- Israel

- /

- Aerospace & Defense

- /

- TASE:RSEL

Don't Buy RSL Electronics Ltd. (TLV:RSEL) For Its Next Dividend Without Doing These Checks

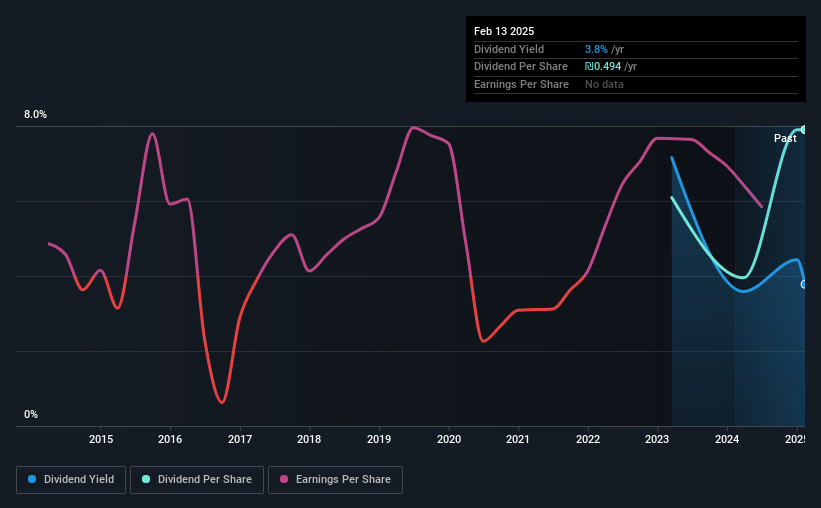

Readers hoping to buy RSL Electronics Ltd. (TLV:RSEL) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade takes at least two business day to settle. This means that investors who purchase RSL Electronics' shares on or after the 18th of February will not receive the dividend, which will be paid on the 27th of February.

The company's next dividend payment will be ₪0.4939405 per share. Last year, in total, the company distributed ₪0.25 to shareholders. Based on the last year's worth of payments, RSL Electronics has a trailing yield of 3.8% on the current stock price of ₪13.07. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

Check out our latest analysis for RSL Electronics

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. RSL Electronics is paying out an acceptable 67% of its profit, a common payout level among most companies. A useful secondary check can be to evaluate whether RSL Electronics generated enough free cash flow to afford its dividend.

Click here to see how much of its profit RSL Electronics paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. This is why it's a relief to see RSL Electronics earnings per share are up 2.4% per annum over the last five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. RSL Electronics has delivered an average of 14% per year annual increase in its dividend, based on the past two years of dividend payments. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

To Sum It Up

Should investors buy RSL Electronics for the upcoming dividend? RSL Electronics is paying out a reasonable percentage of its income and an uncomfortably high -83% of its cash flow as dividends. At least earnings per share have been growing steadily. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with RSL Electronics. For example, we've found 5 warning signs for RSL Electronics (1 is a bit concerning!) that deserve your attention before investing in the shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:RSEL

RSL Electronics

Develops, manufactures, and sells control systems, utilities, health monitoring, and diagnostics and prognostics systems for aerospace, railroad, energy, and defense sectors in Israel and internationally.

Outstanding track record with flawless balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)