Advertisement

Birman Wood & Hardware (TLV:BIRM) Could Be At Risk Of Shrinking As A Company

When we're researching a company, it's sometimes hard to find the warning signs, but there are some financial metrics that can help spot trouble early. A business that's potentially in decline often shows two trends, a return on capital employed (ROCE) that's declining, and a base of capital employed that's also declining. Trends like this ultimately mean the business is reducing its investments and also earning less on what it has invested. So after glancing at the trends within Birman Wood & Hardware (TLV:BIRM), we weren't too hopeful.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Birman Wood & Hardware, this is the formula:

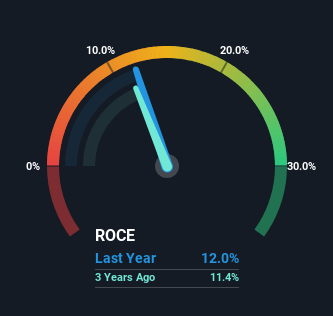

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.12 = ₪18m ÷ (₪451m - ₪298m) (Based on the trailing twelve months to June 2023).

Therefore, Birman Wood & Hardware has an ROCE of 12%. That's a relatively normal return on capital, and it's around the 11% generated by the Building industry.

Check out our latest analysis for Birman Wood & Hardware

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Birman Wood & Hardware has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What Can We Tell From Birman Wood & Hardware's ROCE Trend?

There is reason to be cautious about Birman Wood & Hardware, given the returns are trending downwards. Unfortunately the returns on capital have diminished from the 20% that they were earning five years ago. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Birman Wood & Hardware to turn into a multi-bagger.

On a side note, Birman Wood & Hardware's current liabilities are still rather high at 66% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

Our Take On Birman Wood & Hardware's ROCE

In summary, it's unfortunate that Birman Wood & Hardware is generating lower returns from the same amount of capital. Despite the concerning underlying trends, the stock has actually gained 6.1% over the last five years, so it might be that the investors are expecting the trends to reverse. Regardless, we don't like the trends as they are and if they persist, we think you might find better investments elsewhere.

If you'd like to know more about Birman Wood & Hardware, we've spotted 5 warning signs, and 3 of them don't sit too well with us.

While Birman Wood & Hardware may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Birman Wood & Hardware might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:BIRM

Birman Wood & Hardware

Imports, produces, and markets wood panels, hardware products, kitchen electrical appliances, and laminate flooring parquets.

Moderate second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor