Advertisement

As global markets face varied economic challenges, including shifts in inflation and interest rate expectations, the Hong Kong market has been navigating its own set of dynamics with a focus on growth and insider confidence. Amidst this backdrop, identifying growth companies with significant insider ownership can be particularly insightful as it often signals strong internal belief in the company's potential.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| Laopu Gold (SEHK:6181) | 36.4% | 33.2% |

| Akeso (SEHK:9926) | 20.5% | 53% |

| Fenbi (SEHK:2469) | 33.1% | 22.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.8% | 69.8% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Ocumension Therapeutics (SEHK:1477) | 24% | 95.6% |

| DPC Dash (SEHK:1405) | 38.1% | 104.8% |

| Beijing Airdoc Technology (SEHK:2251) | 29.4% | 93.4% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 71.8% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 109.2% |

Let's uncover some gems from our specialized screener.

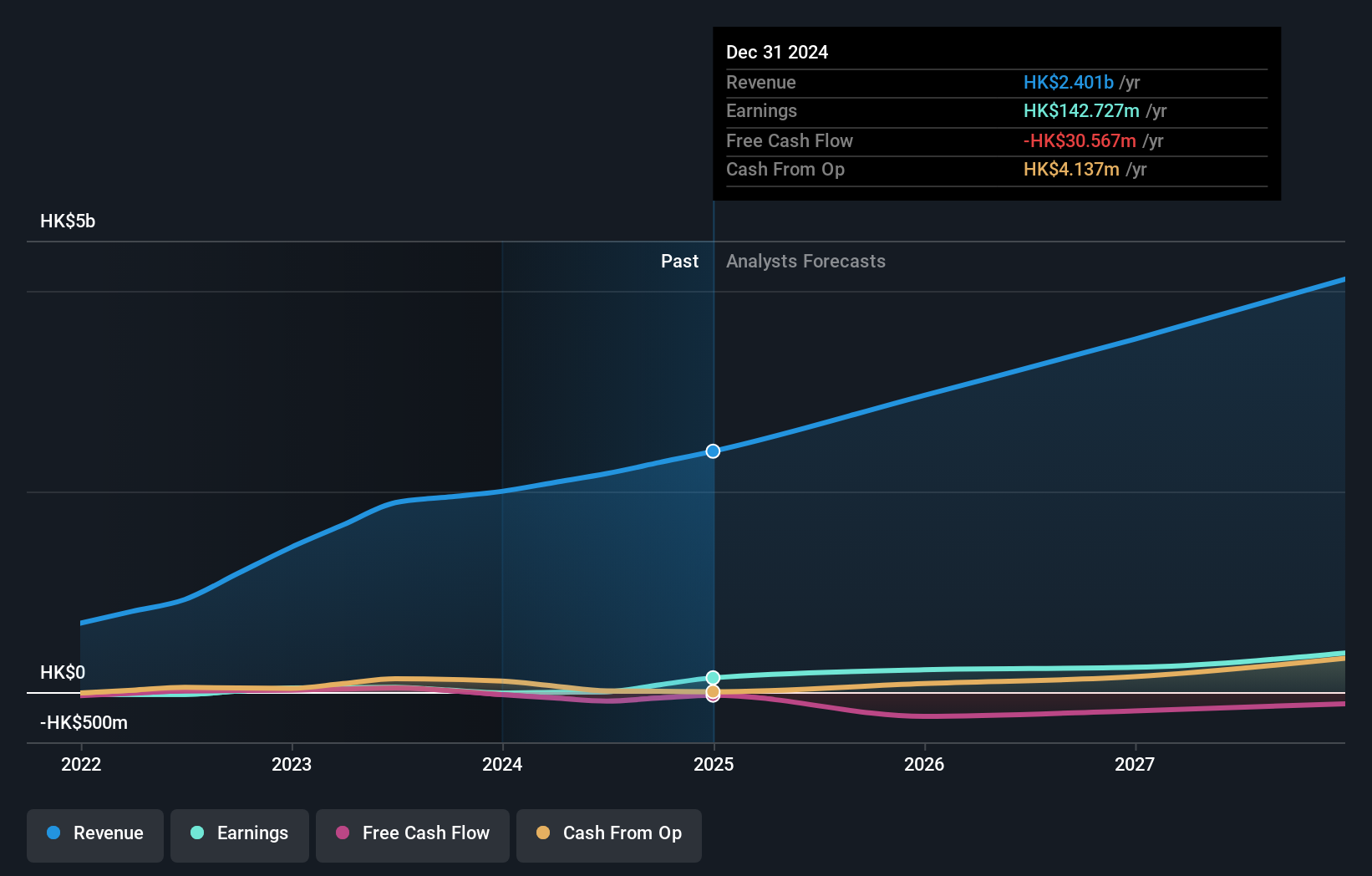

Vobile Group (SEHK:3738)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Vobile Group Limited is an investment holding company that offers software as a service for digital content asset protection and transactions across the United States, Japan, Mainland China, and internationally, with a market cap of HK$5.70 billion.

Operations: The company generates revenue primarily from its software as a service offerings, amounting to HK$2.18 billion.

Insider Ownership: 23.1%

Vobile Group is experiencing significant growth, with earnings projected to increase by 68.45% annually over the next three years, outpacing the Hong Kong market. However, profit margins have declined recently. Despite past shareholder dilution and share price volatility, Vobile trades below its estimated fair value and has initiated a share buyback program to enhance net asset value per share. Recent earnings show improved sales at HK$1.18 billion and net income of HK$41.47 million for H1 2024.

- Click here and access our complete growth analysis report to understand the dynamics of Vobile Group.

- Our comprehensive valuation report raises the possibility that Vobile Group is priced higher than what may be justified by its financials.

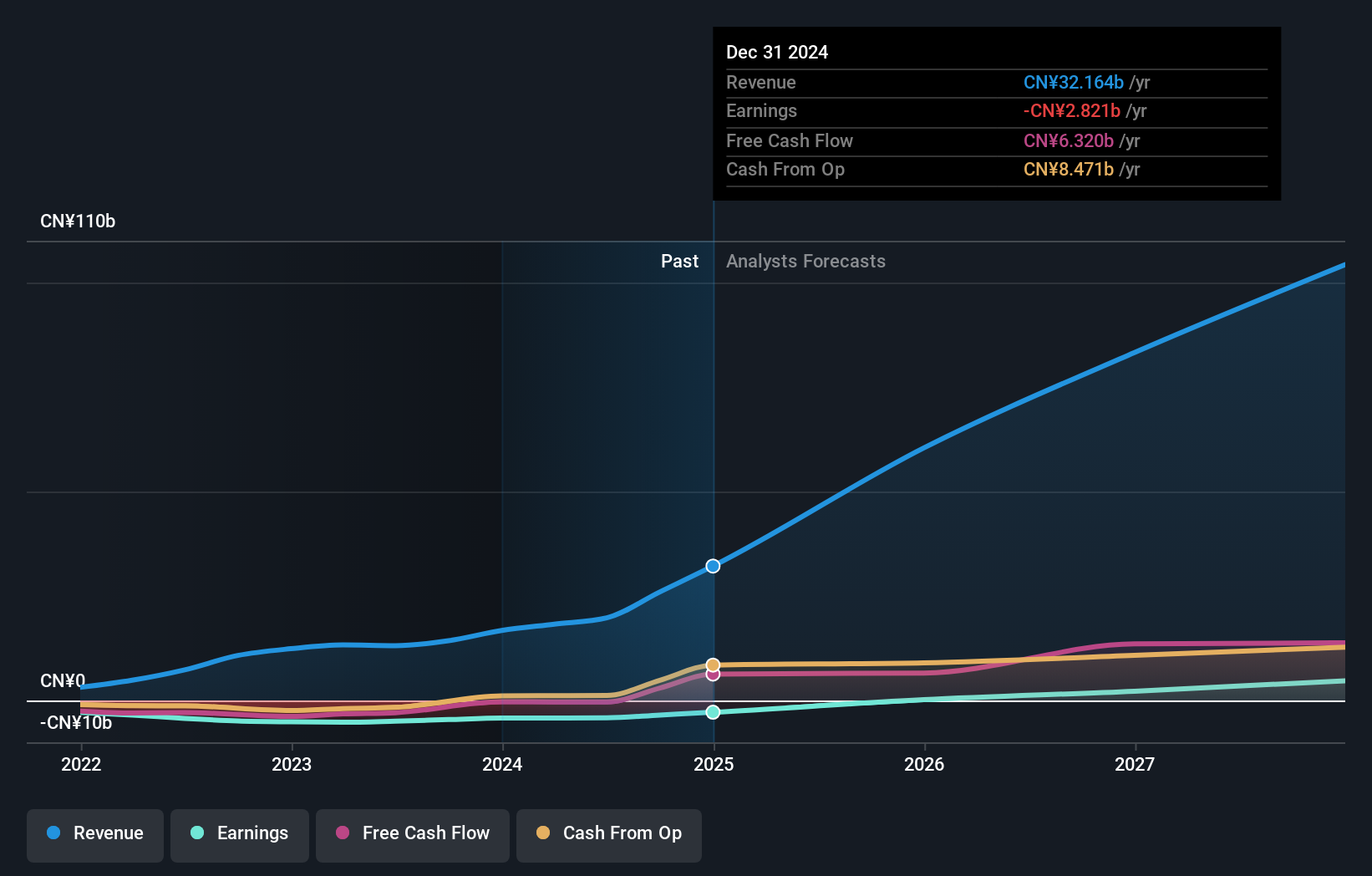

Zhejiang Leapmotor Technology (SEHK:9863)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zhejiang Leapmotor Technology Co., Ltd. focuses on the research, development, production, and sale of energy vehicles in China, with a market cap of HK$38.30 billion.

Operations: The company's revenue primarily comes from the production, research and development, and sales of new energy vehicles, amounting to CN¥19.78 billion.

Insider Ownership: 15%

Zhejiang Leapmotor Technology is poised for substantial growth, with revenue expected to climb 33.2% annually, surpassing Hong Kong's market average. The company anticipates profitability within three years despite past shareholder dilution and a net loss of CNY 2.21 billion in H1 2024. Insider confidence remains high, with significant insider buying and no major sales recently reported. Trading at a considerable discount to estimated fair value, the stock reflects potential upside as strategic amendments proceed.

- Get an in-depth perspective on Zhejiang Leapmotor Technology's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, Zhejiang Leapmotor Technology's share price might be too optimistic.

Akeso (SEHK:9926)

Simply Wall St Growth Rating: ★★★★★★

Overview: Akeso, Inc. is a biopharmaceutical company that focuses on researching, developing, manufacturing, and commercializing antibody drugs with a market cap of HK$58.83 billion.

Operations: The company's revenue from the research, development, production, and sale of biopharmaceutical products is CN¥1.87 billion.

Insider Ownership: 20.5%

Akeso, Inc. demonstrates strong growth potential with expected revenue growth of 33.5% annually, surpassing the Hong Kong market average. Despite recent shareholder dilution and a net loss of CNY 238.59 million in H1 2024, insider ownership remains significant, indicating confidence in future prospects. Recent positive clinical trial results for its cancer treatment cadonilimab highlight its commercialization potential and address critical unmet needs in oncology, further strengthening Akeso's position as it trades below estimated fair value.

- Navigate through the intricacies of Akeso with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that Akeso is trading beyond its estimated value.

Taking Advantage

- Get an in-depth perspective on all 48 Fast Growing SEHK Companies With High Insider Ownership by using our screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Leapmotor Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:9863

Zhejiang Leapmotor Technology

Engages in the research and development, production, and sale of new energy vehicles in Mainland China and internationally.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor