Advertisement

- Hong Kong

- /

- Wireless Telecom

- /

- SEHK:941

China Mobile (SEHK:941) Reports Strong Earnings Growth and Strategic Expansion in Asia-Pacific Region

Simply Wall St

Reviewed by Simply Wall St

China Mobile (SEHK:941) recently announced strong earnings for the nine months ending September 30, 2024, with sales reaching CNY 791,458 million, reflecting a year-over-year increase. Challenges such as below-industry-average earnings growth and regulatory hurdles persist, yet the company continues to leverage strategic expansions and product innovations to enhance its market position. Readers should anticipate insights into China Mobile's strategic maneuvers and financial health, alongside an analysis of its growth prospects and competitive challenges.

Take a closer look at China Mobile's potential here.

Innovative Factors Supporting China Mobile

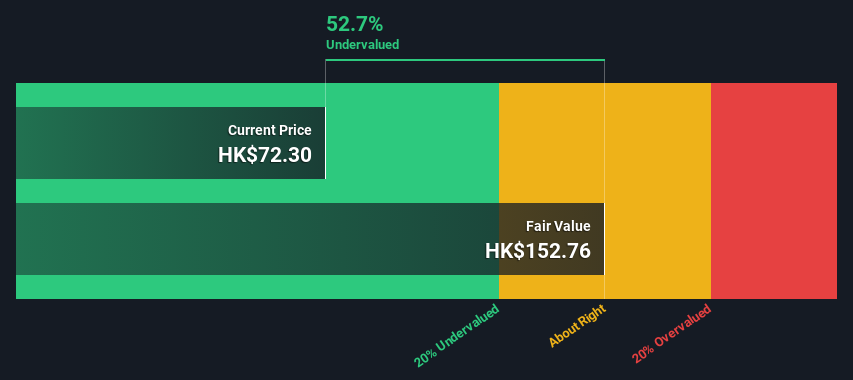

China Mobile's financial stability is underscored by its debt-free status and a consistent dividend history over the past decade. The seasoned management team, with an average tenure of 4.1 years, plays a pivotal role in steering strategic goals, fostering stability and continuity. The company's market presence is evident from a 15% year-over-year revenue increase, as highlighted by CFO Biao He. This growth is largely attributed to strategic expansions in the Asia-Pacific region. Moreover, product innovation drives success, with a 30% rise in adoption rates for new offerings, as noted by Ronghua Li. The company's current share price of HK$71.6, significantly below its estimated fair value of HK$155.72, further underscores its strong market positioning and financial health.

To dive deeper into how China Mobile's valuation metrics are shaping its market position, check out our detailed analysis of China Mobile's Valuation.Critical Issues Affecting the Performance of China Mobile and Areas for Growth

China Mobile faces challenges such as a forecasted Return on Equity of 10.3%, which falls short of industry standards. Revenue growth projections of 3.4% per year lag behind the Hong Kong market's 7.8%. Additionally, recent earnings growth of 3.6% is below the company's five-year average of 6.1%. Operational inefficiencies, particularly in supply chain management, have led to increased costs, impacting margins. The company's North American segment, growing at only 5%, highlights the need for strategic reassessment to stimulate growth in this area.

To gain deeper insights into China Mobile's historical performance, explore our detailed analysis of past performance.Emerging Markets Or Trends for China Mobile

Opportunities abound as analysts predict a significant rise in stock price, with a target more than 20% above the current share price. The potential for profit growth remains, albeit modest. Strategic alliances and product-related announcements, such as those presented at the Goldman Sachs China+ Conference, could enhance market position and capitalize on emerging trends. These initiatives are crucial for maintaining competitive advantage and expanding market share.

See what the latest analyst reports say about China Mobile's future prospects and potential market movements.Regulatory Challenges Facing China Mobile

External threats include intense competition in the wireless telecom industry, where China Mobile's earnings growth of 3.6% trails the industry average of 14.6%. Additionally, regulatory hurdles pose risks to operational continuity and market access. The company's dividend yield of 6.64% is lower than the top 25% of dividend payers in the Hong Kong market, which stands at 7.93%. These factors necessitate vigilance and strategic agility to navigate potential challenges effectively.

Learn about China Mobile's dividend strategy and how it impacts shareholder returns and financial stability.Conclusion

China Mobile's strategic expansion in the Asia-Pacific region and its innovative product offerings have led to a notable 15% increase in revenue, reflecting a strong market position. However, the company faces challenges with its Return on Equity and earnings growth lagging behind industry standards, necessitating improvements in operational efficiency and strategic reassessment, particularly in the North American segment. The company's current share price of HK$71.6, significantly below its estimated fair value of HK$155.72, suggests potential for capital appreciation. This undervaluation, coupled with strategic initiatives and alliances, positions China Mobile for future growth, provided it can effectively navigate regulatory hurdles and enhance its competitive edge.

Turning Ideas Into Actions

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About SEHK:941

China Mobile

Provides telecommunications and information related services in Mainland China and Hong Kong.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor