Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:6888

Freetech Road Recycling Technology (Holdings) Limited's (HKG:6888) Share Price Boosted 37% But Its Business Prospects Need A Lift Too

Freetech Road Recycling Technology (Holdings) Limited (HKG:6888) shares have had a really impressive month, gaining 37% after a shaky period beforehand. Unfortunately, despite the strong performance over the last month, the full year gain of 4.3% isn't as attractive.

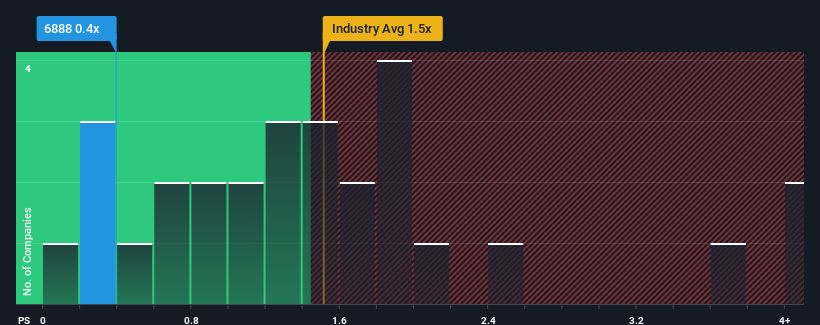

Although its price has surged higher, when close to half the companies operating in Hong Kong's Infrastructure industry have price-to-sales ratios (or "P/S") above 1.5x, you may still consider Freetech Road Recycling Technology (Holdings) as an enticing stock to check out with its 0.4x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Freetech Road Recycling Technology (Holdings)

How Has Freetech Road Recycling Technology (Holdings) Performed Recently?

The revenue growth achieved at Freetech Road Recycling Technology (Holdings) over the last year would be more than acceptable for most companies. Perhaps the market is expecting this acceptable revenue performance to take a dive, which has kept the P/S suppressed. Those who are bullish on Freetech Road Recycling Technology (Holdings) will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Freetech Road Recycling Technology (Holdings)'s earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Freetech Road Recycling Technology (Holdings)?

In order to justify its P/S ratio, Freetech Road Recycling Technology (Holdings) would need to produce sluggish growth that's trailing the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 16%. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 4.4% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Comparing that to the industry, which is predicted to deliver 3.1% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this in mind, we understand why Freetech Road Recycling Technology (Holdings)'s P/S is lower than most of its industry peers. However, we think shrinking revenues are unlikely to lead to a stable P/S over the longer term, which could set up shareholders for future disappointment. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Bottom Line On Freetech Road Recycling Technology (Holdings)'s P/S

Freetech Road Recycling Technology (Holdings)'s stock price has surged recently, but its but its P/S still remains modest. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Freetech Road Recycling Technology (Holdings) revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

Having said that, be aware Freetech Road Recycling Technology (Holdings) is showing 3 warning signs in our investment analysis, you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6888

Freetech Road Recycling Technology (Holdings)

An investment holding company, manufactures and sells road maintenance equipment in Mainland China.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor