Advertisement

Risks Still Elevated At These Prices As ImmuneOnco Biopharmaceuticals (Shanghai) Inc. (HKG:1541) Shares Dive 29%

ImmuneOnco Biopharmaceuticals (Shanghai) Inc. (HKG:1541) shares have retraced a considerable 29% in the last month, reversing a fair amount of their solid recent performance. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 24% in that time.

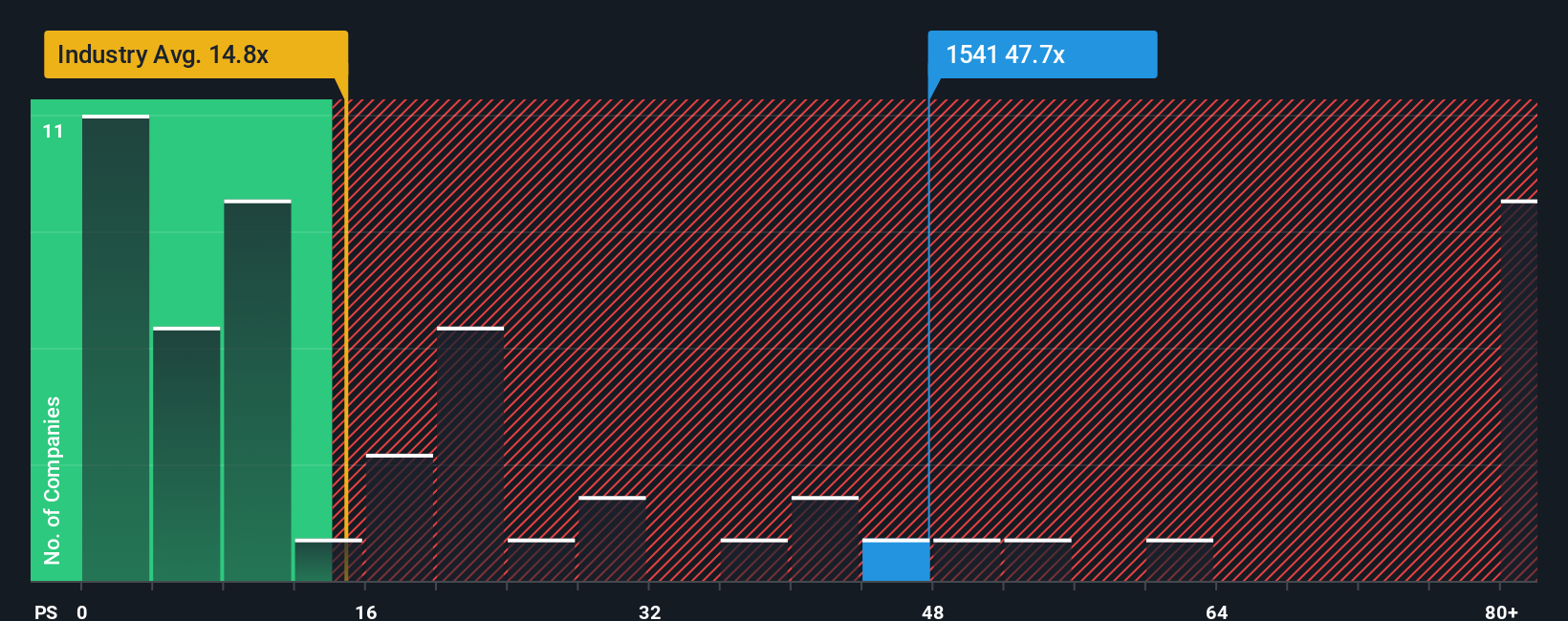

Although its price has dipped substantially, ImmuneOnco Biopharmaceuticals (Shanghai) may still be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 47.7x, since almost half of all companies in the Biotechs industry in Hong Kong have P/S ratios under 14.8x and even P/S lower than 5x are not unusual. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for ImmuneOnco Biopharmaceuticals (Shanghai)

How ImmuneOnco Biopharmaceuticals (Shanghai) Has Been Performing

Recent times have been advantageous for ImmuneOnco Biopharmaceuticals (Shanghai) as its revenues have been rising faster than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think ImmuneOnco Biopharmaceuticals (Shanghai)'s future stacks up against the industry? In that case, our free report is a great place to start.How Is ImmuneOnco Biopharmaceuticals (Shanghai)'s Revenue Growth Trending?

In order to justify its P/S ratio, ImmuneOnco Biopharmaceuticals (Shanghai) would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered an explosive gain to the company's top line. Spectacularly, three year revenue growth has also set the world alight, thanks to the last 12 months of incredible growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 58% per year as estimated by the only analyst watching the company. With the industry predicted to deliver 359% growth per annum, the company is positioned for a weaker revenue result.

With this information, we find it concerning that ImmuneOnco Biopharmaceuticals (Shanghai) is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What Does ImmuneOnco Biopharmaceuticals (Shanghai)'s P/S Mean For Investors?

ImmuneOnco Biopharmaceuticals (Shanghai)'s shares may have suffered, but its P/S remains high. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

It comes as a surprise to see ImmuneOnco Biopharmaceuticals (Shanghai) trade at such a high P/S given the revenue forecasts look less than stellar. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 1 warning sign for ImmuneOnco Biopharmaceuticals (Shanghai) that you need to be mindful of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1541

ImmuneOnco Biopharmaceuticals (Shanghai)

A biotechnology company, engages in the research and development of immuno-oncology therapies in the People’s Republic of China.

Excellent balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor