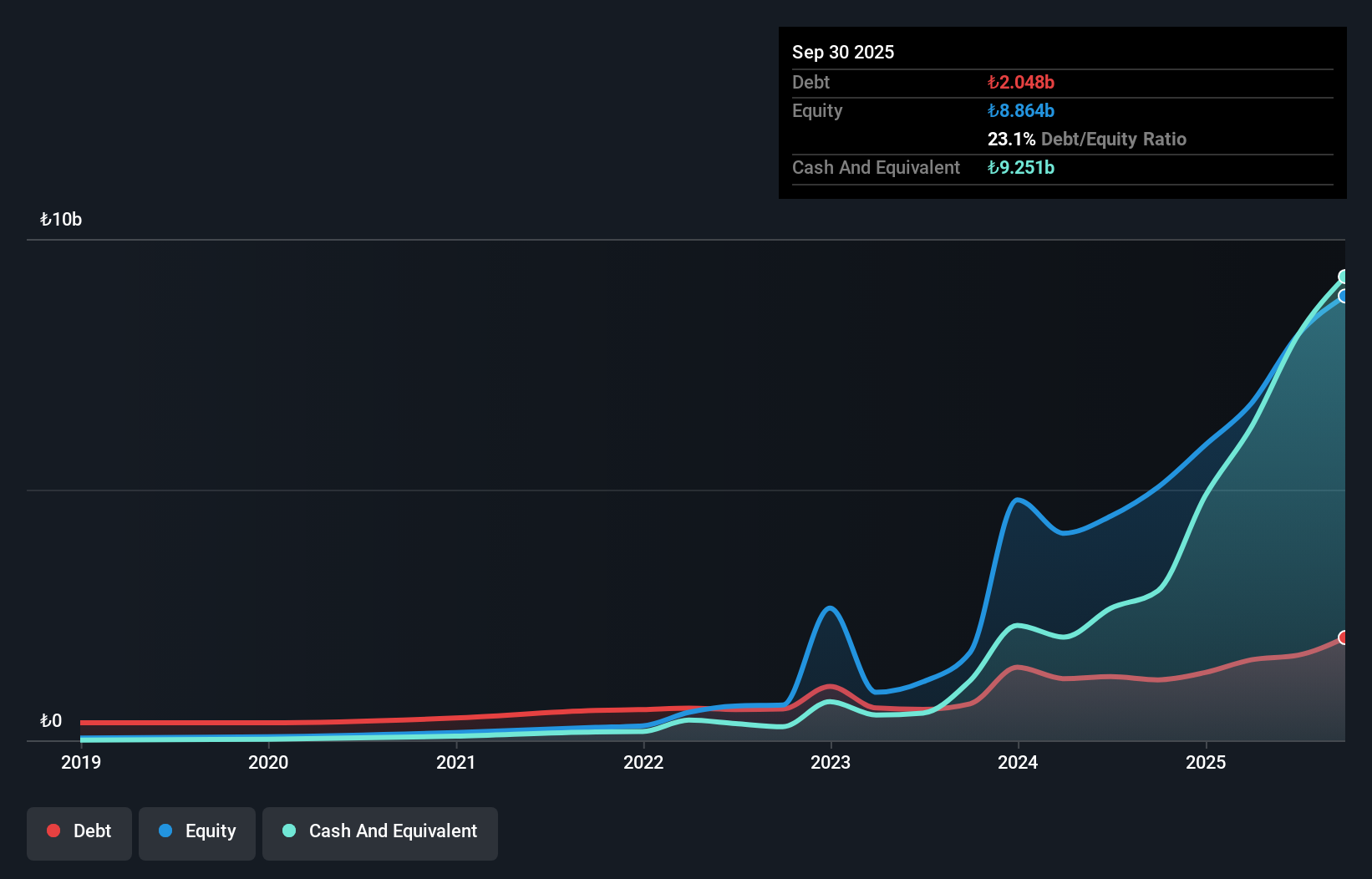

LDR Turizm (IBSE:LIDER)

Simply Wall St Value Rating: ★★★★☆☆

Overview: LDR Turizm A.S. specializes in long-term car rental services and has a market cap of TRY45.84 billion.

Operations: LDR Turizm generates revenue primarily from long-term car rental services. The company has a market cap of TRY45.84 billion, indicating its significant presence in the industry.

LDR Turizm, a dynamic player in the Middle East, showcases intriguing financial shifts. Over five years, its debt to equity ratio impressively dropped from 354.9% to 21%, hinting at strategic financial management. Despite sales dipping to TRY 442 million in Q2 2025 from TRY 620 million the previous year, net income surged dramatically to TRY 1 billion from TRY 21 million. This earnings growth outpaces the transportation sector significantly, with a notable increase of over 186%. The company’s price-to-earnings ratio of 25x remains attractive compared to the industry average of nearly double that figure.

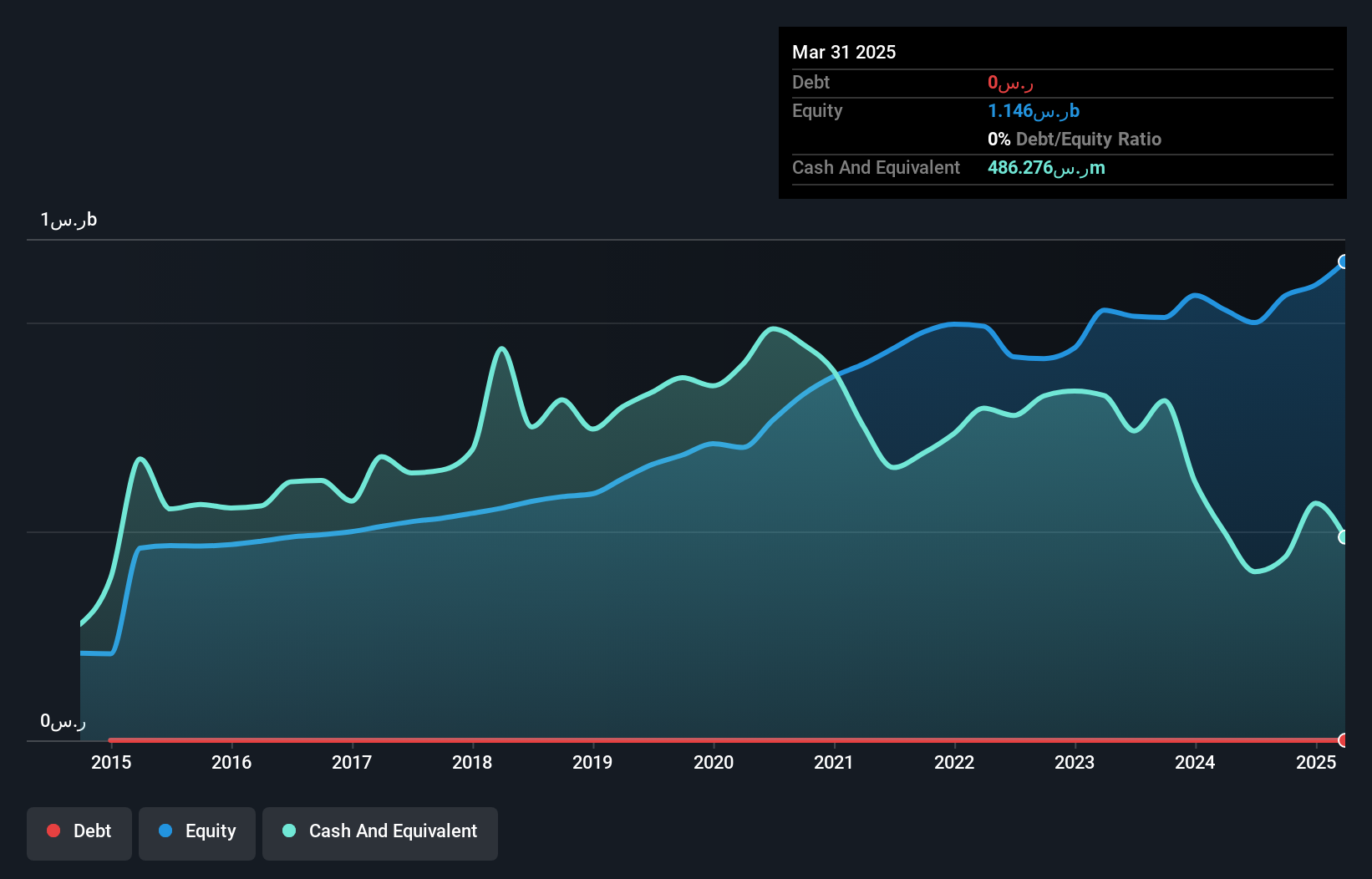

Gulf Insurance Group (SASE:8250)

Simply Wall St Value Rating: ★★★★★☆

Overview: Gulf Insurance Group offers a range of insurance and reinsurance products and services to corporates, SMEs, and individual customers in Saudi Arabia, with a market capitalization of SAR1.31 billion.

Operations: The company's primary revenue streams include Motor insurance (SAR622.52 million), Health insurance (SAR396.47 million), and Property and Casualty insurance (SAR355.84 million).

Gulf Insurance Group, a small-cap player in the insurance sector, has demonstrated robust financial health with no debt over the past five years and high-quality earnings. The company’s price-to-earnings ratio of 10.3x suggests it is trading at a good value compared to the SA market's 20.9x. Despite net income for Q2 2025 dropping to SAR 34.14 million from SAR 52.46 million last year, six-month figures show an increase to SAR 61.23 million from SAR 32.24 million previously, indicating potential resilience amidst industry challenges where earnings growth outpaced peers significantly by growing at 97.5% against an industry decline of -23%.

- Unlock comprehensive insights into our analysis of Gulf Insurance Group stock in this health report.

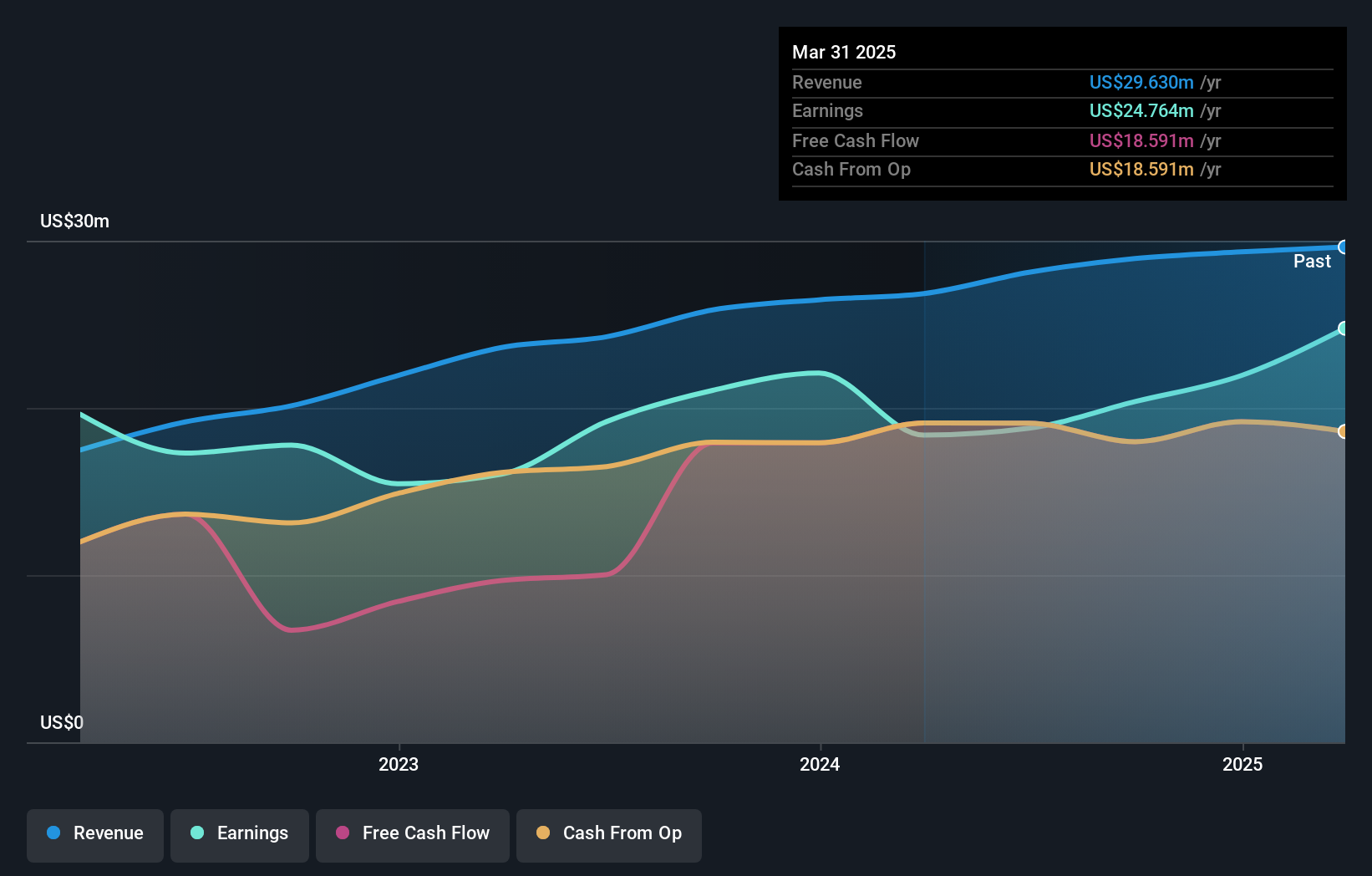

Cohen Development Gas & Oil (TASE:CDEV)

Simply Wall St Value Rating: ★★★★★★

Overview: Cohen Development Gas & Oil Ltd. is involved in the exploration, development, production, and marketing of natural gas, condensate, and oil across Israel, Cyprus, and Morocco with a market capitalization of ₪1.30 billion.

Operations: Cohen Development Gas & Oil generates revenue primarily from the production and management of oil and gas exploration, amounting to $29.63 million.

Cohen Development Gas & Oil, a nimble player in the Middle East energy sector, has been making waves with its robust financial health. The company is debt-free and boasts a price-to-earnings ratio of 15.4x, slightly below the IL market's 15.7x, indicating potential undervaluation. Over the past year, earnings surged by 34.8%, outpacing the broader oil and gas industry's negative growth of -1%. Recent earnings announcements revealed net income at US$6.26 million for Q1 2025, up from US$3.44 million last year, with basic EPS climbing to US$0.97 from US$0.53—reflecting strong operational performance and profitability prospects ahead.

Summing It All Up

- Delve into our full catalog of 213 Middle Eastern Undiscovered Gems With Strong Fundamentals here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:LIDER

Solid track record with excellent balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion

Thanks for sharing these. They really help when I pick what dividend stocks to invest in