Advertisement

Need To Know: Analysts Are Much More Bullish On RemeGen Co., Ltd. (HKG:9995) Revenues

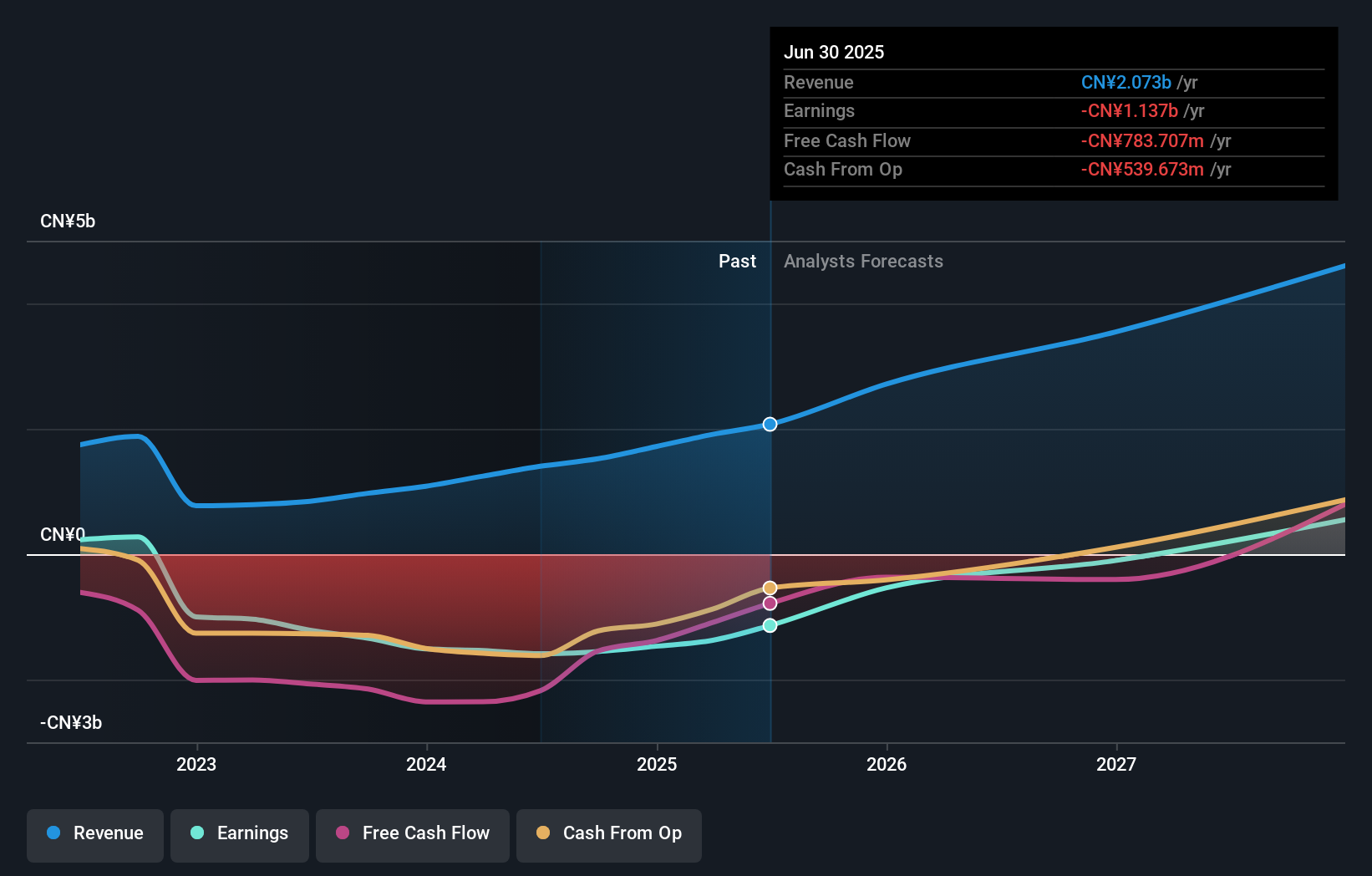

Celebrations may be in order for RemeGen Co., Ltd. (HKG:9995) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with analysts now much more optimistic on its sales pipeline. The market may be pricing in some blue sky too, with the share price gaining 12% to HK$87.85 in the last 7 days. We'll be curious to see if these new estimates convince the market to lift the stock price higher still.

Following the upgrade, the latest consensus from RemeGen's 14 analysts is for revenues of CN¥2.7b in 2025, which would reflect a major 31% improvement in sales compared to the last 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 53% to CN¥0.96. Yet before this consensus update, the analysts had been forecasting revenues of CN¥2.4b and losses of CN¥1.54 per share in 2025. We can see there's definitely been a change in sentiment in this update, with the analysts administering a sizeable upgrade to this year's revenue estimates, while at the same time reducing their loss estimates.

See our latest analysis for RemeGen

The consensus price target rose 35% to CN¥58.18, with the analysts encouraged by the higher revenue and lower forecast losses for this year. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on RemeGen, with the most bullish analyst valuing it at CN¥107 and the most bearish at CN¥14.60 per share. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how think this business will perform. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the RemeGen's past performance and to peers in the same industry. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 31% growth on an annualised basis. That is in line with its 36% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 26% annually. So although RemeGen is expected to maintain its revenue growth rate, it's only growing at about the rate of the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting RemeGen is moving incrementally towards profitability. They also upgraded their revenue forecasts, although the latest estimates suggest that RemeGen will grow in line with the overall market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at RemeGen.

It's great to see the analysts upgrading their estimates, but the biggest highlight to us is that the business is expected to become profitable in the foreseeable future. For more information, you can click through to our free platform to learn more about these forecasts.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:9995

RemeGen

A biopharmaceutical company, discovers, develops, produces and commercializes biological drugs for the treatment of autoimmune, oncology, and ophthalmic diseases in Mainland China and the United States.

Exceptional growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor