Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that CStone Pharmaceuticals (HKG:2616) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Our analysis indicates that 2616 is potentially overvalued!

What Is CStone Pharmaceuticals's Net Debt?

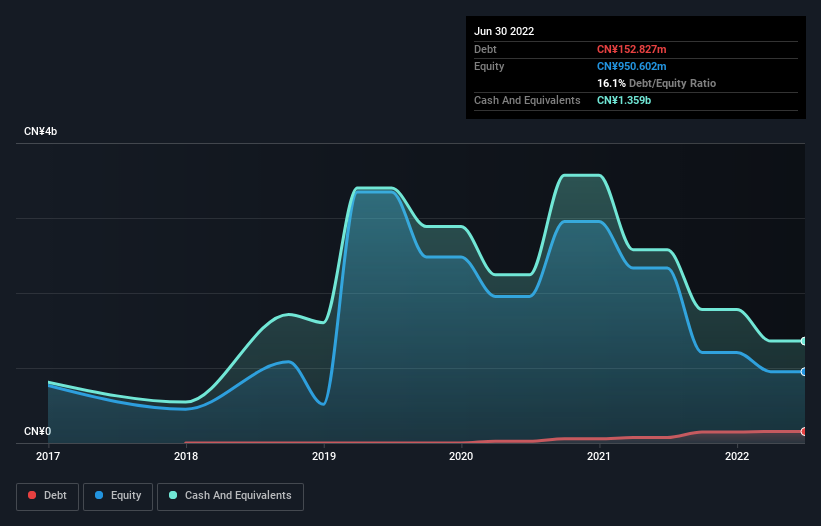

As you can see below, at the end of June 2022, CStone Pharmaceuticals had CN¥152.8m of debt, up from CN¥72.7m a year ago. Click the image for more detail. But on the other hand it also has CN¥1.36b in cash, leading to a CN¥1.21b net cash position.

A Look At CStone Pharmaceuticals' Liabilities

Zooming in on the latest balance sheet data, we can see that CStone Pharmaceuticals had liabilities of CN¥900.6m due within 12 months and liabilities of CN¥163.5m due beyond that. Offsetting this, it had CN¥1.36b in cash and CN¥164.0m in receivables that were due within 12 months. So it can boast CN¥458.7m more liquid assets than total liabilities.

This surplus suggests that CStone Pharmaceuticals has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that CStone Pharmaceuticals has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine CStone Pharmaceuticals's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, CStone Pharmaceuticals made a loss at the EBIT level, and saw its revenue drop to CN¥426m, which is a fall of 62%. To be frank that doesn't bode well.

So How Risky Is CStone Pharmaceuticals?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months CStone Pharmaceuticals lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through CN¥1.2b of cash and made a loss of CN¥1.5b. But the saving grace is the CN¥1.21b on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 1 warning sign for CStone Pharmaceuticals that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2616

CStone Pharmaceuticals

A biopharmaceutical company, researches and develops anti-cancer therapies to address the unmet medical needs of cancer patients in China and internationally.

Excellent balance sheet with reasonable growth potential.

Market Insights

Community Narratives