Advertisement

Oriental Enterprise Holdings' (HKG:18) Dividend Will Be HK$0.01

Oriental Enterprise Holdings Limited (HKG:18) has announced that it will pay a dividend of HK$0.01 per share on the 10th of September. This means that the annual payment will be 5.6% of the current stock price, which is in line with the average for the industry.

Oriental Enterprise Holdings' Projected Earnings Seem Likely To Cover Future Distributions

Solid dividend yields are great, but they only really help us if the payment is sustainable. Before this announcement, Oriental Enterprise Holdings was paying out 91% of earnings, but a comparatively small 40% of free cash flows. This leaves plenty of cash for reinvestment into the business.

EPS is set to fall by 3.9% over the next 12 months if recent trends continue. If recent patterns in the dividend continue, we could see the payout ratio reaching 92% in the next 12 months which is on the higher end of the range we would say is sustainable.

Check out our latest analysis for Oriental Enterprise Holdings

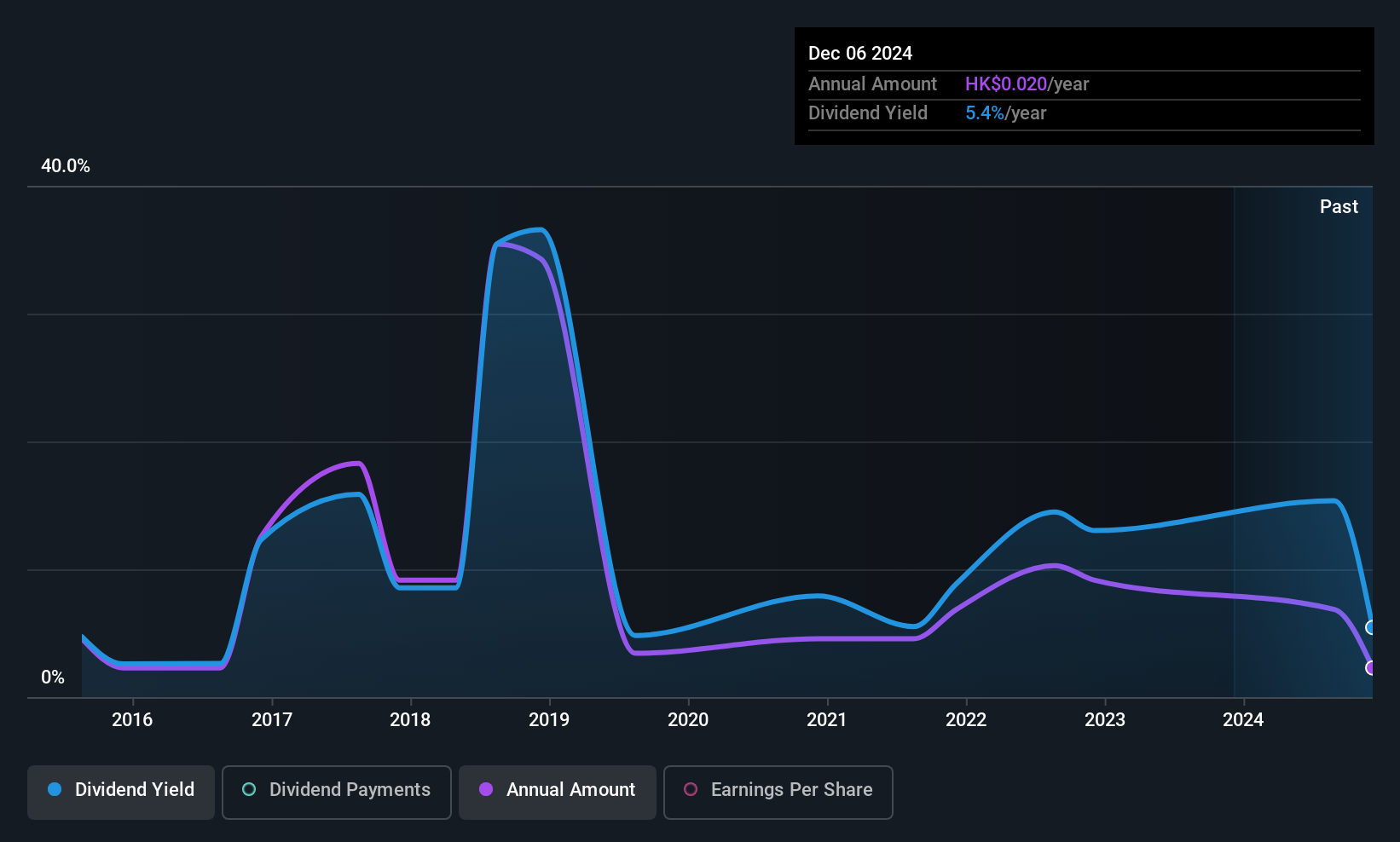

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2015, the dividend has gone from HK$0.05 total annually to HK$0.02. The dividend has shrunk at around 8.8% a year during that period. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend's Growth Prospects Are Limited

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Oriental Enterprise Holdings has seen earnings per share falling at 3.9% per year over the last five years. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed.

In Summary

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 1 warning sign for Oriental Enterprise Holdings that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:18

Oriental Enterprise Holdings

An investment holding company, engages in the publication of newspapers in Hong Kong and Australia.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|50.2% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|3.4% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|1.4% undervalued

ZW

Community Contributor