- Hong Kong

- /

- Real Estate

- /

- SEHK:35

Far East Consortium International's (HKG:35) Shareholders Will Receive A Bigger Dividend Than Last Year

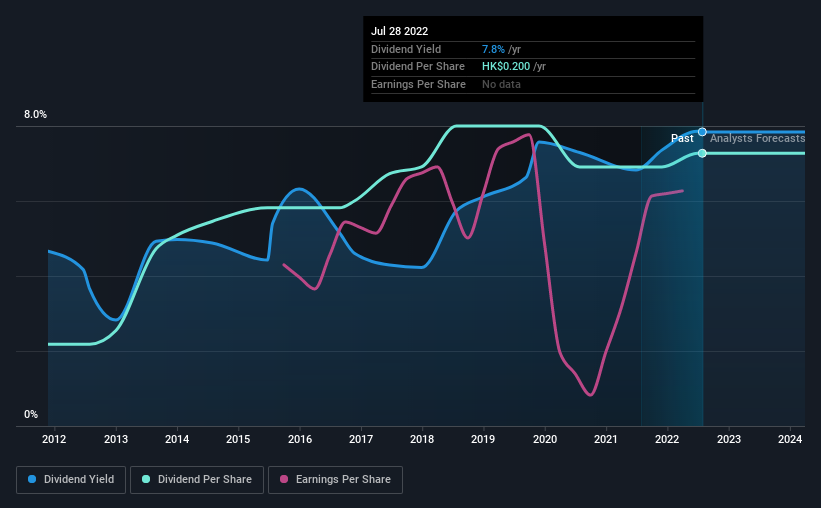

Far East Consortium International Limited (HKG:35) has announced that it will be increasing its dividend from last year's comparable payment on the 21st of September to HK$0.16. This will take the dividend yield to an attractive 7.8%, providing a nice boost to shareholder returns.

Check out our latest analysis for Far East Consortium International

Far East Consortium International's Earnings Easily Cover The Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, Far East Consortium International was easily earning enough to cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS is forecast to fall by 59.1%. If recent patterns in the dividend continue, we could see the payout ratio reaching 80% in the next 12 months, which is on the higher end of the range we would say is sustainable.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2012, the dividend has gone from HK$0.06 total annually to HK$0.20. This implies that the company grew its distributions at a yearly rate of about 13% over that duration. Far East Consortium International has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

Dividend Growth May Be Hard To Achieve

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Earnings has been rising at 3.9% per annum over the last five years, which admittedly is a bit slow. While EPS growth is quite low, Far East Consortium International has the option to increase the payout ratio to return more cash to shareholders.

In Summary

Overall, this is a reasonable dividend, and it being raised is an added bonus. The dividend has been at reasonable levels historically, but that hasn't translated into a consistent payment. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 4 warning signs for Far East Consortium International (2 are concerning!) that you should be aware of before investing. Is Far East Consortium International not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

If you're looking to trade Far East Consortium International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:35

Far East Consortium International

An investment holding company, engages in the property development and investment activities in Australia, New Zealand, the Czech Republic, Hong Kong, Malaysia, the People’s Republic of China, Singapore, the United Kingdom, and the rest of Europe.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives