Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:12

Henderson Land Development (HKG:12) Takes On Some Risk With Its Use Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Henderson Land Development Company Limited (HKG:12) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Henderson Land Development

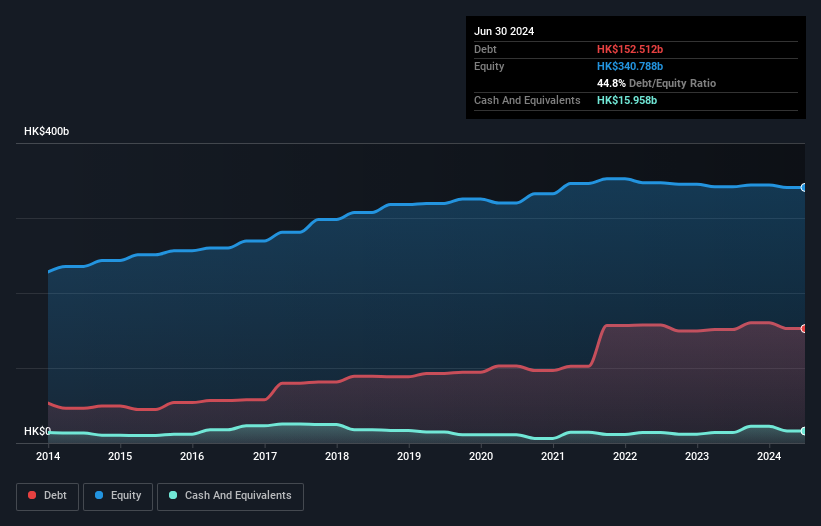

What Is Henderson Land Development's Net Debt?

The chart below, which you can click on for greater detail, shows that Henderson Land Development had HK$152.5b in debt in June 2024; about the same as the year before. On the flip side, it has HK$16.0b in cash leading to net debt of about HK$136.6b.

How Healthy Is Henderson Land Development's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Henderson Land Development had liabilities of HK$56.3b due within 12 months and liabilities of HK$137.9b due beyond that. Offsetting this, it had HK$16.0b in cash and HK$8.32b in receivables that were due within 12 months. So its liabilities total HK$169.9b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's massive market capitalization of HK$123.0b, we think shareholders really should watch Henderson Land Development's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Henderson Land Development has a rather high debt to EBITDA ratio of 19.4 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 6.0 times, suggesting it can responsibly service its obligations. Importantly Henderson Land Development's EBIT was essentially flat over the last twelve months. Ideally it can diminish its debt load by kick-starting earnings growth. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Henderson Land Development can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Henderson Land Development actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

To be frank both Henderson Land Development's level of total liabilities and its track record of managing its debt, based on its EBITDA, make us rather uncomfortable with its debt levels. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. Once we consider all the factors above, together, it seems to us that Henderson Land Development's debt is making it a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Henderson Land Development has 3 warning signs (and 1 which is a bit unpleasant) we think you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Henderson Land Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:12

Henderson Land Development

An investment holding company, engages in the property development and investment activities in Hong Kong and Mainland China.

Moderate growth potential second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor