Advertisement

- Hong Kong

- /

- Entertainment

- /

- SEHK:6899

We Think Ourgame International Holdings (HKG:6899) Can Afford To Drive Business Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So, the natural question for Ourgame International Holdings (HKG:6899) shareholders is whether they should be concerned by its rate of cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for Ourgame International Holdings

Does Ourgame International Holdings Have A Long Cash Runway?

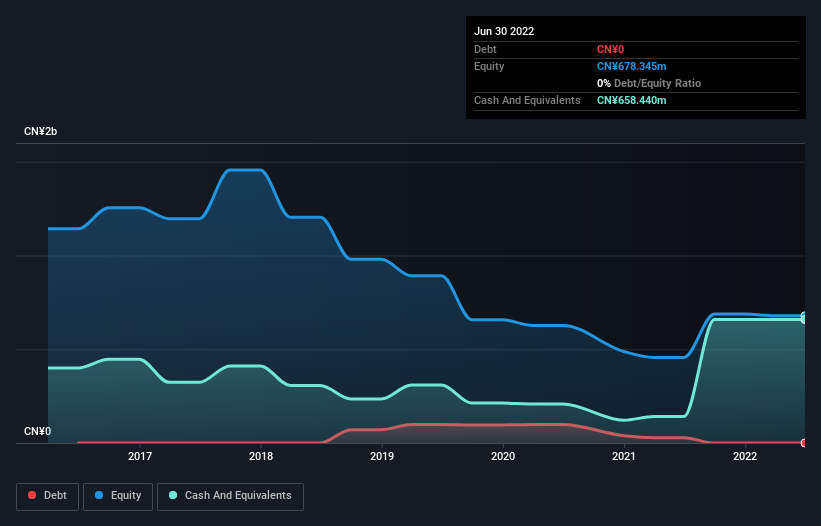

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. As at June 2022, Ourgame International Holdings had cash of CN¥658m and no debt. In the last year, its cash burn was CN¥190m. That means it had a cash runway of about 3.5 years as of June 2022. There's no doubt that this is a reassuringly long runway. Depicted below, you can see how its cash holdings have changed over time.

Is Ourgame International Holdings' Revenue Growing?

We're hesitant to extrapolate on the recent trend to assess its cash burn, because Ourgame International Holdings actually had positive free cash flow last year, so operating revenue growth is probably our best bet to measure, right now. It's nice to see that operating revenue was up 47% in the last year. Of course, we've only taken a quick look at the stock's growth metrics, here. This graph of historic revenue growth shows how Ourgame International Holdings is building its business over time.

How Hard Would It Be For Ourgame International Holdings To Raise More Cash For Growth?

Notwithstanding Ourgame International Holdings' revenue growth, it is still important to consider how it could raise more money, if it needs to. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Ourgame International Holdings' cash burn of CN¥190m is about 70% of its CN¥269m market capitalisation. That's very high expenditure relative to the company's size, suggesting it is an extremely high risk stock.

How Risky Is Ourgame International Holdings' Cash Burn Situation?

On this analysis of Ourgame International Holdings' cash burn, we think its cash runway was reassuring, while its cash burn relative to its market cap has us a bit worried. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. Its important for readers to be cognizant of the risks that can affect the company's operations, and we've picked out 2 warning signs for Ourgame International Holdings that investors should know when investing in the stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6899

Ourgame International Holdings

An investment holding company, develops and operates online card and board games in the People’s Republic of China and internationally.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor