Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies COSCO SHIPPING Ports Limited (HKG:1199) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for COSCO SHIPPING Ports

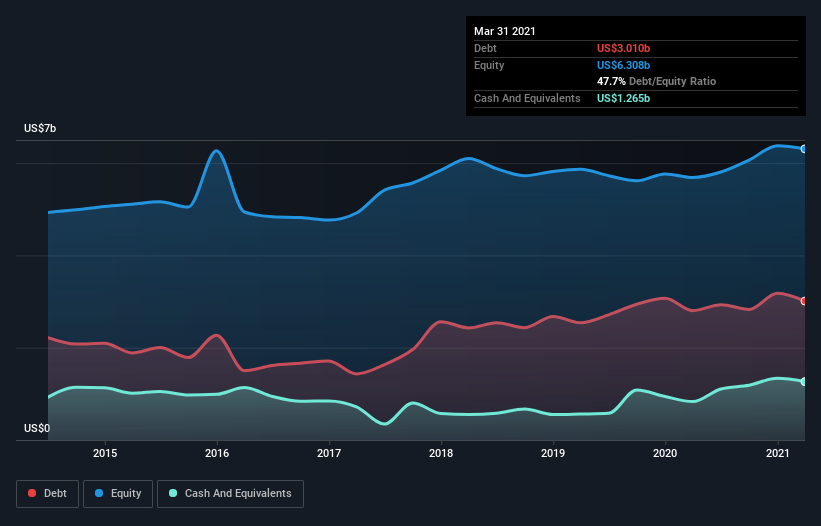

How Much Debt Does COSCO SHIPPING Ports Carry?

The image below, which you can click on for greater detail, shows that at March 2021 COSCO SHIPPING Ports had debt of US$3.01b, up from US$2.80b in one year. On the flip side, it has US$1.27b in cash leading to net debt of about US$1.74b.

How Strong Is COSCO SHIPPING Ports' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that COSCO SHIPPING Ports had liabilities of US$1.11b due within 12 months and liabilities of US$3.69b due beyond that. Offsetting this, it had US$1.27b in cash and US$294.6m in receivables that were due within 12 months. So its liabilities total US$3.24b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company's US$2.74b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

COSCO SHIPPING Ports shareholders face the double whammy of a high net debt to EBITDA ratio (7.3), and fairly weak interest coverage, since EBIT is just 0.81 times the interest expense. This means we'd consider it to have a heavy debt load. Even worse, COSCO SHIPPING Ports saw its EBIT tank 65% over the last 12 months. If earnings keep going like that over the long term, it has a snowball's chance in hell of paying off that debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if COSCO SHIPPING Ports can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, COSCO SHIPPING Ports's free cash flow amounted to 31% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

On the face of it, COSCO SHIPPING Ports's interest cover left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. And even its level of total liabilities fails to inspire much confidence. We should also note that Infrastructure industry companies like COSCO SHIPPING Ports commonly do use debt without problems. After considering the datapoints discussed, we think COSCO SHIPPING Ports has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 4 warning signs we've spotted with COSCO SHIPPING Ports (including 1 which makes us a bit uncomfortable) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading COSCO SHIPPING Ports or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1199

COSCO SHIPPING Ports

An investment holding company, manages and operates ports and terminals in Mainland China, Hong Kong, Europe, and internationally.

Undervalued with acceptable track record.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.2% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor