- Hong Kong

- /

- Gas Utilities

- /

- SEHK:3

Hong Kong and China Gas (SEHK:3) Valuation After Major AWS Cloud and AI Modernization Drive

Reviewed by Simply Wall St

Hong Kong and China Gas (SEHK:3) just pushed a big chunk of its core infrastructure onto Amazon Web Services with partner eCloudvalley, aiming for up to 40% lower IT costs and 99.99% uptime on mission critical systems.

See our latest analysis for Hong Kong and China Gas.

The HK$7.18 share price has held up reasonably well this year, with a 17.5% year to date share price return and a 24.8% one year total shareholder return suggesting improving sentiment as investors warm to its gradual earnings growth and digital overhaul.

If this kind of digital upgrade has you rethinking your watchlist, it could be worth exploring fast growing stocks with high insider ownership as a way to uncover other under the radar compounders.

Yet despite only a modest discount to analyst targets, the stock trades at a meaningful intrinsic discount, with steady earnings growth and digital efficiencies starting to build. Is this a quiet buying window, or is the market already pricing in the upside?

Price-to-Earnings of 23.8x: Is it justified?

On a price-to-earnings ratio of 23.8x, Hong Kong and China Gas looks expensive versus peers at the current HK$7.18 share price.

The price-to-earnings multiple compares what investors pay today with the company’s current earnings, and it is a standard yardstick for steady, cash generating utilities like gas distributors. A higher multiple implies the market is baking in stronger or more reliable profit streams than the sector norm.

Here, the market is assigning Hong Kong and China Gas a premium multiple of 23.8x, which sits well above both the Asian Gas Utilities industry average of 13.3x and the peer average of 13.9x, and is also more than double our estimated fair price-to-earnings ratio of 10.5x that the market could ultimately converge toward as expectations reset.

Explore the SWS fair ratio for Hong Kong and China Gas

Result: Price-to-Earnings of 23.8x (OVERVALUED)

However, persistent overvaluation and only modest revenue growth could quickly unwind sentiment if digital efficiencies or mainland expansion fail to materially boost earnings.

Find out about the key risks to this Hong Kong and China Gas narrative.

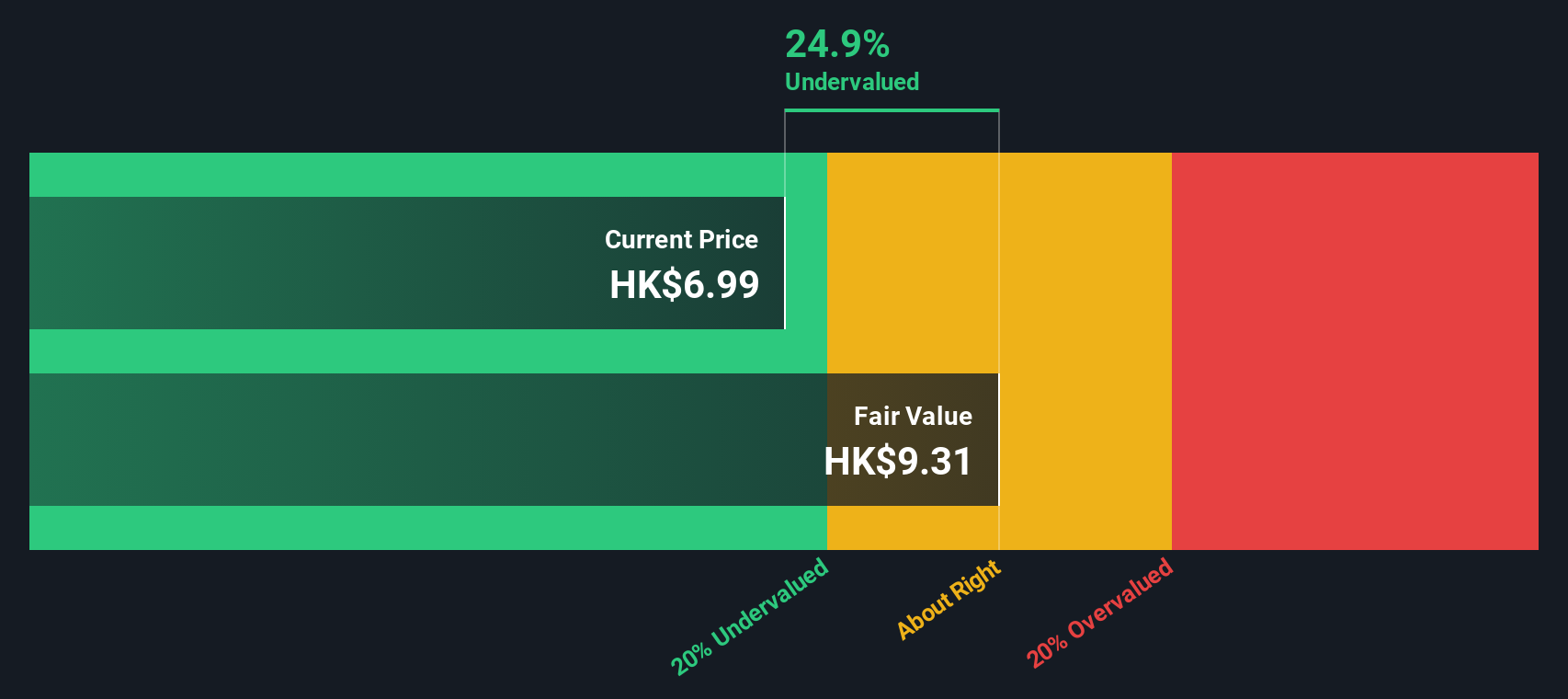

Another View: What Our DCF Says

While the 23.8x earnings multiple makes Hong Kong and China Gas look expensive, our DCF model tells a different story. It suggests fair value around HK$9.31 versus the current HK$7.18, roughly a 23% upside. Is the market underestimating steady, utility like cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hong Kong and China Gas for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hong Kong and China Gas Narrative

If you see things differently or want to stress test your own assumptions, you can build a personalised narrative in just a few minutes: Do it your way.

A great starting point for your Hong Kong and China Gas research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in an edge by hand picking your next opportunity with targeted screeners that surface quality, momentum, and mispriced growth stories fast.

- Capture resilient income streams by focusing on companies in these 13 dividend stocks with yields > 3% that offer attractive yields supported by cash rich balance sheets.

- Ride structural growth trends by zeroing in on innovators from these 26 AI penny stocks shaping productivity, automation, and data driven decision making.

- Seize potential bargains by targeting companies in these 908 undervalued stocks based on cash flows where share prices trail the strength of their underlying cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hong Kong and China Gas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:3

Hong Kong and China Gas

Produces, distributes, and markets gas, water supply and energy services in Hong Kong and Mainland China.

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)