- Hong Kong

- /

- Renewable Energy

- /

- SEHK:836

With A -13% Earnings Drop, Did China Resources Power Holdings Company Limited (HKG:836) Really Underperform?

Examining China Resources Power Holdings Company Limited's (SEHK:836) past track record of performance is a valuable exercise for investors. It enables us to understand whether the company has met or exceed expectations, which is a powerful signal for future performance. Below, I will assess 836's latest performance announced on 30 June 2019 and weigh these figures against its longer term trend and industry movements.

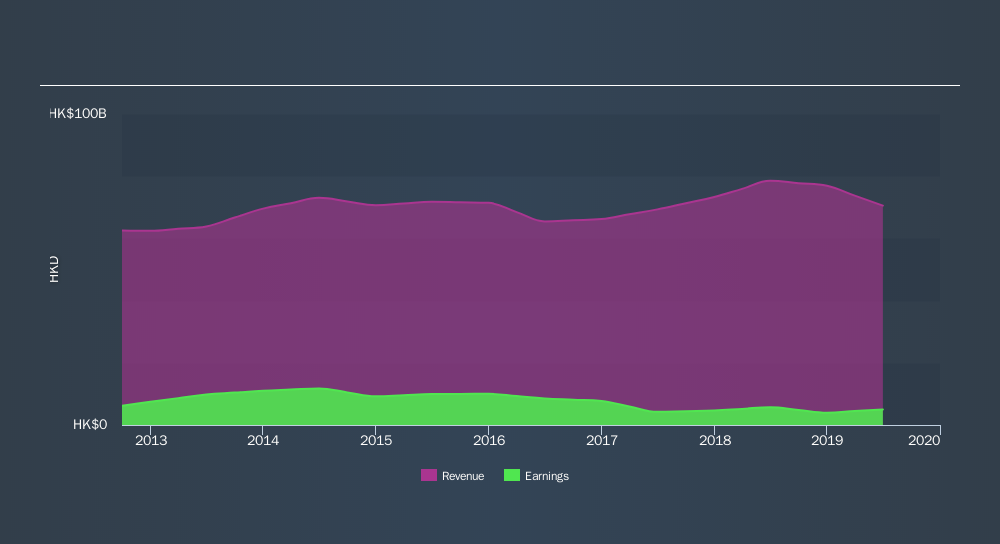

Check out our latest analysis for China Resources Power Holdings

Despite a decline, did 836 underperform the long-term trend and the industry?

836's trailing twelve-month earnings (from 30 June 2019) of HK$5.0b has declined by -13% compared to the previous year.

Furthermore, this one-year growth rate has been lower than its average earnings growth rate over the past 5 years of -21%, indicating the rate at which 836 is growing has slowed down. Why is this? Well, let’s take a look at what’s going on with margins and if the entire industry is experiencing the hit as well.

In terms of returns from investment, China Resources Power Holdings has fallen short of achieving a 20% return on equity (ROE), recording 7.4% instead. Furthermore, its return on assets (ROA) of 3.9% is below the HK Renewable Energy industry of 4.3%, indicating China Resources Power Holdings's are utilized less efficiently. And finally, its return on capital (ROC), which also accounts for China Resources Power Holdings’s debt level, has declined over the past 3 years from 14% to 8.4%. This correlates with an increase in debt holding, with debt-to-equity ratio rising from 114% to 124% over the past 5 years.

What does this mean?

While past data is useful, it doesn’t tell the whole story. Typically companies that experience a prolonged period of decline in earnings are going through some sort of reinvestment phase Although, if the entire industry is struggling to grow over time, it may be a signal of a structural change, which makes China Resources Power Holdings and its peers a higher risk investment. I recommend you continue to research China Resources Power Holdings to get a more holistic view of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for 836’s future growth? Take a look at our free research report of analyst consensus for 836’s outlook.

- Financial Health: Are 836’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 30 June 2019. This may not be consistent with full year annual report figures.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:836

China Resources Power Holdings

An investment holding company, invests in, develops, operates, and manages power plants and coal mines in the People’s Republic of China.

Good value second-rate dividend payer.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)